Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

7 Disciplines. One Framework. No More Guessing.

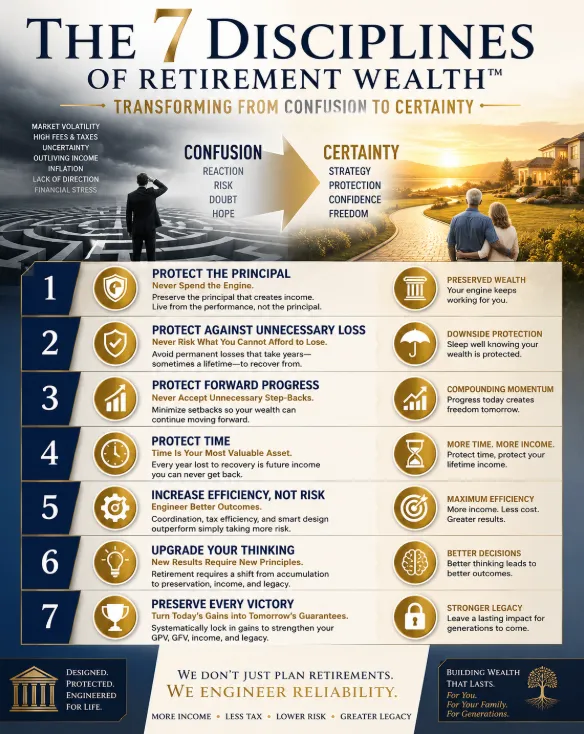

The 7 Disciplines of Retirement Wealth™: The Framework That Turns Confusion into Certainty

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

The 7 Disciplines of Retirement Wealth™: The Framework That Turns Confusion into Certainty

One Framework. Seven Disciplines. A Lifetime of Better Decisions.

If you are a successful professional or business owner between the ages of 45 and 75, you’ve likely spent decades following a specific set of rules. You were told to save, diversify, and "ride out" the market cycles.

But as you approach or enter retirement, those rules start to feel like a Rolodex in a SpaceX world. They were durable in the 1980s, but they are fundamentally inadequate for the speed, volatility, and technical demands of modern retirement.

Most people are unknowingly operating on a False Model driven by Wall Street's "Shiny Objects": the 7–10% average return mirage. They ignore the Dark Objects: cumulative cycle losses, the wealth-killing "time tax," and the reality that a single 30% retraction requires a 42% gain just to break even.

At Your Street Wealth, we don't guess. We engineer. Why?

"Retirement is not an investment problem.

It is an engineering problem."

We look at your retirement through the lens of Institutional-Grade Asset Liability Management (ALM). We don't "participate" in the market; we design outcomes. To do that, we use The 7 Disciplines of Retirement Wealth™. This is the foundational "why" that precedes every decision on your balance sheet.

Discipline 1 : Protect the Principal

Never Spend the Engine.

Is your retirement plan designed to preserve your wealth engine?

Wealth is not a number in a bank account; it is the asset that produces income. In the traditional Wall Street model, retirees are often forced to "cannibalize" their principal to maintain their lifestyle: especially during market downturns. This is the financial equivalent of burning your house down to stay warm.

The Discipline: True retirement wealth is created by preserving the engine. You must live from performance, not by consuming the source of funds. If your plan requires you to draw down your principal, you aren't retired; you're just on a long countdown to zero.

Is your principal working for you—or are you slowly spending it?

Discipline 2 : Protect Against Unnecessary Loss

Never Risk What You Cannot Afford to Lose.

How much of your retirement should be insulated from unnecessary loss?

Wall Street treats loss as a "price of admission." We treat it as an engineered failure. The Math of Recovery is brutal: a 50% loss requires a 100% gain just to get back to zero. While you are waiting years to "break even," you are losing the one thing you can never recover: Time.

The Discipline: Identify which assets must be moved from Assets at Risk (AAR) into Fully Performing Assets (FPA). Your "Floor" should be 0%, ensuring that when the market resets, your wealth stays exactly where it earned its last victory.

How much of your retirement could disappear in the next market correction?

Discipline 3 : Protect Forward Progress

Never Accept Unnecessary Step-Backs.

How many years could your current strategy lose during the next major downturn?

Major market declines don't just reduce your account value: they delay your life goals by years. Progress compounds when setbacks are minimized. This is the difference between a mountain climber who falls 10 feet and one who falls back to the base camp.

The Discipline: Wealth architecture is about maintaining forward momentum. By eliminating the "Dark Object" of major retractions, we ensure that every gain is a permanent floor for the next level of growth.

How many years would the next bear market cost you?

Discipline 4 : Protect Time

Time Is Your Most Valuable Asset.

How much future income is lost when time is lost?

Money can be recovered. Time cannot. According to the Wall Street Cycle, major retractions (averaging ~40%) occur every 5–7 years. Each of these major swings costs a minimum of 3.3+ years of lost time: time spent digging out of a hole instead of compounding toward your legacy.

The Discipline: We measure wealth by its Lifetime Usefulness. If your strategy "loses" a decade of compounding to market volatility, you have paid a tax that no CPA can recover. Protect your time by engineering a path that never resets the clock.

What is one lost year of compounding worth?

Discipline 5 : Increase Efficiency, Not Risk

Engineer Better Outcomes.

Can your retirement produce more without increasing your exposure to risk?

Increase Wealth Velocity

Better systems outperform higher risk.

Traditional "Single Pillar" assets: like stocks, standalone real estate, or basic savings: are outdated. They are the "pagers" of the financial world. Today, we use the Consolidation of Technology analogy. Just as your smartphone consolidated your camera, GPS, and phone into one device, Fully Performing Assets (FPA) consolidate 5–15 pillars of value (growth, protection, LTC, tax-free income) into one vehicle.

The Discipline: A better retirement isn't created by taking more risk; it's created by making every dollar work harder through coordination, tax planning, and Sequence of Return Margin.

Can your retirement produce more income without increasing risk?

Discipline 6 : Upgrade Your Thinking

New Results Require New Principles.

Are you solving retirement with yesterday's thinking?

The strategies that helped you accumulate wealth are often the exact same strategies that will destroy it in retirement. Accumulation is about "maybe" and "average returns." Retirement is about "certainty" and "actual income."

The Discipline: You must shift from being an investor to being an Architect. This requires moving away from the Orange (Tyranny of Urgent) or Red (More Risk is Better) personalities and becoming Green (Continuous Learning): using 0% floors, stripping fees, and following a rules-based plan.

Are you solving retirement with yesterday's thinking?

Discipline 7 : Preserve Every Victory

Turn Today's Gains into Tomorrow's Guarantees.

How much of your success is permanently protected for your future and family?

On Wall Street, your gains are "on paper" until you sell. On Your Street, we use Uncapped Gains (UCG) and Expanded Market Participation (EMP) to capture the upside, and then we lock it in.

The Discipline: As your wealth grows, you must strengthen the foundation. Every market victory should be converted into a permanent guarantee for your income and legacy. This is how you win the battle of Margin: the space between your source of funds and your use of funds.

Every financial victory should strengthen your future.

Lock in progress.

Increase your Guaranteed Present Value.

Increase your Guaranteed Future Value.

Increase your lifetime income.

Increase the wealth that remains for generations.

How much of your wealth is permanently positioned to benefit your family?

The 3% Success Truth vs. Engineered Certainty

Industry titans admit that only 3% of people are successful on Wall Street through sheer skill and luck. For the other 97%, the "Participation" model is a trap designed to extract fees while providing zero protection against wealth killers.

We don't play those odds. We use the Million Dollar Hour™ Income Analysis Comparison to shine a light on both the Shiny and Dark objects simultaneously. We look at the 5x Accumulated Loss Truth: the reality that $100k in lifetime contributions can lead to $500k in cumulative losses due to volatility and lost time.

Peace is the path, wisdom is the way.

Next Steps: The "Stop" Series

This post is the cornerstone of our "Stop" Series. Over the coming weeks, we will dive deep into each of these 7 Disciplines, showing you exactly how to stop the "leaks" in your plan and start engineering a blueprint that guarantees you won't outlive your money.

Your Money, Your Rules, In Your Time, On Your Street.

Are you ready to stop guessing and start engineering? Most people lose six or seven digits in their lifetime simply because they don’t know the value of what they are losing.

The Million Dollar Hour™ Forecast is a $995 professional engineering audit designed for the "Architect" persona. We don't offer "free cheese" for mice; we offer high-clarity architecture for Quiet Builders who want to know exactly where their plan leads.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Retirement isn't won by earning the highest return.

It is won by practicing the right disciplines consistently over time.

The Seven Disciplines of Retirement Wealth™ transform retirement planning from speculation into engineering.

They replace confusion with clarity.

Hope with strategy.

Risk with discipline.

And uncertainty with confidence.

Wealth is not measured by how much money you accumulate.

It is measured by how much lifetime income it produces and how much remains for the next generation.

Does your current retirement plan follow these seven disciplines—or does it depend on hope, market timing, and assumptions?

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now