Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Delay: Why Later Doublings are the secret to Wealth

The Hidden Cost of Delay: Why Your Fourth and Fifth Doublings Are the Secret to True Wealth

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

Most people think the cost of waiting is just the return they miss this year. They look at a 5% or 7% market fluctuations and think, "I'll just catch the next wave."

They are wrong.

The true cost of delay isn't a missed percentage point. It is the compounding that never gets a chance to occur. It’s the "ghost wealth" that haunts your retirement because you didn't allow the math to finish its job.

At Your Street Wealth, we don’t look at your money through the lens of Wall Street’s "Participation" model: where you hope for a good year and pray for a low-loss decade. We look at it through Engineering.

If you want to build a skyscraper, you don't "participate" in a construction site; you follow a blueprint. The most important part of that blueprint is the foundation, because the highest floors (the ones with the view) cannot exist without it.

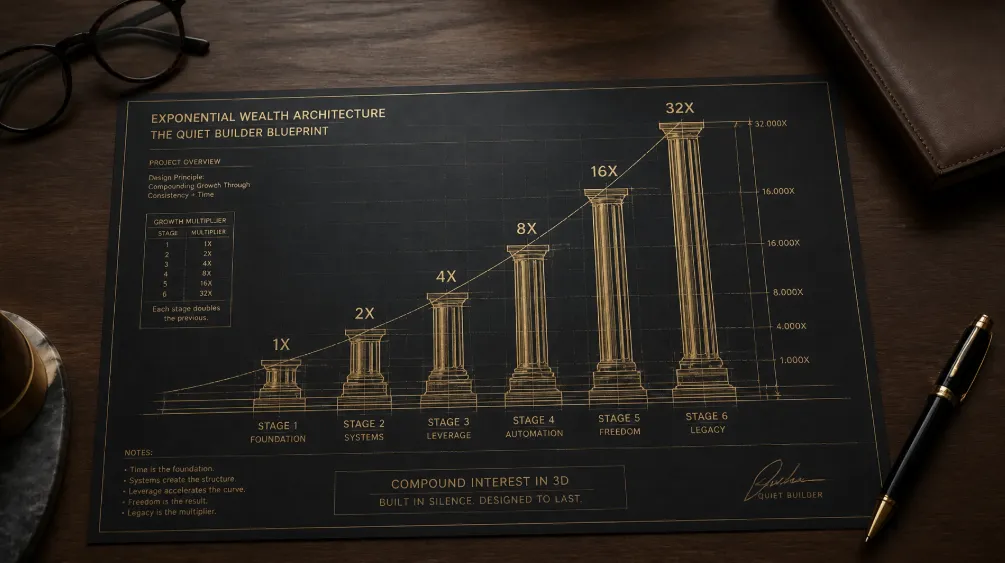

The Math of the 4th and 5th Doubling

Let’s frame this through the 5 W's & H: Who, What, When, Where, Why, and How.

Who builds wealth this way? Quiet Builders do. People who stop waiting for a giant pile of money to appear and start engineering from what they actually have.

What starts the process? Small amounts. That is all anyone has in the beginning. You do not build wealth by starting with large amounts. You build wealth by starting early enough for small amounts to reach the 4th and 5th doublings.

When should it start? As early as possible. The first move matters because the later doublings cannot happen until the first one begins.

Where should that money go? On Your Street: into rules-based, engineered, protection-first design that respects time and avoids unnecessary loss.

Why does this matter so much? Because the category of wealth is money you will never spend. Wealth is not the dollars you cycle through. Wealth is the money you preserve, compound, and keep outside the reach of market interruption.

How do you do it? Put as much as you can in the smallest increments as often as possible. Repeat the behavior. Protect the principal. Keep the clock running.

Let’s look at the math of reality. If your money earns a steady 5%, it doubles approximately every 15 years. (This is a simplified "Rule of 72" calculation for the real world).

Imagine you have a single $10,000 decision to make today. Here is what that journey looks like over a lifetime of Uninterrupted Time:

15 Years (1st Doubling): $20,000

30 Years (2nd Doubling): $40,000

45 Years (3rd Doubling): $80,000

60 Years (4th Doubling): $160,000

Stop and look at those numbers.

Most people focus on the first doubling. They get excited about the $10,000 they "made." But the wealthy: the Quiet Builders who understand financial architecture: focus on the fourth and fifth layers.

Why? Because in the final layer of this example, your money adds $80,000 in value ($80k to $160k). That single 15-year period creates more wealth than the first 45 years combined ($70k total gain).

The greatest growth occurs in the final layers of compounding. But here is the catch: those layers cannot begin until the first layer starts. Every year you wait to position your money correctly is a year you are effectively chopping off the top floor of your future wealth skyscraper.

A wealthy person does not wait for a windfall. A wealthy person builds from what they have, not from what they were given.

Participation vs. Engineered Performance

Wall Street wants you to stay in "Participation" mode. They use hidden complexity to keep you addicted to the daily news cycle. They want you focused on "price x return," ignoring the most critical dimension: Time (T).

At Your Street Wealth, we use 3D Math: Price x Return x Uninterrupted Time.

When you experience a 30% loss in the market, you don't just lose money. You lose the Time Compounding that money would have earned. This is the Math of Recovery. To recover from a 30% loss, you need a 42% gain just to get back to zero. While you are chasing that 42%, your neighbors who used Fully Performing Assets (FPA) were already moving toward their next doubling.

Audit the margin. If you are spinning sharp knives with high-risk "Single Pillar" assets like stocks or speculative real estate, you are risking the integrity of your entire timeline.

The Smartphone of Finance: Fully Performing Assets

Think of traditional financial products as a "Rolodex in a SpaceX world." Banks, stocks, and real estate are single-pillar assets. They do one thing, often with high fees and high risk.

Fully Performing Assets (FPA) are the "smartphone" of finance. Just as your phone consolidated your camera, pager, and TV into one device, an FPA consolidates 5–15 "pillars" of value: growth, protection, tax-free income, and LTC: into one vehicle.

By using an engineered strategy like the Million Dollar Hour™ Forecast, we can move you from the "False Model" of Wall Street (driven by fear and greed) to an Architecture of Certainty.

The Decision Not Made Today

The calendar never pauses. Compounding never catches up.

If you wait one more year to fix a "leaky" retirement plan, you aren't just losing 12 months of interest. You are delaying the start date of your final doubling. You are also increasing the odds that volatility interrupts the process before it fully matures.

This is the simple philosophy most people miss: your future is guaranteed to be greater if you never lose money. That is the whole point of engineering over participation. Protect the base. Preserve the timeline. Let the compounding do its full job.

There is a reason so many people say, "I wish I had started 20 years ago." What they are really saying is this: time is the most valuable commodity in wealth building. They are not just mourning missed returns. They are mourning missed doublings.

That realization should not lead to regret. It should lead to action. Once you know the path, start immediately. Do not delay another day. Do not give up another doubling cycle. Money can recover. Time never does.

This is where Assets at Risk (AAR) become dangerous. Market volatility can create a loss in one day that takes a year to recover. That is not just a bad month. That is a reset of your compounding clock. And for current retirees and future retirees alike, losses are the ultimate compounding killer.

If you want to reach those final doublings, you cannot afford to let Wall Street risk interrupt the design. You cannot build level 4 and level 5 wealth on a system that keeps knocking you back to level 2 and 3.

The Million Dollar Hour™ Question:

"If every $10,000 you fail to position today could cost you $100,000 to $160,000 later, what is the actual cost of waiting one more year?"

That is the true cost of delay. It’s the difference between a retirement where you are "hoping and praying" and one where you are living on a Guaranteed Path.

Mind Your Gap

Most pre-retirees have a "Volatility Recovery Gap": a period of time where their portfolio is simply trying to get back to where it was before the last market dip.

Stop chasing the "mice" of free advice and daily market tips. Be the Architect. Your money, by Your Rules, in Your Time, on Your Street.

Peace is the path, wisdom is the way.

Don't let the decision you didn't make today become the wealth you never experience tomorrow. Engineer your certainty now.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads — not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now