Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Best Retirement Income Strategies: Stop Market Gambling

The 7 Reasons to Stop Gambling and Start Engineering Your Future Today

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

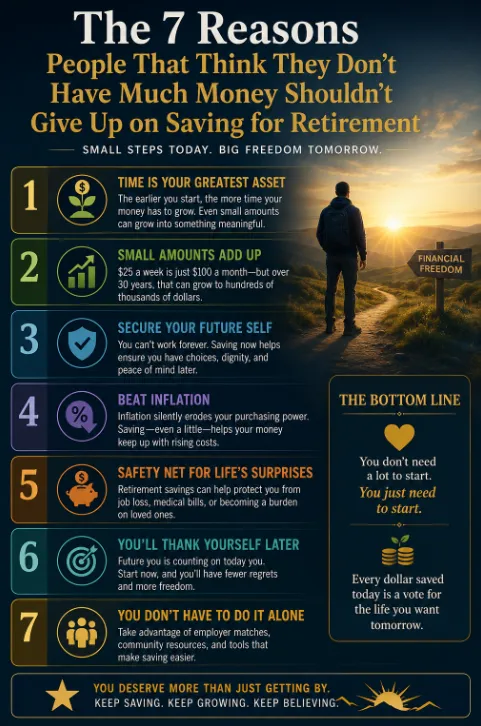

The 7 Reasons People Who Think They Are "Behind" Should Stop Gambling and Start Engineering Their Future Today

If you feel like you’re "behind" in the retirement race, you’re not alone. Most people in their 40s, 50s, and 60s feel a low-grade fever of financial fatigue. They look at the 401(k) balance, look at the S&P 500 headlines, and feel like they’re trying to run up a down escalator.

The common "Wall Street" advice? "Take more risk. You need to catch up. Buy the dip. Ride the volatility."

At Your Street Wealth, we call that "Participation." It’s a polite word for gambling. Wall Street loves it because they get paid whether you win or lose. But for the Quiet Builder: the successful, uneasy professional who wants certainty: gambling is a terrible retirement strategy.

You don’t need more "opportunity." You need better Engineering.

Here are the 7 reasons why you shouldn't give up: and why you should get out of the stock market casino today to start building on Your Street.

1. Time is Your Greatest Asset (The Multiplier)

Most people think of time as a countdown clock. We view it as a Compounding Efficiency multiplier.

The earlier you start, the better, but it is never too late to stop the bleeding. When you "participate" in the stock market, you are essentially resetting your clock every time there is a 10%, 20%, or 30% drawdown.

On Your Street, we focus on Forward Momentum. When you remove the possibility of market loss, every day becomes a day of growth. Time is only on your side if you aren't spending it trying to break even. Remember: Money can recover. Time never does.

2. Small Amounts Add Up (The Math of Recovery)

You might think, "I only have $25 or $50 a week to spare. Why bother?"

Here is the forensic truth: Small amounts add up to hundreds of thousands of dollars if you don't risk them. Wall Street thrives on the "Math of Recovery" because it’s hidden in plain sight.

Consider this: If you lose 30% in the market, you don't need a 30% gain to get back to even. You need a 42.8% gain just to see $0 again. If you lose 50%, you need a 100% gain. While you're waiting for that "recovery," your $50 a week is doing nothing but filling a hole.

On Your Street, we use Fully Performing Assets (FPA). Imagine a "Smartphone of Finance": a single vehicle that consolidates growth, protection, and tax-free income. When you save even small amounts in an FPA, you achieve Uncapped Gains (UCG) with a floor of 0%. You never have to do the "Math of Recovery" because you never go backward.

3. Secure Your Future Self (Dignity and Choice)

Retirement isn't about a "number" on a screen; it’s about Dignity.

You can't work forever. Eventually, your "human capital" (your ability to work) must be replaced by "financial capital." Saving now: even in small increments: is about ensuring that "Future You" has choices.

Do you want to depend on a volatile market that could drop 20% the year you decide to stop working? Or do you want an Engineered Path where your income is guaranteed? Engineering certainty provides peace of mind that a "hope-based" portfolio never can.

4. Beat Inflation: The Silent Tax

Inflation silently erodes your purchasing power. If you leave your money in a "Single Pillar" traditional asset like a standard bank account, you are losing. If you put it in the "Single Pillar" of stocks, you are gambling.

We shift our clients toward Multi-Pillar strategies. An FPA can provide 5–15 pillars of value (growth, LTC protection, tax-free access, etc.) in one vehicle. By using Expanded Market Participation (EMP), we can often apply a 110%–200% multiplier to market gains while maintaining a 0% floor. This is how you beat inflation without spinning sharp knives with your principal.

5. A Safety Net for Life’s Surprises

Traditional retirement plans are fragile. A medical bill or a job loss can force you to liquidate stocks at the worst possible time (the bottom of a crash).

Our Margin Audit™ identifies these "Sequence of Return" risks. By moving from Assets at Risk (Teens) to Fully Performing Assets (Foundation), you create a balance sheet that heals. You aren't just saving for a party at age 65; you’re building a fortress that protects you from job loss and medical expenses today.

6. You’ll Thank Yourself Later (No Regrets)

"Future You" is counting on "Today You." The most common regret we hear from retirees isn't "I wish I picked a better tech stock." It’s "I wish I had protected my time and wealth from unnecessary risk."

When you shift from a "Participation" mindset (gambling on headlines) to a "Performance" mindset (architectural design), you stop the "Greed/Fear" cycle. High greed signals high risk; high fear signals low risk. We help you exit that meter entirely.

7. You DON’T Have to Do It Alone

Wall Street wants you to think finance is too complex for you to understand, so you'll stay addicted to their daily research and "noise."

It’s a False Model. You can leverage employer matches, community resources, and professional engineering to build your street. You don't need a broker; you need an Architect.

Our Million Dollar Hour™ Forecast is designed to do the heavy lifting. In 60 minutes, we perform a forensic Volatility Recovery Analysis to show you exactly how much time and wealth you've lost to the market: and how to get it back.

The Path to Certainty

Stop chasing "opportunity" and start demanding Engineering.

Traditional Wall Street methods are like a "Rolodex in a SpaceX world." They were durable in the 80s, but they are inadequate for the speed and risk of today. You deserve a plan where you know the outcome before you start.

Peace is the path, wisdom is the way.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now