How to Protect Retirement Savings From a Market Crash

7 Mistakes You’re Making With Your Nest Egg (and How to Protect Retirement Savings From a Market Crash)

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

showing a calm, green-lit path to retirement through a stormy digital landscape representing market volatility. The interface is clean, professional, and reflects \"Quiet Builder\" engineering.")

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

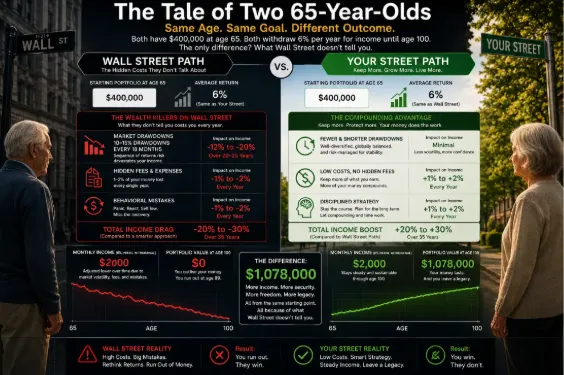

Can You Protect Your Retirement From a Market Crash?

If you are a "Quiet Builder": someone who spent decades building a career, a business, or a corporate legacy: you probably feel a nagging sense of unease. You’ve done the work. You’ve filled the nest egg. But as you look at the horizon, the traditional "Wall Street" path feels less like a strategy and more like a game of high-stakes musical chairs.

The problem isn't your work ethic; it’s the architecture. Most retirement plans are built on "Participation": the hope that if you just stay in the market long enough, the averages will work out. But hope is not an engineering strategy.

In a "SpaceX world," most people are still using a financial "Rolodex." They are relying on single-pillar assets (like just stocks or just real estate) that were durable in the 1980s but are inadequate for the speed and risk of modern retirement.

To protect your time and wealth, you must move from Participation to Engineered Performance. Here are the 7 critical mistakes currently draining the certainty from your retirement: and how to fix them.

1. Chasing "Average Returns" (The Sequence of Returns Trap)

Wall Street loves to talk about "Average Annual Returns." It sounds safe. It sounds predictable. But in retirement, averages are a lie.

When you are in the "Accumulation Phase" (saving money), the order of your returns doesn't matter much. But the moment you enter the "Distribution Phase" (spending money), the Sequence of Returns is everything. If the market crashes in the first five years of your retirement while you are taking withdrawals, your portfolio can be permanently "broken," even if the market eventually recovers.

The Fix: Stop managing for averages and start managing for Sequence of Return Margin. You need a plan that ensures your lifestyle is funded by assets that don't care what the S&P 500 did this morning.

2. Staying in "Assets at Risk" (AAR) Too Close to the Finish Line

Most investors carry "Assets at Risk" (AAR) deep into their 60s and 70s. This is like sprinting toward a cliff and hoping your brakes work at the very last second. Traditional models suggest a "glide path," but often that path is still 60% exposed to the "sharp knives" of interest-rate ripples and market volatility.

The deeper problem is allocation. Many advisors keep Quiet Builders parked in high-risk mixes like 80/20 or even 60/40 far too close to retirement because that model keeps assets in motion, keeps participation alive, and keeps Wall Street paid. In plain English, it is often an allocation that serves the house, not the builder.

Call it what it is: Wall Street's one-size-fits-all plan. It may look diversified on paper, but it still leaves 100% of your money exposed to the system. Stocks can fall. Bonds can get hit by rates. Correlation can show up right when you need protection most. Meanwhile, the advisor still collects the fee for keeping you in the game. Those are participation credits for the house, not engineered performance for your retirement.

That matters because a 60/40 portfolio is not a protection strategy. It is still a participation strategy with a smaller helmet. When stocks fall and bonds wobble under rate pressure, the so-called "balanced" portfolio can still lose meaningful ground right when income planning matters most. That is not certainty. That is dependence.

Your Street Wealth recommends a different rule set: the Rule of 100 or 75. In simple terms, reduce risk each year as you age by increasing the percentage of Fixed Pension Accounts (FPA) in your plan. Move gradually out of Assets at Risk and into assets engineered for protection, compounding efficiency, and income clarity. That is how you shift from Participation vs. Engineered Performance. That is how you protect time, not just statements.

Instead of asking, "How much market exposure can I tolerate?" ask, "How much uncertainty should I carry this close to retirement?" For Quiet Builders, the answer is usually less every year. More FPA. Less noise. More peace of mind. More architecture. Less hope.

The Fix: Audit your Asset Pyramid. Run The Margin Audit™. Apply the Rule of 100 or 75. Reduce risk annually by increasing your allocation to Fully Performing Assets (FPA) as you age. Ask whether your allocation protects your future income or simply keeps you participating in the Wall Street machine. Your foundation should be built on engineered performance designed for the client's peace of mind, not on participation risk designed to secure advisor fees.

3. Ignoring the "Math of Recovery"

If your $1,000,000 nest egg drops by 30%, you have $700,000 left. To get back to $1,000,000, you don't need a 30% gain. You need a 42.8% gain.

If you lose 50%, you need a 100% gain just to break even. This is the "Volatility Recovery Analysis" that most brokers ignore. While you are waiting years (or decades) for that recovery, you are losing the one thing you can never replace: Time.

The Fix: Use a Volatility Recovery Analysis to see exactly how many years of your life are currently at risk. Remember: Money can recover. Time never does.

4. Relying on "Single-Pillar" Assets

Traditional financial products are "single-pillar."

Banks: Provide liquidity, but zero growth and high "leakage" to taxes.

Stocks: Provide growth, but zero protection.

Real Estate: Provides income, but low liquidity and high "friction."

In the modern era, relying on these is like carrying a pager, a map, and a camera. It’s clunky and inefficient.

The Fix: Shift to "Smartphone Finance": Fully Performing Assets (FPA). Just as a smartphone consolidated ten devices into one, an FPA consolidates 5–15 "pillars" of value (growth, LTC protection, tax-free income, and A+ guarantees) into a single, engineered vehicle.

5. Keeping the "Greed Meter" Pinned

Wall Street operates on a "False Model" driven by fear and greed. When the market is up, the "Greed Meter" hits red, and investors stay in far too long, trying to squeeze out the last 2%. When it crashes, fear takes over, and they sell at the bottom.

The Fix: Practice Engineered Certainty. Use a "Margin Audit" to identify when it’s time to take gains off the table and move them into the "Your Street" side of the ledger. Growth without loss is the only way to maintain forward momentum.

6. Paying "Participation Credits" (Hidden Fees)

Many Wall Street products are designed with hidden complexity to drive daily research and "addictive" buying and selling. Between management fees, transaction costs, and "participation credits" taken by the house, your Compounding Efficiency is being bled dry.

The Fix: Look for vehicles with Uncapped Gains (UCG) and Expanded Market Participation (EMP). We often see EMP multipliers of 110%–200%, meaning if the market gains 10%, your engineered asset could gain 11%–20%: all while maintaining a 0% floor against market losses.

7. Lacking a "Heads-Up Display" (HUD)

Most retirees are flying blind. They have a "statement" that tells them where they were last month, but they don’t have a Forecast that tells them where they are going. They are making guesses based on "probabilistic" software that uses a 4% rule from the 1990s.

The Fix: You need a Million Dollar Hour™ Forecast. This isn't a "sales pitch"; it’s an institutional-grade engineering session. It functions as your wealth's "Heads-Up Display," providing a clear, actionable path that eliminates uncertainty.

Moving From Participation to Architecture

Peace is the path, and wisdom is the way. You don't have to stay on "Wall Street," spinning sharp knives and hoping the wind doesn't blow. You can move to "Your Street," where the rules are yours and the math is guaranteed.

Stop "participating" in the gamble. Start "engineering" your certainty.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now