Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Tripling: The Math Wall Street Hopes You Never Do

The Rule of Tripling: The Math Wall Street Hopes You Never Do

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Why is it called Rule of 115 to triple your money?

Most people know the Rule of 72. It’s that handy little mental shortcut that tells you how long it takes for your money to double. If you earn 10%, your money doubles every 7.2 years. If you’re stuck with 2% in a traditional bank account, you’re looking at a 36-year wait just to see your $10,000 turn into $20,000.

At Your Street Wealth, we call that the Rule of 36, and for a "Quiet Builder" looking to actually retire, it’s a recipe for running out of time.

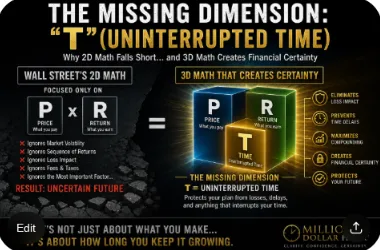

But there’s a deeper, more powerful math that Wall Street conveniently forgets to mention: The Rule of Tripling. The rules often have numbers because the power of TIME is MAGIC either for you or against you. Wall St uses TIME against you.

Why is it unknown? Because it doesn’t happen on Wall Street. On Wall Street, gains are frequently "taken back" by the market. And as any engineer will tell you, a system that resets its own progress isn’t a growth engine: it’s a hamster wheel.

The Quiet Builder’s Final Act

Let’s make this math real for the people who actually need it most.

If you’re between 45 and 65, these are not random years. These are your most critical compounding years. This is the stretch where the finish line comes into view, and small interruptions create big consequences.

Here’s what the Rule of Tripling (115) looks like when you protect the finish line:

If your money compounds at 11.5% for 10 uninterrupted years, then:

$100,000 becomes $300,000.

$300,000 becomes $900,000 in 20 years.

$900,000 becomes $2,700,000 in 30 years.

That is the math of a strong final act. Not flashy. Not speculative. Just disciplined, uninterrupted compounding doing heavy lifting over the exact years that matter most.

Now here’s the problem. Wall Street does not offer 11.5% uninterrupted over 10 years. It offers "Participation." It offers the chance to go up 30% one year, lose 20% the next, and call the whole thing "long-term investing."

That is not performance. That is a reset button.

In the Wall Street world, a 20% loss isn't just a 20% setback. It’s a Volatility Recovery Analysis nightmare. To recover from a 20% loss, you don't need a 20% gain: you need a 25% gain just to get back to zero. If you lose 30%, you need a 42% gain.

Every time the market "loses its lunch," it resets the math and steals the years you can least afford to lose. Protect the finish line. Protect your time.

Participation vs. Engineered Performance

Wall Street operates on a "False Model" driven by the Greed/Fear meter. When greed is high, they tell you to "participate" in the upside. When fear is high, they tell you to "ride it out."

But "riding it out" is just another way of saying "losing time."

Imagine if you used the Rule of Tripling instead. If you are able to earn 11.5% per year for 10 years, your money triples.

$100,000 becomes $300,000.

$300,000 becomes $900,000.

$900,000 becomes $2,700,000.

In just 30 years of engineered, uninterrupted growth, you’ve gone from $100k to nearly $3 Million.

If this happened on Wall Street, people would be shouting from the rooftops. But it doesn't happen there. Wall Street has no floor. It cannot guarantee that it won't take back your gains. It forces you into a Sequence of Returns Risk where a few bad years at the start of your retirement can liquidate your entire legacy.

The Smartphone Analogy: Fully Performing Assets (FPA)

Remember the world before the smartphone? You had a camera, a pager, a calculator, and a brick-sized phone. These were "single-pillar" tools. If you wanted to take a photo, you needed the camera. If you wanted to talk, you needed the phone.

Traditional assets: Banks, Stocks, and Real Estate: are the "Rolodex" of the financial world. They are single-pillar assets.

Banks: Provide safety but 0% growth (The Rule of 36).

Stocks: Provide growth but 0% protection (The "Lose Your Lunch" model).

Real Estate: Provides equity but carries high fees and low liquidity.

In a SpaceX world, you need a Fully Performing Asset (FPA). This is the "smartphone" of finance.

An FPA is a multi-pillar asset that consolidates 5–15 pillars of value into one vehicle. It offers Uncapped Gains (UCG) and Expanded Market Participation (EMP). We’re talking about 110% to 200% multipliers on the market’s upside, with a contractual 0% floor.

When the market goes up 10%, your EMP might turn that into an 11% or 20% gain. When the market drops 30%? You stay at 0%. You don't lose money, and more importantly, you don't lose time.

How Much Do I Need to Retire? (The Wrong Question)

Most people asking "how much do I need to retire?" are looking for a magic number. But a number without a system is just a hope.

If your "number" is $2 Million, but that money is sitting in a volatile market, your actual income is dependent on the whims of Wall Street. You aren't retired; you're just a professional gambler who stopped working.

True retirement income planning isn't about predicting the future value of a portfolio that you can't control. It’s about Engineering Certainty.

It’s about moving from:

Uncertainty to Certainty (Knowing vs. Hoping)

Probabilities to Guarantees (Contractual vs. Projections)

Dependence to Control (Controlling outcomes vs. Depending on markets)

At Your Street Wealth, we use a process called the Margin Audit™. We look at your current plan and identify the "leaks": the fees, the taxes, and the market volatility that are resetting your compounding clock.

We don't chase "opportunities." We build architecture.

The Million Dollar Hour™ Forecast

Peace is the path, wisdom is the way.

For the "Quiet Builder": the successful, yet financially fatigued professional: the noise of Wall Street is exhausting. You’ve spent your life building your business or your career. You’ve taken enough risks. Retirement shouldn't be another one.

The Million Dollar Hour™ Forecast is our premium engineering session. In 60 minutes, we don't just "review" your stocks. We perform a Volatility Recovery Analysis. We show you exactly how many years you've lost to market resets and how to pivot to a guaranteed retirement income strategy.

We use institutional-grade banking architecture to ensure your money is working for you, on your terms, on your street.

No participation. Just ownership. No work required: just the inspection of performance.

Audit the Margin. Protect Your Time.

Wall Street wants you to believe that finance is complicated so you’ll keep paying them to "manage" the chaos. But the math of the Rule of Tripling is simple.

If you eliminate the losses, you accelerate the gains. If you protect the floor, the ceiling takes care of itself.

Stop chasing "Free Cheese" and start investing in true financial architecture. Your money can recover from a dip, but your time never does.

Engineer your certainty today.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now

Check out the Retirement Blueprint