Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Can You Retire at 65? Survival vs. Maximum Wealth Guide.

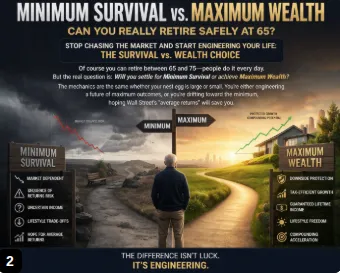

Minimum Survival vs. Maximum Wealth: Can You Really Retire Safely at 65?

![[HERO] Minimum Survival vs. Maximum Wealth: Can You Really Retire Safely at 65?](https://cdn.marblism.com/tqDUOQ-jIky.webp "[HERO] Minimum Survival vs. Maximum Wealth: Can You Really Retire Safely at 65?")

Can you retire safely between the ages of 65 and 75?

Of course you can. People do it every day. But here is the thing: the question isn’t really about if you can stop working. The question is whether you will settle for Minimum Survival or achieve Maximum Wealth.

Whether you have a massive nest egg or a modest one, the mechanics are the same. You are either engineering a future of "Maximum" outcomes: where your lifestyle is guaranteed and your compounding is protected: or you are drifting toward the "Minimum," hoping that Wall Street’s "Average Returns" don’t desert you when you need them most.

Some wealthy folks get lazy with their plans, assuming a big number on a screen equals safety. Others, with less wealth, feel defeated by the "leaks and losses" of their past. Both groups are often operating on a False Model driven by fear and greed, rather than the institutional-grade engineering required for a "Forever Lifestyle."

Let’s pull back the curtain on why your current plan might be a "Rolodex in a SpaceX world" and how to fix it.

The Minimum: The "Death by a Thousand Leaks" Strategy

When we talk about "Minimum Survival," we aren't necessarily talking about poverty. We are talking about a retirement that is constantly under threat. It’s a retirement where you are surviving on what’s left after the "leaks" take their cut.

What are these leaks?

Market Losses: The "spinning sharp knives" of volatility.

Taxes: The silent partner that takes a third of your success.

Fees: The hidden complexity Wall Street uses to extract value.

Sequence of Returns Risk (SORR): The math of bad luck.

If you retire at 65 and the market drops 20% in your first three years, your "average return" might look fine on paper a decade later, but your bank account will be gasping for air. This is the Sequence of Return Margin. When you experience losses and taxes early in retirement, you have almost zero chance of achieving the "Maximum."

")

As the chart above shows, bear markets happen roughly every five years. If you are "Participating" in the market without a design, you are essentially gambling that the 5.2-year break-even period won't happen the year you decide to stop working.

The Maximum: Engineering the Sum of the Parts

Maximum wealth isn’t about picking the "hot stock." It’s about Engineering Compounding for the longest period of time possible.

The goal is to make the sum of the parts you contribute greater than the whole. How? By removing the "Math of Recovery."

Think about it: if you lose 30% of your portfolio, you don't just need a 30% gain to get back to even. You need a 42% gain just to get back to where you started. That is wasted time. In the world of "Quiet Builders," time is the one asset we cannot manufacture more of.

Maximum wealth focuses on Compounding Efficiency. It’s the difference between "Hope" (Wall Street’s favorite product) and "Evidence" (Engineering’s favorite outcome).

The Evolution: From Individual Stocks to Multi-Pillar Protection

Most people’s financial journey looks like this:

Individual Stocks: You choose a portfolio of "winners." This provides the maximum opportunity for achieving the minimum. Why? Because the risk of a single pillar failing is too high.

Index Funds: You realize the "experts" can't beat the market, so you join the market. You improve your opportunity for success, but you are still fully exposed to the -30% drawdowns.

Multiple Indexes with Multiple Pillars: This is the "Smartphone" of finance.

In the old days, you had a phone, a pager, a map, and a camera. Today, they are all inside one device. Traditional assets like individual stocks or rental properties are "Single-Pillar" assets. They do one thing, but they carry high risk or high fees.

Fully Performing Assets (FPA) are the foundation of a modern retirement. These are "Multi-Pillar" vehicles that can provide 5 to 15 pillars of value: such as growth, protection, long-term care benefits, and tax-free income: all within one structure. They offer Uncapped Gains (UCG) and Expanded Market Participation (EMP).

Imagine a world where your range of outcomes is 0% to +30% instead of Wall Street’s -30% to +30%. When you eliminate the negatives, the "Math of Recovery" disappears. You aren't just participating; you are performing.

Why "Average Returns" are a Wall Street Lie

When asking "how much do I need to retire," most people use a standard retirement income calculator. These calculators usually ask for an "average annual return."

Average returns don't pay bills. Actual returns do.

If you have $1 million and lose 50% in year one, then gain 100% in year two, your "average return" is a glowing 25%. But your actual balance? It’s exactly $1 million. You’ve gone nowhere for two years.

This is why we perform a Margin Audit™ and a Volatility Recovery Analysis. We look for the "leaks" in your current boat before we try to put a bigger motor on it. We shift the focus from "How much do I need to retire?" to "How much guaranteed retirement income can we engineer?"

Unlearning the Myths

To get to the "Maximum," you have to be willing to stay out of the place where Wall Street wants you to stay. They want you addicted to the noise, the headlines, and the daily "research" that drives buying and selling.

It’s about Awareness & Unlearning. You have to unlearn the myth that risk is a requirement for growth.

In our world, Risk is for Business, Not Retirement.

We treat financial planning like architecture. You wouldn't build a house by "participating" in a pile of lumber and hoping a roof forms. You use a blueprint. You use engineering. You ensure the foundation can support the weight of your future.

The Million Dollar Hour™: Your Engineering Blueprint

If you are a "Quiet Builder": successful, perhaps a bit financially fatigued, and looking for certainty: then "hope" is no longer a strategy you can afford.

The Million Dollar Hour™ Forecast is our institutional-grade process designed to translate your current "Assets at Risk" into a designed, engineered outcome. This isn't a "free consultation" where a salesman tries to pitch you a product. This is a $995 professional engineering session.

In one 60-minute session, we conduct a Margin Audit™ to see exactly where your plan leads: not just where it has been. We look at:

GPV (Today's Value): What is your money actually worth right now after taxes and fees?

GFV (Future Value): Where is the math actually taking you?

The 5 Pillars of Wealth Restoration: How do we recover lost time, taxes, and fees?

We use the Million Dollar Hour™ to show you the evidence of outcomes based on financial fundamentals, rather than depending on the luck of Wall Street myths.

Peace is the Path, Wisdom is the Way

Can you retire safely at 65? Yes. But don't settle for the minimum survival that the "False Model" offers.

By shifting from Participation to Engineered Performance, you can stop guessing and start knowing. You can move your assets from "Underperforming" or "At Risk" to "Fully Performing."

It’s your money, your rules, in your time, on your street.

Stop spinning sharp knives and start building a foundation that lasts for life. The transition from a "Rolodex" strategy to a "SpaceX" strategy starts with one hour of clarity.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.