Beyond Wall St: Using the Margin Audit for Retirement Planning

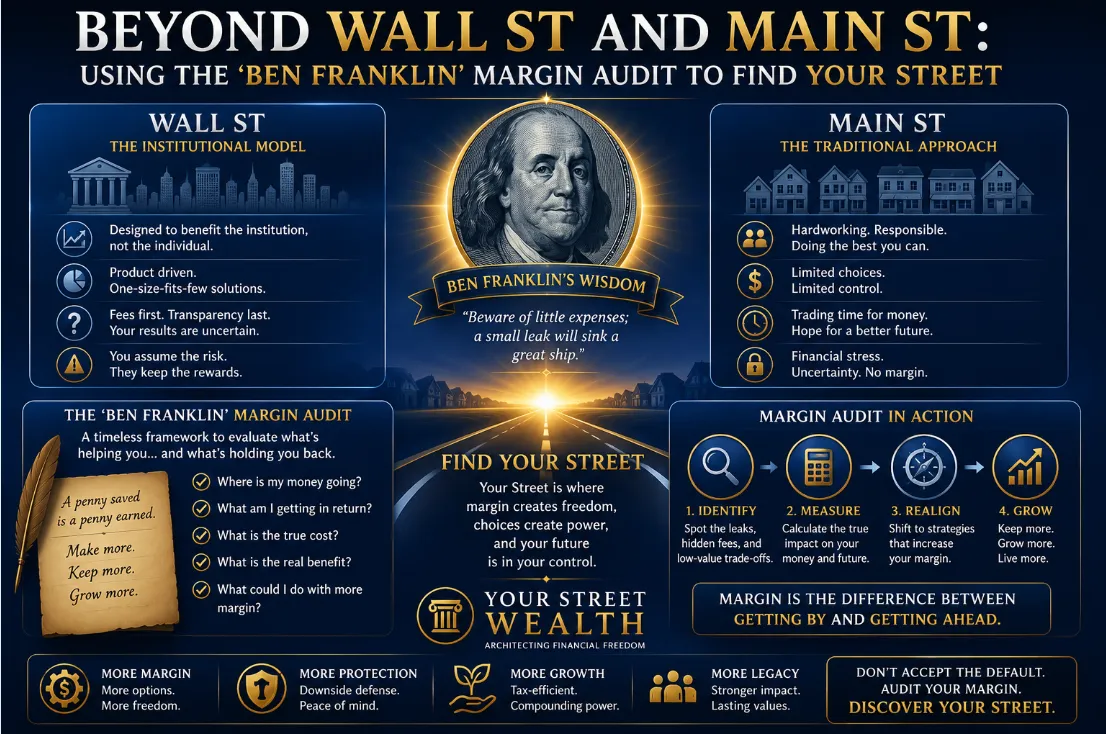

Beyond Wall St and Main St: Using the 'Ben Franklin' Margin Audit to Find Your Street

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

![[HERO] Beyond Wall St and Main St: Using the 'Ben Franklin' Margin Audit to Find Your Street](https://cdn.marblism.com/xo7lfa9FcOT.webp "[HERO] Beyond Wall St and Main St: Using the 'Ben Franklin' Margin Audit to Find Your Street")

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The Retirement Ping-Pong Trap: Why You’re Losing on Both Wall St and Main St

If you’ve spent any time looking at your 401(k) statement lately, you’ve likely felt like a spectator at a high-stakes ping-pong match.

On one side of the table is Wall Street. It’s loud, it’s fast, and it’s volatile. One year you’re up 20%, and the next, a "market correction" wipes out three years of progress. When you get tired of the bruising losses and the "hope and pray" model of traditional investing, you do what most people do: you retreat.

You head over to Main Street. You look for safety in big-box banks, CDs, or basic savings accounts. But once the dust settles, you realize you’ve traded one problem for another. On Main Street, your money isn’t shrinking, but it isn’t breathing, either. It’s stagnant. Inflation is eating your lunch, and the "safety" you bought feels a lot like a slow-motion leak in your retirement boat.

Eventually, you get bored or frustrated with zero growth, and: like a predictable reflex: you jump back onto the Wall Street table.

This is the Fake Binary. It’s the false choice that keeps most "Quiet Builders" trapped in a cycle of frustration. Wall Street titans want you to believe that if you want growth, you must accept soul-crushing risk. Main Street tycoons want you to believe that if you want safety, you must accept zero performance.

There is a third option. It’s called Your Street.

The Plus Delta: The Math Wall Street Hides

In engineering, "Delta" refers to change. In your retirement, every single financial move has a Plus Delta (+) and a Minus Delta (-). Everything has an impact, and most of those impacts are hidden in the fine print.

Understanding the timing and impact of these elements is the difference between an engine that hums and one that smokes.

When you "participate" in the market, you see the Plus (+). That’s the shiny green number on your statement. But you rarely calculate the Delta (Δ): the actual change in your purchasing power after you account for the "Wealth Killers."

The Minus Delta of Taxes: Are you building a pile of money that you only own 70% of?

The Minus Delta of Fees: Are you paying for "active management" that fails to beat a simple index?

The Minus Delta of Volatility: This is the big one. It’s the Math of Recovery.

If your portfolio takes a 30% hit: which history shows happens about every five years: you don’t need a 30% gain to get back to even. You need a 42% gain just to see the surface of the water again. While you’re busy "recovering," your most precious asset: Time: is being set on fire. Money can recover. Time never does.

The Math of Reality vs. The Math of Hope

Wall Street runs on "Average Returns." Your life runs on "Actual Returns."

Imagine a pilot telling you that, on average, the plane stays in the air 95% of the time. You wouldn’t get on that plane. Yet, we accept "probabilities" in our retirement planning every day. We use retirement plan reviews that are built on projections, not guarantees.

")

As this chart shows, bear markets aren't "black swan" events; they are a regular feature of the Wall Street landscape. If you are 5 to 10 years away from retirement, or already in it, you cannot afford to "participate" in these cycles. You need engineered performance.

The Benjamin Franklin Side-by-Side Chart

Old Ben Franklin was known for his "Prudential Algebra." When faced with a tough decision, he’d divide a sheet of paper into two columns: Pro and Con. He’d weigh the factors, cross out the ones that canceled each other out, and find the truth.

At Your Street Wealth, we use a modern, institutional-grade version of this called the Margin Audit™.

We take your current "Wall Street" or "Main Street" plan and put it side-by-side with a "Your Street" design. We don’t look at "maybe" or "if." We look at the margins. We look at the Compounding Efficiency and the Sequence of Return Margin.

On one side, you see the Assets at Risk (AAR): the single-pillar assets like stocks or real estate that are subject to the whims of the market and the "sharp knives" of interest rate ripples.

On the other side, we look at Fully Performing Assets (FPA).

The difference isn't just a few percentage points. The difference is a complete shift in architecture.

From "Rolodex" to "Smartphone": The FPA Advantage

Traditional retirement strategies are like a Rolodex in a SpaceX world. They were durable in the 1980s, but they are inadequate for today’s speed and risk.

Think about your phone. It used to be just a phone. If you wanted to take a picture, you needed a camera. If you wanted to find your way, you needed a map. If you wanted to listen to music, you needed a Walkman.

Single-pillar assets (the Wall Street/Main Street model) are like that old gear. Your bank account does one thing. Your stock portfolio does another. Your real estate does a third. They don't talk to each other, and they certainly don't protect each other.

Fully Performing Assets (FPA) are the "smartphone" of finance. They consolidate 5 to 15 pillars of value into one vehicle:

Uncapped Gains (UCG): The ability to grow when the market grows.

Expanded Market Participation (EMP): Using multipliers (110%–200%) to capture more of the upside.

Guaranteed Retirement Income: Contractual certainty that you won't outlive your money.

Protection from Market Crashes: A contractual floor of 0%. If the market drops 30%, your "Delta" is zero. You stay level while everyone else falls behind.

The 7-Vector Navigation: Finding Your Street

When we conduct a Margin Audit™, we aren't just looking for a better "product." We are looking at your entire financial ecosystem through the lens of our 7-Vector Wealth Navigation System™.

Most advisors focus solely on "Growth." They ignore the other six vectors: Protection, Time, Income, Legacy, Liquidity, and Reality.

Risk is for business, not retirement. When you were 30, you had the time to gamble. Now, you need best retirement income strategies that are based on engineering, not luck. You need a plan that understands that a dollar protected is worth more than a dollar "maybe" gained.

Stop the Ping-Pong Match

The "Titans of Wall Street" don't want you to know about Your Street because they can't charge you fees when your money is protected and performing with precision. The "Main Street" institutions don't want you to know because they rely on your stagnant cash to fund their own growth.

It’s time to stop accepting the Fake Binary. You don’t have to choose between losing your shirt and losing your mind to boredom.

You can have guaranteed retirement income and protect retirement savings from market crash scenarios without giving up the growth you need to outpace inflation. It’s about moving your money from the "Teens" (Assets at Risk) to the "Foundation" (Fully Performing Assets).

Is Your Retirement Engine Smoking?

Most people don't realize their plan is failing until the market crashes and they see the "Minus Delta" in real-time. By then, the damage is done.

The first step to finding "Your Street" is getting a clear, unvarnished look at your current trajectory. You need to know if your retirement engine is actually performing or if it’s just blowing smoke.

Audit the margin. Protect your time. Engineer certainty.

Take the Seven Question Retirement Stress Test. It takes less than three minutes, but it will reveal the truth that Wall Street and Main Street have been hiding from you.

👉 Take the 7-Question Stress Test Here

Peace is the path, wisdom is the way. It’s time to put your money on Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been. Guaranteed to show you how to Increase your account value by $20,000 - $100,000 immediately.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now

Check out the Retirement Blueprint