Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Why Time, Not Money, Is Your Biggest Retirement Risk

The Silent Thief: Why Time, Not Money, Is Your Biggest Retirement Risk

The Great Misconception

Most people believe the greatest threat to their retirement is losing money.

They watch the tickers. They check their apps. They sweat the red days and breathe a sigh of relief when the green days return. They assume that as long as the account balance eventually creeps back to where it was, the damage is healed.

It isn't.

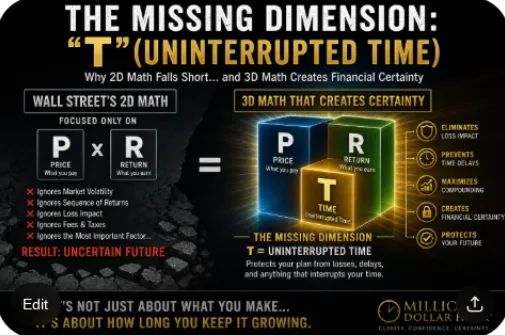

The biggest threat to your retirement isn't losing money. It’s losing time.

Money can be recovered. Time cannot. When your portfolio takes a 20% or 30% hit, Wall Street tells you to "stay the course." They tell you "it's just a paper loss." What they don't tell you is that your wealth just stopped moving forward. It didn't just pause; it began a grueling, multi-year hike just to get back to the starting line.

While you were busy "breaking even," your peers with engineered certainty were compounding. This is the Math of Recovery, and it is the silent thief of American wealth.

The Math of Recovery: Why "Breaking Even" is a Failure

Let’s look at the cold, hard numbers. Wall Street loves to talk about "average returns." Average returns are a myth used to mask the reality of geometric losses.

If you have $1,000,000 and you lose 30%, you have $700,000.

To get back to $1,000,000, you don’t need a 30% gain. You need a 42.8% gain.

Think about how long it takes to achieve a 42% return in a typical market. Two years? Four? Six? That is the "Time Lost." During those years, you aren't building wealth; you are healing a wound.

In the world of Your Street Wealth, we call this a lack of Compounding Efficiency. Every market retraction steals your most precious asset: the years your money should have been working at its full potential.

Participation vs. Engineered Performance

The traditional Wall Street model is built on Participation. You are a passenger. You "participate" in the ups, and you "participate" in the downs. This is gambling disguised as strategy. It relies on hope, macro headlines, and the belief that the "False Model" of daily research and addictive buying/selling will somehow lead to peace.

We reject Participation in favor of Engineered Performance.

Architecture is a designed process that grows and heals. Participation is a false architecture that extracts value and creates hidden harm through fees, taxes, and volatility.

When you move from being a "Participant" to an "Architect," you stop hoping and start knowing. You move from the "Teens" phase of the Asset Pyramid (Assets at Risk) to the Foundation (Fully Performing Assets).

The Asset Pyramid

NPA (Non-Performing Assets): Infants/Emergency funds. Necessary, but they don't build the future.

AAR (Assets at Risk): The traditional Wall Street "Teens." They are volatile, moody, and can disappear when you need them most.

FPA (Fully Performing Assets): The Foundation. This is where engineered certainty lives.

The Smartphone Analogy: Consolidation of Technology

Why are you still using a financial "Rolodex" in a SpaceX world?

In the 1990s, you had a pager, a camera, a calculator, a map, and a phone. Today, you have a smartphone. It’s a Multi-Pillar device. It consolidated dozens of single-use tools into one high-performance machine.

Traditional assets like stocks, real estate, and bank accounts are Single-Pillar assets.

Banks: Liquid, but low growth.

Stocks: Growth potential, but high risk and high fees.

Real Estate: Appreciation, but zero liquidity.

Fully Performing Assets (FPA) are the "smartphones" of finance. They provide 5–15 pillars of value: including growth, protection, tax-free income, and LTC benefits: inside a single vehicle. They offer Uncapped Gains (UCG) and Expanded Market Participation (EMP).

Imagine a 10% market gain. In a traditional account, you get 10% (minus fees and taxes). With EMP, that same 10% can be engineered into an 11% or even 20% gain, all while maintaining a 0% floor.

Your Street math is simple: -30% to +30% (Wall Street) versus 0% to +30% (Your Street). Which one protects your time?

The Margin Audit™: Identifying the Leaks

Most "Quiet Builders" are successful but financially fatigued. They’ve done the work, but they feel the "Sequence of Return Margin" shrinking. They know that a major market correction five years before or after retirement could permanently alter their lifestyle.

This is where the Margin Audit™ comes in.

We don't look at "average returns." We look at Volatility Recovery Analysis. We calculate exactly how many years have already been lost to market noise and hidden fees. We look for the "interrupted gains" that prevent your wealth from reaching its true destination. For a deeper look at the decision-making metrics behind this process, read The 5 Numbers That Will Determine Your Retirement Future.

Audit the margin. Protect your time. Engineer certainty.

A Tale of Two Paths

Every retirement plan eventually becomes a fork in the road.

One path is Participation / Wall Street. It leaves a person walking in an unknowing life of lack and uncertainty, driven by the cycle of fear and greed. You watch the headlines. You react to red screens. You wait for recoveries. You hope probabilities become promises. You live with uncertainty because the system depends on it.

The other path is Engineering / Your Street. It leads to a life of abundance, walking in peace and confidence. You stop chasing noise. You start following architecture. You trade projections for rules, volatility for stability, and guesswork for design.

This is the real choice:

Certainty vs Uncertainty: Know where your plan leads instead of hoping it works.

Guarantees vs Probabilities: Use contractual strength instead of market projections.

Control vs Dependence: Engineer outcomes instead of depending on Wall Street’s False Model.

Growth Without Loss vs Growth With Loss: Protect compounding instead of resetting the clock.

Increasing Income vs Depleting Assets: Build rising income instead of spending down principal.

Time Compounding vs Time Lost: Protect the one asset you can never replace.

This is not just about accounts. It is about how you live. One road keeps you financially fatigued. The other lets you walk forward with clarity. One road trains you to participate. The other teaches you to engineer. One road feeds fear and greed. The other builds peace and confidence.

Choose the road that protects your time. Choose the road that protects your wealth. Choose the road that lets you live on purpose, not on edge.

The Million Dollar Hour™ Forecast

We do not offer "free consultations." We offer a high-friction, high-clarity professional service for those willing to pay for a scrutinized, certain plan.

The Million Dollar Hour™ ($995) is a 60-minute session where we act as the architects of your future. We use Asset Liability Management (ALM) principles: the same ones used by major banks: to forecast your path.

In this hour, you will unlearn the myths of the 1980s and learn fundamental financial architecture. You’ll discover:

How much income your assets can realistically produce (The Truth, not the Projection).

Your actual Sequence of Return Margin.

How to achieve Growth Without Loss.

The path to an Increasing Income vs. a depleting asset base.

We use the 7-Vector Wealth Navigation System™ to map your Protection, Time, Income, and Legacy. We find the "Reality Axis" of your returns, stripped of Wall Street’s hidden complexity.

Peace is the Path, Wisdom is the Way

The greatest risk is not the market. The greatest risk is what you don't know is costing you.

Every year you delay is another year of compounding that is permanently deleted from your life. You can earn more money, but you cannot buy back 2026. If you already feel like you’re running up a down escalator, check out 7 Reasons to Stop Gambling.

It is time to shift from "Hoping" to "Knowing." It is time to stop being a "Participant" in a rigged game and start being the "Architect" of your own street.

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now