Retirement Income Planning: The 5 D’s of Wealth Deficiency

The Next 5 D's of Wealth Deficiency: Debt, Dependency, Deceit, Distraction & Delay

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

If you’ve been following our work at Your Street Wealth, you’ve likely seen The 5 D's of Wealth Destruction. Those are the catastrophic events: Denial, Decisions, Downturns, Divorce, and Death: that can level a financial house overnight.

But wealth isn't always lost in a landslide. Often, it’s siphoned away by a slow, persistent leak.

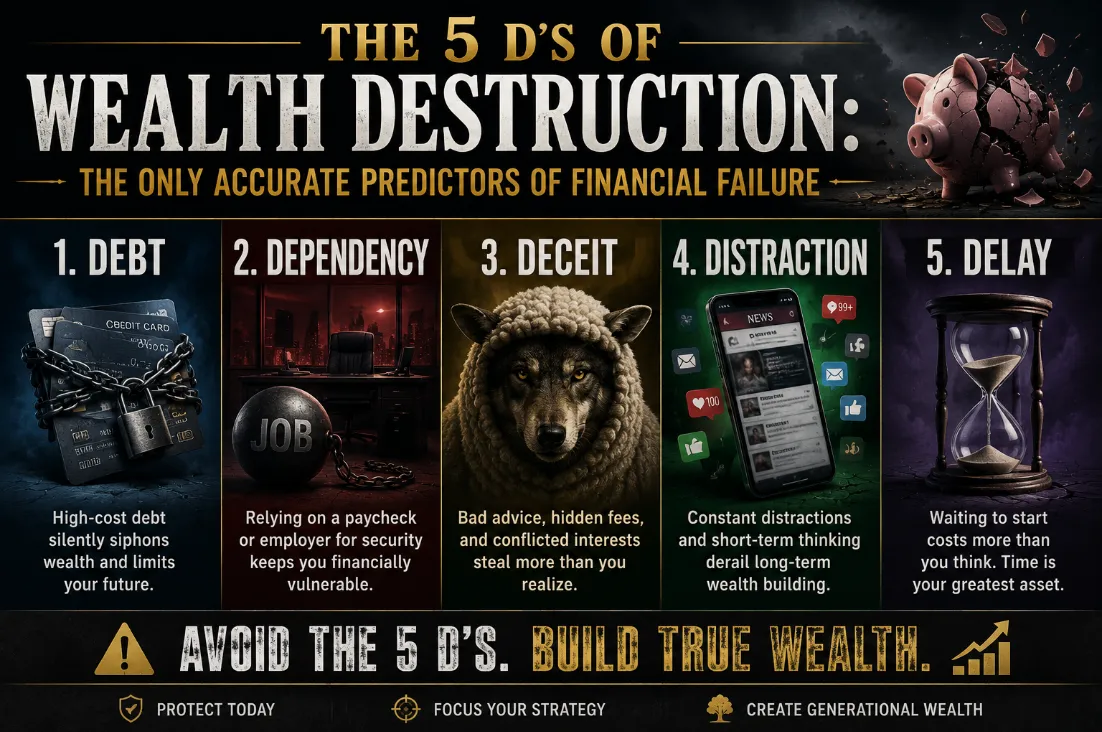

We call these the Next 5 D’s of Wealth Deficiency. These aren't the storms; they are the termites. They are the structural flaws in your financial architecture that prevent you from ever reaching your full potential. While the first 5 D's focus on protecting retirement savings from a market crash, these next 5 focus on Compounding Efficiency and the engineering required to stop the "slow bleed."

For the Quiet Builder, the goal isn't just to survive a downturn; it's to engineer a life where wealth grows with certainty. To do that, we must audit the margin and eliminate the siphons.

1. Debt: The Reverse Compounder

Wall Street loves to talk about the power of compounding. What they rarely mention is that debt is compounding working against you. It is the "Reverse Compounder."

High-cost debt: whether it’s a lingering mortgage, high-interest business loans, or consumer credit: silently siphons wealth and limits your future. Every dollar you pay in interest is a dollar that isn't working for you in a Fully Performing Asset (FPA).

In our world, we perform a Margin Audit™. We look at the delta between what your money could be doing and what it is doing. If you are paying 7% on a loan while your "Assets at Risk" (AAR) are fluctuating in the market, you aren't just losing the 7%; you are losing the Compounding Efficiency of those dollars over the next 20 years.

Debt is a single-pillar liability. It has one job: to extract value from your balance sheet. Contrast this with strategic engineering, where we use the Math of Recovery to ensure every dollar is optimized. If you want to know how much you need to retire, you first have to know how much of your future is already "owned" by someone else.

2. Dependency: The Illusion of the Single Pillar

Many successful people: former corporate executives, business owners, and engineers: suffer from the "Dependency Trap." They rely on a single paycheck or a single employer for their security. This keeps you financially vulnerable, regardless of how high your salary is.

Relying on one source of income is what we call a "Single Pillar" model. It’s like using a Rolodex in a SpaceX world. It worked in the 1980s, but it’s inadequate for the speed and risk of modern planning.

In a retirement income planning context, dependency is the enemy of peace. If your retirement is dependent on the "hope" that a CEO doesn't make a bad call or that the market stays bullish for the next 30 years, you aren't an architect; you are a participant in someone else’s gamble.

We advocate for moving from dependency to Performance. This means shifting your foundation into Fully Performing Assets (FPA). Think of an FPA as the "smartphone" of finance. Just as your phone consolidated your camera, pager, and TV into one device, an FPA consolidates 5–15 pillars of value: like growth, protection, and tax-free income: into one vehicle. Control over your income stream matters far more than the size of it.

3. Deceit: The Hidden Complexity of Wall Street

Wall Street operates on a "False Model" driven by greed and fear. They use hidden complexity to drive daily research and addictive buying and selling. This is the third D: Deceit.

This isn't always a "suit-and-tie" scam. Often, it’s the deceit of hidden fees, commission-based advisors, and the "free" lunch that costs you decades of growth. They promise "market participation" but hide the fact that a 30% loss requires a 42% gain just to get back to zero. This is the Math of Recovery that they hope you never calculate.

When you undergo a retirement plan review, ask yourself: Am I being told about probabilities or guarantees? Wall Street deals in projections; Your Street deals in contractual certainty. We contrast their "spinning sharp knives" approach with institutional-grade banking architecture.

Peace is the path, wisdom is the way. To find the path, you must first unlearn the myths sold by the "Participation" crowd.

4. Distraction: The Noise vs. The Engineering

We live in an age of constant distraction. Daily market headlines, social media "experts," and shiny object syndrome derail long-term wealth building.

Distraction is a wealth-killer because it shifts your focus from micro margins to macro headlines. Real wealth isn't built on what the Fed said this morning; it’s built on Compounding Efficiency and Sequence of Return Margin.

The "Quiet Builder" knows that wealth is an engineered outcome, not a reaction to the news. When you are distracted by the "Greed/Fear meter," you make emotional decisions that reset the clock on your compounding.

Audit the margin. Ignore the noise. Focus on the architecture. Our Million Dollar Hour™ Forecast is designed to cut through this distraction in exactly 60 minutes, providing a clear, actionable path that eliminates uncertainty.

5. Delay: The Cost of Lost Time

The final D is the most expensive: Delay.

Waiting to start: or waiting to fix a broken plan: costs more than you realize. Money can recover; time never does.

Let’s look at the math. A five-year delay in moving from an "Asset at Risk" (AAR) to a "Fully Performing Asset" (FPA) doesn't just cost you five years of growth. It costs you the Volatility Recovery Analysis: the years you spend just trying to get back to even after a market dip.

If you are 55 and you wait until 60 to implement the best retirement income strategies, you aren't just losing five years; you are potentially losing six or seven figures in compounded value. In financial architecture, time is the structural steel. The longer you wait to pour the foundation, the more the elements erode your potential.

"Your Money, Your Rules, In Your Time, On Your Street." That mantra only works if you take control of the time component.

The Path Forward: From Deficiency to Certainty

These 5 D’s: Debt, Dependency, Deceit, Distraction, and Delay: are the reasons why "hoping" for a good retirement is a failing strategy. You cannot predict future portfolio value when losses and leaks are uncontrollable.

You can, however, engineer a path where you know exactly where you stand.

Are you ready for clarity instead of confusion? The first step for any Quiet Builder is to stop the leaks and start the engineering. We recommend two specific tools to begin:

The 7 Question Retirement Stress Test: A quick audit to see if your current plan is built on sand or stone.

The Million Dollar Hour™ Forecast: This is our premium, $995 engineering session where we do the heavy lifting for you. We calculate your actual compounded growth, identify your lost years, and present a personalized, guaranteed path to wealth.

Stop participating in a system designed to extract value from you. Start engineering a system designed to perform for you.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now