Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

The Soft Landing Lie: Best Retirement Income Strategies

The Soft Landing Lie: Why Your Retirement Needs an Upward Trajectory

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

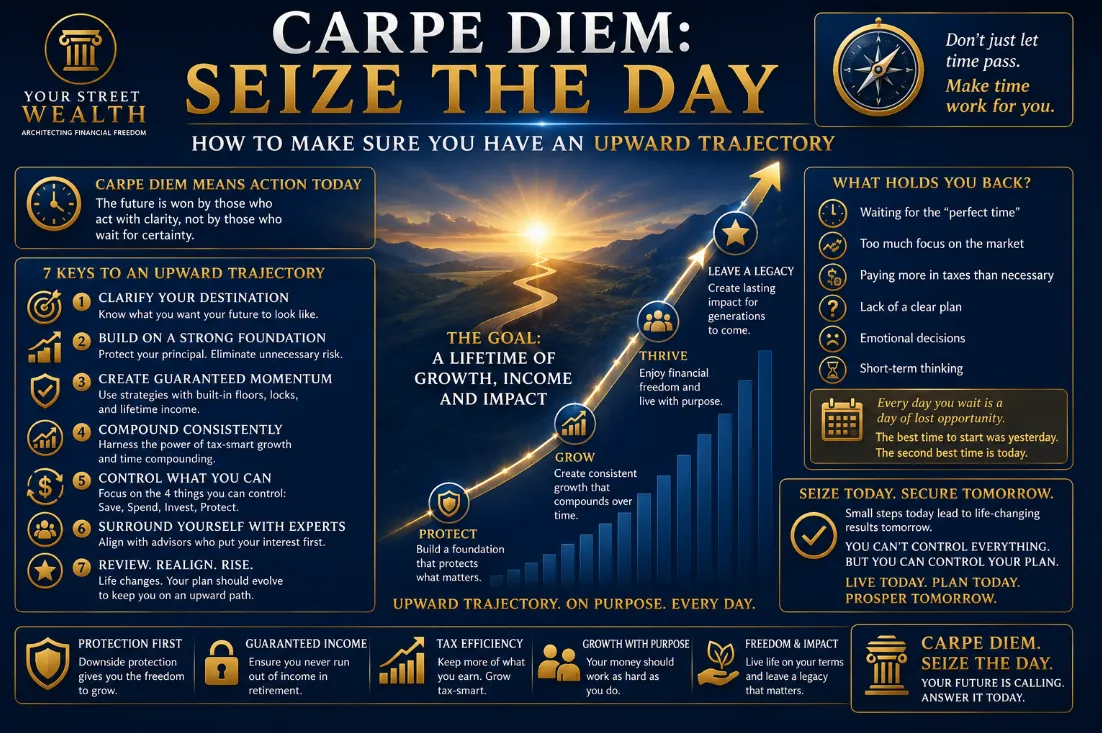

![[HERO] The Soft Landing Lie: Why Your Retirement Needs an Upward Trajectory](https://cdn.marblism.com/Nqa8bbTTWkl.webp "[HERO] The Soft Landing Lie: Why Your Retirement Needs an Upward Trajectory")

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The Gravity Trap: Why Wall Street’s ‘Soft Landing’ is Just a Slow-Motion Crash

You’ve heard the phrase a thousand times on CNBC: the "Soft Landing."

The talking heads in expensive suits want you to believe that if the economy just touches down gently: like a Boeing 747 grazing the tarmac: everything will be fine. Your 401(k) will stay intact, inflation will go on a diet, and you can finally stop doom-scrolling the tickers every morning.

But here’s the cold, hard truth that Wall Street won’t tell you: A "landing" is still a downward trajectory.

Whether you land softly or sink like a stone, you are losing altitude. In the world of retirement, altitude isn’t just a number on a screen; it’s your time, your freedom, and your ability to "Carpe Diem" without looking over your shoulder for the next bear market.

At Your Street Wealth, we don’t want you to "land." We want you to ascend. If you’re a Quiet Builder who has spent thirty years climbing the mountain of success, the last thing you need is a "soft landing" that leaves you stuck at basecamp while the cost of living continues to skyrocket.

The Financial Fatigue of "Participation"

Most people are exhausted. Not from working hard: Quiet Builders thrive on work: but from the uncertainty.

This is what we call Financial Fatigue. It’s the mental drain of participating in a system where you have all the risk but none of the control. You’ve been told to "ride out the market," which is essentially Wall Street code for "stay in the casino so we can keep charging you fees while you lose sleep."

Traditional retirement planning is a "Participation" model. You participate in the gains, but you also participate in the bloodbath. This creates a jagged, heart-monitor-style graph that forces you to constantly calculate how much you can afford to lose today before it ruins your tomorrow.

The Math of Recovery: Why "Breaking Even" is a Lie

Let’s talk about the Math of Recovery. This is where the "Soft Landing" narrative completely falls apart.

If the market drops 30%: a common occurrence in the "Wall Street Fugazi": you don’t just need a 30% gain to get back to where you were. You need a 42% gain just to see the surface again. If you lose 50%, you need a 100% gain to break even.

When you’re 35, you have time to wait for those miracles. When you’re 65, time is the one asset you cannot afford to waste. Money can recover. Time never does.

Wall Street treats your retirement like a game of probabilities. They tell you there’s an "80% chance" your money will last. Would you board an airplane if the pilot said there was an 80% chance of landing safely? Of course not. You’d demand Engineering over Odds.

Carpe Diem: Seizing the Day Without Sinking the Future

The mission of Your Street Wealth is simple: Seize the Day.

But you can’t truly seize the day if you’re worried about "uncontrollable losses." How do you enjoy a Tuesday morning round of golf if the S&P 500 just wiped out your planned Europe trip for next summer?

To live a "Your Street" life, you have to eliminate the downward trajectory. You need to build your wealth on a ladder, not a bungee cord. By using Engineered Performance instead of "Market Participation," we ensure that every step you take is a step up.

When you eliminate the possibility of a 0% year (or worse, a -30% year), you create a floor. On Your Street, your floor is yesterday’s ceiling. That is how you find an upward trajectory that doesn't exhaust you.

The "Rolodex in a SpaceX World" Problem

Many Quiet Builders are still using financial strategies designed in the 1980s. These are what we call Single-Pillar Assets.

Banks: Low return, high inflation risk.

Stocks: High volatility, no guarantees.

Real Estate: High tax, high maintenance, low liquidity.

Relying on these single-use tools is like trying to manage your life with a Rolodex and a pager in a SpaceX world. It worked once, but it’s inadequate for the speed and risk of the modern age.

The alternative? Fully Performing Assets (FPA).

Think of an FPA as the "smartphone" of finance. Just as your phone consolidated your camera, GPS, computer, and phone into one device, an FPA consolidates 5 to 15 "pillars" of value into one vehicle. We’re talking about Uncapped Gains (UCG) and Expanded Market Participation (EMP): where you can get a multiplier on the market’s growth without ever participating in its losses.

Imagine a world where your "worst-case scenario" is 0% and your "upside" is a 110% to 200% multiplier on the market’s positive moves. That isn’t a fairy tale; it’s institutional-grade Asset Liability Management (ALM) applied to your personal balance sheet.

The Margin Audit™: Finding the Leaks

Before you can climb the mountain, you have to stop the bleeding. Most retirement plans are riddled with "wealth leaks": hidden fees, unnecessary taxes, and the "Volatility Tax" (the cost of recovering from market drops).

We use a process called The Margin Audit™ to scrutinize every dollar. We aren't looking at macro headlines; we’re looking at micro margins.

Where is your compounding efficiency being robbed?

How much is your "Sequence of Return Margin" being squeezed by market timing?

Are you paying for "Participation" when you should be paying for "Performance"?

By auditing the margin, we reclaim the lost wealth that was previously being siphoned off by the Wall Street machine.

(Suggested Visual: A professional architect reviewing a blueprint (The Margin Audit) vs. a gambler throwing dice at a table (Wall Street Participation))

From Uncertainty to Engineered Certainty

The "Soft Landing" is a myth because it relies on factors you can’t control: the Fed, global conflict, and the whims of high-frequency trading algorithms.

Your Street Wealth is about shifting from Dependence to Control.

Wall Street: "We hope the market goes up so you can retire."

Your Street: "We have engineered a contractual guarantee so you will retire."

This is the difference between Knowing and Hoping. It’s the difference between a "Soft Landing" (downward) and an "Ascent" (upward).

If you are tired of spinning sharp knives and hoping you don't get cut, it’s time to unlearn the myths of the "Participation" model. You don't need more "research" or more "diversification" into the same risky assets. You need a better Architecture.

The Million Dollar Hour™: Your Engineering Blueprint

We don't offer "free consultations" because we don't offer "free cheese." We aren't here to sell you a product; we’re here to engineer a result.

The Million Dollar Hour™ is a premium, $995 deep-dive engineering session designed specifically for high-intent Quiet Builders. Guaranteed to show you how to Increase your account value by $20,000 - $100,000 immediately.In sixty minutes, we perform a total Margin Audit of your current trajectory.

We don't just show you where you've been; we show you exactly where your current plan leads. If there's a gap between your current path and the life you want to live, we identify it and close it using modern banking architecture.

This session is designed to last for life. It is the moment you stop "participating" in Wall Street's games and start "performing" on Your Street.

Protect your time. Engineer your certainty. Seize your day.

Because at the end of the day, it's your money, your rules, in your time, on your street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now

Check out the Retirement Blueprint