Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

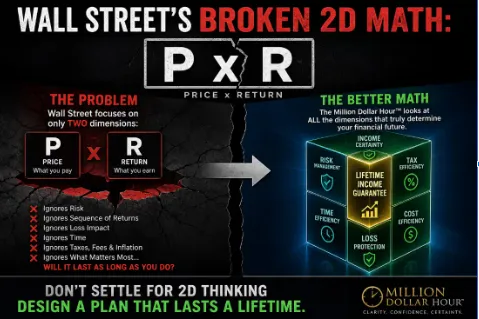

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Annuities Pros and Cons for Retirement Income Planning

The Tax-Free Finish Line: How to Stop Being a Silent Partner to the IRS

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

How to Stop Being a Silent Partner to the IRS. The Tax-Free Finish Line

Imagine you started a business with a partner. This partner never helps with the strategy. They don’t help you find customers, they don’t manage the staff, and they certainly don't chip in when the budget gets tight.

Yet, every time you make a profit, they show up and take 20%, 30%, or even 40% of the top line. They didn’t take a board seat, but they have a permanent lien on your revenue.

In the world of traditional retirement planning, that partner is the IRS. And if your money is sitting in a traditional 401(k) or IRA, you aren't just saving for your future: you are building a massive, growing account for a silent partner who gets paid first.

It’s time to find the finish line where that partnership ends.

The Rolodex in a SpaceX World

Most people nearing retirement are still using tax strategies from the 1980s. Back then, "tax-deferred" was the gold standard. The idea was simple: hide your money from the IRS today, let it grow, and pay them later when you’re in a "lower tax bracket."

That was a Rolodex strategy. We now live in a SpaceX world.

The reality of retirement income planning today is that tax rates are at historic lows, the national debt is at historic highs, and "later" is looking a lot more expensive than "now." When you defer taxes, you aren't avoiding them; you are just delaying the calculation of the bill. You are essentially giving the IRS a blank check and letting them fill in the amount twenty years from now.

If you want true financial freedom, you need to transition from Participation (hoping the tax rules stay in your favor) to Performance (engineering a tax-free outcome).

Compounding Efficiency: The Math of the Leak

In the Million Dollar Hour™, we often talk about Compounding Efficiency. This is the mathematical advantage of growing your wealth without a "tax leak."

When your money grows in a taxable account, you lose a portion of your gains every year to the IRS. Even in a tax-deferred account like a 401(k), the value of your compounding is being eroded because a third of that growth doesn't actually belong to you. It belongs to the Silent Partner.

A Fully Performing Asset (FPA) changes the physics of your balance sheet. By using the right institutional-grade structures, you can achieve tax-free accumulation and tax-free distribution. This means you compound 100% of your gains on 100% of your principal, 100% of the time.

When you eliminate the tax leak, your money doesn’t just grow: it heals.

Annuities: Pros and Cons for the Quiet Builder

If you’ve spent any time researching annuities pros and cons for retirement, you’ve likely run into a wall of conflicting information. Most Wall Street brokers hate them because they can’t trade them daily to generate fees. Most "free" internet gurus hate them because they don't understand the engineering.

Let’s look at the reality with institutional-grade precision.

The Cons (The Traditional Problems):

Complexity and Caps: Many retail annuities have "caps" that limit your upside to 3% or 4%, which barely keeps up with inflation.

Hidden Fees: Some products are layered with "Mortality and Expense" charges that act like a dripping faucet, draining your principal.

Liquidity Traps: Traditional products often lock your money away with zero flexibility.

The Pros (The FPA Solution):

The 0% Floor: In an FPA structure, you participate in market gains but never the losses. When the market drops 30%, you stay at 0%. You never have to do the "Math of Recovery."

EMP (Expanded Market Participation): We use multipliers that can give you 110% to 200% participation in market gains. If the market goes up 10%, your account could see an 11% to 20% gain: uncapped.

Guaranteed Lifetime Income: Unlike a stock portfolio that you hope doesn't run out, an FPA is contractually obligated to pay you for as long as you breathe.

The Power Pairs of Tax-Free Planning

To move toward the tax-free finish line, you have to choose which side of the "Power Pairs" you want to live on.

Certainty vs. Uncertainty: Do you want to know your tax rate in retirement, or do you want to hope the government doesn't change the rules?

Control vs. Dependence: Do you want to control your distributions, or be dependent on RMD (Required Minimum Distribution) schedules set by the IRS?

Increasing Income vs. Depleting Assets: Are you drawing down a taxable bucket that gets smaller every year, or are you utilizing an FPA designed to provide rising income that you can't outlive?

Why the Sooner You Start, the Better

Tax-free accumulation is a function of time. The longer you let your money compound without the IRS taking its cut, the more powerful the "Multi-Pillar" effect becomes. While a bank account or a stock is a "single-pillar" asset (it only does one thing), an FPA can provide 5 to 15 pillars of value: including growth, protection, and tax-free legacy.

Every year you wait to audit your tax margin is another year you are giving your Silent Partner a raise.

Audit Your Margin

The "Quiet Builders": the business owners, engineers, and executives we work with: aren't looking for "hot tips." They are looking for architecture. They want a plan that is engineered to work regardless of what happens in Washington D.C. or on Wall Street.

Stop being a silent partner to the IRS. Stop guessing at your future tax liability. It’s time to apply institutional-grade ALM (Asset Liability Management) to your personal balance sheet and find your finish line.

Peace is the path, wisdom is the way.

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now