Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

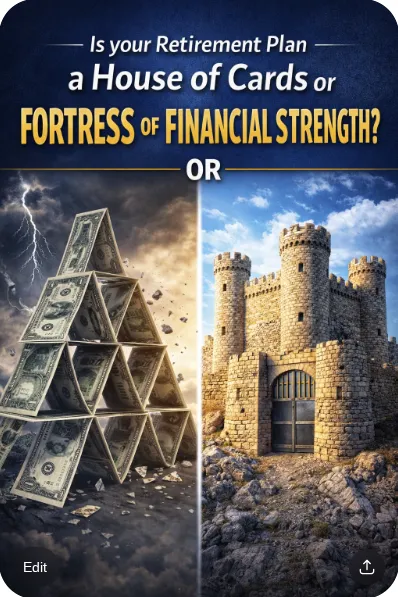

Retirement Planning: House of Cards or Financial Fortress?

Is your Retirement Plan a House of Cards or a Fortress of Financial Strength?

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

![[HERO] Is your Retirement Plan a House of Cards or a Fortress of Financial Strength?](https://cdn.marblism.com/F20XsejNCVT.webp "[HERO] Is your Retirement Plan a House of Cards or a Fortress of Financial Strength?")

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The Wall Street Mirage vs. The Wealth Reality

You’ve spent thirty or forty years in the trenches. You’ve built the business, climbed the ladder, and stayed disciplined while everyone else was chasing the latest shiny object. By all accounts, you’ve "made it." You have a nice number on a statement that arrives in your inbox every month.

But there’s a nagging feeling in the back of your mind, isn’t there?

It’s that "quiet unease" that comes from knowing your lifestyle is currently tied to a system you don’t control. You’re "participating" in the market, which is Wall Street’s polite way of saying you’re gambling with your timeframe.

In our world, we call this the Fugazi vs. Founded dilemma.

Is your retirement plan a "Fugazi": a mirage made of pixie dust, hidden fees, and market volatility? Or is it "Founded": built on institutional-grade engineering and mathematical certainty?

If your plan is a house of cards, one bad year (or one "sequence of return" error) could blow the whole thing down. If it’s a fortress, it doesn’t matter what the Federal Reserve does or what the headlines say. Your money follows your rules, in your time, on your street.

The Wall Street Mirage: A Rolodex in a SpaceX World

Most traditional retirement strategies are what we call "single-pillar" models. You put money in a bank (low return), you put money in the stock market (high risk), or you buy real estate (low liquidity/high hassle). These are old-school tools. They worked in the 80s, but today? Relying on them for a 30-year retirement is like trying to run a global logistics company using a Rolodex in a SpaceX world.

Wall Street thrives on "Participation." They want you addicted to the daily noise, the greed-and-fear meter, and the complex jargon that justifies their fees. But participation isn’t performance. Performance is engineered.

When you’re in a "House of Cards" plan, you are susceptible to the Math of Recovery. Consider this: if the market drops 30% (which happens on average every five years), you don’t just need 30% to get back to even. You need a 42.8% gain just to see the surface again. While you’re waiting five or six years to recover, you’re still burning cash for living expenses. That’s a leak in your foundation that most "advisors" never mention.

The Fugazi vs. Founded Framework: The 7 Steps to a Fortress

At Your Street Wealth, we don’t do "guesses." We do architecture. To move from a House of Cards to a Fortress of Financial Strength, we use a 7-step engineering process.

1. Question

Everything starts by questioning the "False Model." Why are you taking market risk with money you can’t afford to lose? Why are you okay with "uncapped losses" in exchange for "potential gains"? We start by asking if your income is designed or merely dependent on market luck.

2. Inspect (The Margin Audit™)

We look for the leaks. Most plans are bleeding wealth through what we call "The Three Leaks": unnecessary taxes, hidden fees, and Volatility Recovery time. A Margin Audit™ scrutinizes every dollar to see if it's actually working for you or just sitting in a Non-Performing Asset (NPA).

3. Seek Unconditional Process

In a Fortress, we don’t rely on conditions (like "the market has to go up"). We seek an unconditional process where the rules are set in advance. We shift from "Participation" (gambling) to "Engineered Performance" (design).

4. Determine Rules

Your Money, Your Rules. Wall Street has rules that benefit them (like surrender charges or limited access). A Founded plan establishes your rules for liquidity, use, and control of your capital.

5. Forecast (The Million Dollar Hour™)

This is where the magic happens. We don’t "predict" the future; we forecast it based on the current trajectory. Most people can estimate their income needs, but they have zero clue what their future portfolio value will be because they can't control the losses. The Million Dollar Hour™ Forecast provides the engineering blueprint to show exactly where your plan leads: not just where it’s been.

6. Compare

We compare your current "Assets at Risk" (AAR) against "Fully Performing Assets" (FPA).

AAR (Wall Street): The -30% to +30% roller coaster.

FPA (Your Street): The 0% to +30% engineered path.

In an FPA, when the market crashes, you stay at zero (you don't lose). When it gains, you participate in the growth. This is the "Smartphone" of finance: consolidating growth, protection, and tax efficiency into one multi-pillar vehicle.

7. Measure

Finally, we measure the Compounding Efficiency. We look at the "Sequence of Return Margin" to ensure that even if you retire the day before a market crash, your lifestyle remains untouched.

The Mathematics of a Fortress

Why does the "Fortress" approach win? Because it eliminates the "Sharp Knives" of volatility.

Look at the history of the S&P 500. Bear markets aren't "black swan" events; they are features of the system. They happen roughly every five years and take an average of 5.2 years just to break even.

")

If you are 60 years old, how many "5.2-year recovery periods" do you have left in your tank? Your most valuable asset isn't your money; it’s your time. A House of Cards plan gambles with your time. A Fortress plan protects it.

We utilize Fully Performing Assets (FPA) that offer what we call Expanded Market Participation (EMP). Imagine a multiplier on your gains: if the market grows 10%, an EMP strategy might deliver 11% to 20% growth, while still maintaining a "0% floor" on the downside. This isn't magic; it’s institutional-grade Asset Liability Management (ALM).

The Consolidation of Technology: From Single-Pillar to Multi-Pillar

Think back 20 years. You had a pager, a camera, a GPS, and a phone. Today, you just have a smartphone. The "Single Pillar" model of keeping your money in three separate buckets (Bank, Stock, Real Estate) is the pager/camera/GPS era.

Fully Performing Assets are the "Smartphone" of wealth. They consolidate 5 to 15 pillars of value: including growth, principal protection, tax-free income, and long-term care benefits: into one engineered vehicle.

When you move your assets from the top of the pyramid (Assets at Risk) down to the foundation (Fully Performing Assets), you stop "spinning sharp knives" and start building a legacy.

Are You a Quiet Builder?

We don’t write for everyone. We don’t chase "mice" looking for "free cheese." We write for the Quiet Builders. You’ve done the work. You have the capital. Now, you’re just tired of the noise. You’re financially fatigued by a system that seems designed to extract value from you rather than provide certainty to you.

You don't need another "stock tip." You need an Architect.

Architecture is a designed process that grows and heals. Participation is a false architecture that extracts and harms. If you want to stop "participating" in Wall Street's game and start "performing" on your own terms, it's time for a change in perspective.

The Path to Wisdom

"Peace is the path, wisdom is the way."

Wisdom isn't just knowing facts; it's making the right decisions based on mathematical truth. The truth is that you cannot win a game where the rules are stacked against you and the "house" (Wall Street) always takes its cut regardless of whether you win or lose.

It’s time to move your wealth off of "Their Street" and onto "Your Street."

The first step isn't buying a product. It's unlearning the myths. It’s sitting down for 60 minutes to conduct a structural inspection of your financial house.

Is it a House of Cards, waiting for the next gust of market wind? Or is it a Fortress of Financial Strength, engineered to last for generations?

The clarity you’re looking for isn't in a headline. It’s in the engineering.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now

Check out the Retirement Blueprint