Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Protect Retirement Savings from Market Crash and Volatility

The Overriding Worry: Why Wall Street Wants You to Ignore the Math

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

![[HERO] The Overriding Worry: Why Wall Street Wants You to Ignore the Math](https://cdn.marblism.com/H0xP-G9YjJo.webp "[HERO] The Overriding Worry: Why Wall Street Wants You to Ignore the Math")

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The $2.6 Million Difference: Why Wall Street Wants You to Ignore the Math

Do you have "the itch"?

You know the one. It’s that nagging urge to unlock your phone, open your brokerage app, and check your balance. You did it yesterday. You did it this morning. You’ll probably do it again before dinner.

Wall Street loves that itch. In fact, they spent billions of dollars designing a system that keeps you scratching it. They call it "staying informed," but in reality, it’s a symptom of a deep, underlying uneasiness. It’s the overriding worry that the "math" you’ve been told, the 7% or 8% average return, isn't actually working for you.

Deep down, you know something is off. You’ve been a "Quiet Builder" for decades. You’ve worked hard, lived below your means, and stayed the course. Yet, every time the market hiccup, a "routine" 10% or 20% drop, you feel like you’re running on a treadmill that’s slowly sliding backward.

Here is the truth: Wall Street wins when you lose. They win on the fees, the churn, and the complexity. And they stay in business by making sure you never sit down to do the real math.

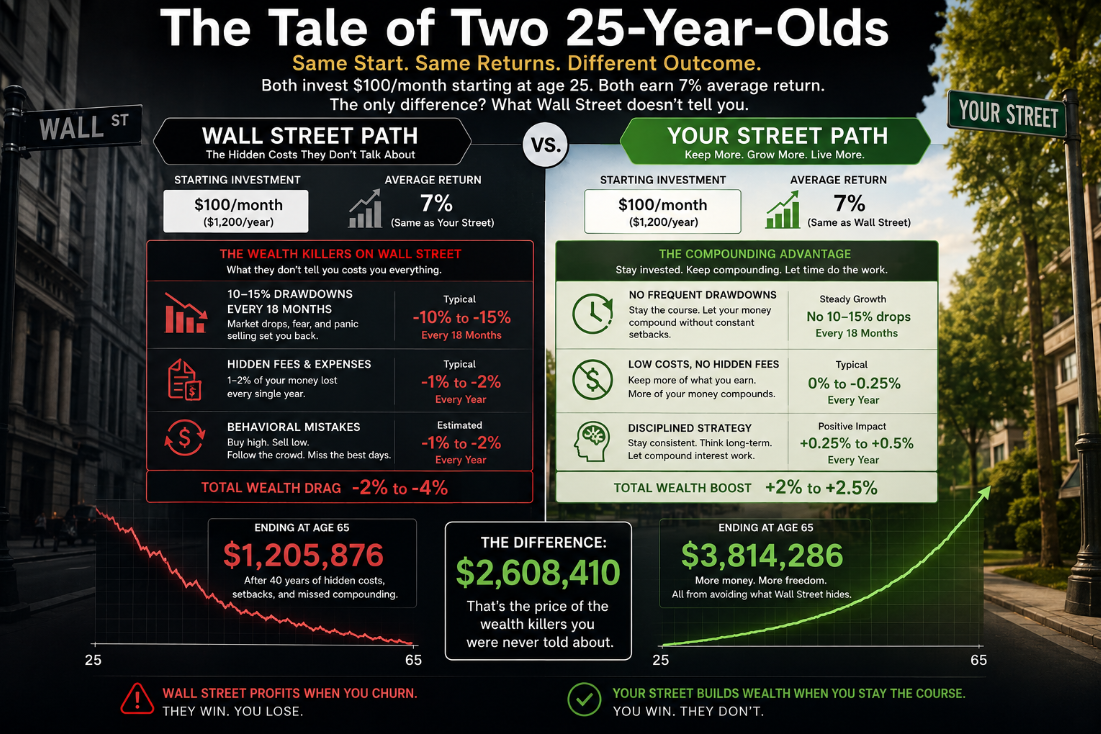

The Tale of Two 25-Year-Olds (The Math Wall Street Hides)

Let’s strip away the jargon and look at a simple scenario. Imagine a 25-year-old who decides to start building wealth. They open an account with $100 and commit to depositing $100 every single month. They are told to expect an "estimated 7% per year growth." The math comparing these two 25-year-old scenarios was calculated using our proprietary Million Dollar Hour™ Forecasting Tool, which is designed to show, with precision, how these outcomes can play out in a real person’s financial life.

Scenario A: The Wall Street "Participation" Model

In this world, our young saver is told to "ride the waves." They are told that volatility is the price of admission. Every 18 months or so, the market takes a routine 10% to 20% dip. On paper, their "average" return might look like 7% over forty years, but the actual sequence of those returns is a nightmare.

Because of those periodic resets, the moments where the market gives back two years of gains in two months, the math breaks. By the time this person reaches retirement age, they haven't just lost sleep; they’ve lost approximately $200,000 in potential gains.

The result? They end up with a balance of roughly $80,000.

Wall Street calls this "market participation." I call it a wealth assassin.

Scenario B: The Your Street "Engineered" Model

Now, imagine that same 25-year-old uses a Fully Performing Asset (FPA), what we call the "Smartphone of Finance." They still get that 7% growth, but it’s engineered for stability. There are no 20% drops. There are no "resetting the clock" moments.

By age 52, their balance is a modest $83,000. It doesn't look like a fortune yet. But because they never lost a dime to market volatility, the power of Compounding Efficiency takes over.

The final ending balance? Approximately $2.75 million.

Read those numbers again. $80,000 versus $2,750,000.

Same monthly contribution. Same "average" percentage. But one person ends up with a hobby, and the other ends up with a legacy. This is the difference between Participation and Performance.

Why You Check Your Account Every Day

The reason you check your account daily isn't because you're greedy; it's because you lack Certainty.

Wall Street operates on a "False Model" driven by the Greed/Fear meter. When the meter swings toward greed, they sell you "upside potential." When it swings toward fear, they tell you to "hold on for the long term."

This is a Single-Pillar Model. Traditional assets like stocks, bonds, or even some real estate are single-pillar. They provide one thing (usually growth), but they lack the structural support to handle a storm. If that one pillar cracks, the whole roof comes down.

When you use Assets at Risk (AAR), you are essentially spinning sharp knives. You can do it for a while, but eventually, the physics of the market will catch up to you. This is why you’re uneasy. You’re waiting for the knife to drop.

The Math of Recovery: Why "Average" is a Lie

One of the biggest myths Wall Street uses to keep you trapped is the "Average Return" lie.

If you have $100,000 and you lose 30%, you have $70,000. To get back to $100,000, do you need a 30% gain?

No. You need a 42.8% gain.

Money can recover, but time never does. Every time you experience a "routine" market crash, you aren't just losing money; you’re losing the time it takes to get back to even. We call this the Volatility Recovery Analysis.

If you are 60 years old and your portfolio takes a 20% hit, you don't just need the market to go back up 25% to break even. You need to account for the inflation, the fees, and the fact that you are now one or two years closer to needing that income. You have lost your Sequence of Return Margin.

Unlearning the "Rolodex" Strategy

Most retirement plans today are the financial equivalent of a Rolodex in a SpaceX world. They were durable in the 1980s, but they are inadequate for the speed and technical demands of a modern retirement.

Back then, you could buy a bond, get a decent yield, and call it a day. Today, you are forced into the "casino" of the stock market just to try and keep up with inflation. You’ve been told there is no other way.

But there is.

We utilize Fully Performing Assets (FPA). Think of an FPA as the "smartphone" of your balance sheet. Just like your phone replaced your camera, your pager, your map, and your music player, an FPA consolidates 5 to 15 "pillars" of value into one vehicle:

Guaranteed Growth (No more daily account checking)

Protection from Loss (Your floor is always zero)

Tax-Free Income (Stop sharing your wealth with the IRS)

Uncapped Gains (Participate in the upside without the downside)

This isn't a "product" you buy from a broker who’s chasing a commission. This is Engineering of Certainty. It is rooted in institutional-grade Asset Liability Management (ALM): the same principles the world’s largest banks use to ensure they never go bust.

The Margin Audit™: Finding the Leaks

Wall Street wins because of "micro-margins." A 1% fee here, a 15% "routine" loss there, a 25% tax hit later. On their own, they seem manageable. Combined, they are the reason that 25-year-old ends up with $80k instead of $2.7M.

Our job is to perform a Margin Audit™. We look at your current plan and find the "leaks."

Where is your money at risk?

How much of your "gain" is actually just inflation?

What happens to your lifestyle if the market drops 20% the year you retire?

If you can’t answer these questions with mathematical precision, you don't have a plan: you have a hope. And hope is not a strategy for retirement.

Peace is the Path, Wisdom is the Way

You don't need more "research." You don't need another daily market update. You need a design.

A true Architect doesn't just hope the building stays up; they engineer the foundation to withstand the specific stresses it will face. Your retirement should be no different.

The overriding worry you feel is your gut telling you that your current foundation is built on sand. It’s time to move your money off of "Wall Street" and onto "Your Street."

It’s time to stop being a participant in someone else’s profit machine and start being the architect of your own certainty.

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now

Check out the Retirement Blueprint

The Orange Zone (Ages 45–65): — The "Great Unknown" where market retracements keep you in the dark.