Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Math Matters Retirement Calculator is False Sense of Security

Math Matters: Why Your Retirement Income Calculator Is Giving You a False Sense of Security

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

Could You Be Receiving a False Sense of Security in Retirement Income

If you’ve spent any time planning for your future, you’ve likely seen it: the "Green Light." You plug your current savings, your age, and a hypothetical "7% average return" into a sleek online retirement calculator. A few seconds later, a bright green bar chart tells you that you’re on track. You’ll have $2.4 million by age 65, and you can safely withdraw $96,000 a year for life.

It looks like math. It feels like science. But for the "Quiet Builder": the engineer who demands precision or the business owner who knows that a 5% margin error can sink a company: this "math" feels... off.

And you’re right to be uneasy.

The truth is that traditional retirement income calculators are built on a foundation of Wall Street fictions. They rely on "averages" and "probabilities" that ignore the physics of how money actually works in the real world. At Your Street Wealth, we don’t believe in hoping for the best; we believe in Engineered Performance.

Here is why your retirement calculator is lying to you, and how to start using the "Math of Recovery" to build a plan that actually holds water.

The Arithmetic Trap: Why Averages Are Not Actuals

Most calculators ask you for an "expected annual return." You might put in 7% or 8% because that’s the historical average of the S&P 500. The calculator then grows your money in a straight line, like a ladder leaning against a wall.

But the market doesn't move in a straight line. It moves like a rollercoaster.

Imagine two years in the market:

Year 1: Your portfolio drops by 50%.

Year 2: Your portfolio gains 50%.

The "average" return is exactly 0% ((-50 + 50) / 2). A traditional calculator would tell you that if you started with $100,000, you still have $100,000.

But look at the actual math:

Year 1: $100,000 drops to $50,000.

Year 2: $50,000 grows by 50% ($25,000) to $75,000.

You didn't break even. You lost $25,000. To get back to your original $100,000, you didn't need a 50% gain; you needed a 100% gain.

This is what we call The Math of Recovery. Wall Street loves to talk about "Participation" in market gains, but they rarely mention the "Volatility Drag" that eats your actual compounding efficiency. When you lose 30%, you don’t need 30% to recover; you need 42%. If you don't account for this, your "green light" is actually a flickering warning bulb.

Sequence of Returns: The Order Matters More Than the Number

For a Quiet Builder, the most dangerous variable in a retirement calculator isn't the average return: it's the Sequence of Return Margin.

When you are in the "Accumulation Phase" (saving money), the order of returns doesn't matter much. But the moment you enter the "Distribution Phase" (taking income), the order of returns is everything.

If the market drops 20% in your first two years of retirement while you are also withdrawing 4% for living expenses, you are effectively "cannibalizing" your principal. You are selling shares at a discount to pay for groceries. This creates a hole so deep that even a massive bull market five years later might not be enough to dig you out.

Traditional calculators use "Monte Carlo simulations," which is a fancy way of saying they run 1,000 guesses and tell you that you have a "90% probability" of success.

Ask yourself: As an engineer or a business owner, would you walk across a bridge that had a 10% chance of collapsing? Would you fly in a plane with a 90% "probability" of landing safely?

Of course not. You want Certainty. You want Guarantees. You want a plan that is contractual, not projected.

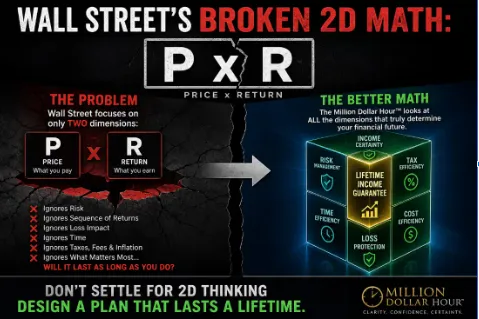

Single Pillar vs. Multi-Pillar: The Smartphone of Finance

Traditional financial planning relies on "Single Pillar" assets.

Banks: Liquid, but zero growth and taxable.

Stocks: High growth potential, but high risk of loss (The Math of Recovery trap).

Real Estate: Great cash flow, but illiquid and high maintenance.

These are like the gadgets of the 1990s: the pager, the Walkman, and the bulky video camera. They each do one thing, but they don't talk to each other, and they create a "Rolodex in a SpaceX world" strategy.

At Your Street Wealth, we focus on Fully Performing Assets (FPA). We think of FPA as the "Smartphone of Finance." Just as a smartphone consolidated ten different devices into one, an FPA consolidates 5 to 15 "pillars" of value into a single vehicle:

Uncapped Gains (UCG): You participate in the market's upside.

0% Floor: You have a contractual guarantee that you will never lose a dime due to market volatility. When the market drops 30%, your statement says 0%. Your compounding is never interrupted.

Expanded Market Participation (EMP): Some strategies allow for a 110% to 200% multiplier on those gains.

Tax-Free Income: Engineered to bypass the "Invisible Lien" the IRS has on your traditional IRA.

serving as the foundation for a secure retirement.")

From "Participation" to "Performance"

Wall Street wants you to "participate" in the market. "Participation" is just another word for gambling with your time. When the market goes down, Wall Street still gets paid their fees. You are the one who loses the time. And while money can recover, time never does.

We shift the conversation from Participation to Engineered Performance. This is rooted in institutional-grade Asset Liability Management (ALM): the same math used by major banks to ensure they stay solvent for centuries.

Instead of "hoping" the market behaves, we perform a Margin Audit™. We look at the micro-margins of your plan: the fees, the taxes, and the volatility leaks: and we plug them. We calculate your Compounding Efficiency to ensure that every dollar you have is working at its maximum potential without being subject to "spinning sharp knives" (interest rate ripples and market crashes).

The Million Dollar Hour™ Forecast

If you are a Quiet Builder between the ages of 45 and 75, you don't need another generic calculator. You need a blueprint.

The Million Dollar Hour™ Forecast is a $995 engineering audit designed for those who value clarity over noise. In 60 minutes, we don't give you a "probability." We provide a personalized, guaranteed path to wealth accumulation and lifetime income.

During this session, we:

Calculate Years Lost: We show you exactly how much time and wealth you've already lost to Wall Street volatility.

Audit the Margin: We identify the hidden "leaks" in your current strategy.

Engineer Certainty: We present a path where your income is designed, not dependent on the whims of a "False Model" driven by greed and fear.

We aren't looking for "free" seekers. We are looking for those who understand that Peace is the path, and wisdom is the way. We write for the person who wants to say, "Your Money, Your Rules, In Your Time, On Your Street."

Stop Guessing. Start Engineering.

The "math" on your screen might look good today, but if it doesn't account for the Math of Recovery or Sequence of Return Risk, it’s a house built on sand. It’s time to unlearn the myths of Reagan-era banking and move toward a modern, multi-pillar architecture.

Protect your time. Protect your wealth. Audit the margin.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now