The $1.3 Million Retirement Trap: Why 55 is the Critical Turning Point

The $1.3 Million Retirement Trap: Why 55 is the Critical Turning Point

How Much Do I Need to Retire at 55?

WOYS - Guarantees | Time Matters

June 25, 2026 • 12 min read

The $1.3M Gap: Why Two 55-Year-Olds Don’t Get the Same Retirement

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Why Do Two 55-Year-Olds Not Get the Same Retirement on Wall St?

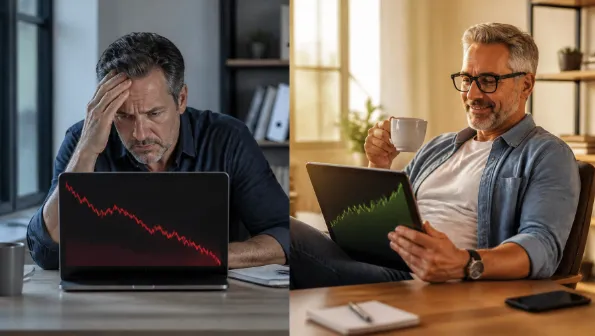

Math should be objective. If two people start at the same age, with the same money, contribute the same amount every month, and both receive a 5% average annual gain, they should land in the same place.

That is the Shiny Object story.

Now audit the margin.

Here is the actual setup for our 55-year-old "Quiet Builders." Two investors both start with $75,000. Both contribute $600 per month. Both are shown 5% average annual gains. Both begin taking 4% income after age 65.

Same Money. Same Time. Different Rules. Different Outcomes. Your Choice.

That is where the Dark Object shows up.

On the Wall Street side, the investor lives inside the routine but rarely forecasted retraction cycle: 10% retractions every 18 months. That schedule is accepted by industry titans. It is widely normalized. It is almost never built honestly into the "average return" projections your broker shows you. That is the trap. And remember, it could be much worse.

On the Your Street side, the investor uses engineered growth with no losses, $0 accumulated losses, and 0 years lost. The average growth is not limited. No Risk, No Limits. This is why you prioritize your Retirement buckets for Reliability.

The result is not a small gap. It is a structural failure on one side and engineered performance on the other.

Wall Street score: 40.5%

Your Street score: 495%

Wall Street accumulated losses: $447,000

Wall Street years lost: 32.4

Wall Street CAGR: 2.11%

Your Street CAGR: 7.31%

That $1.3 million gap is not just about money. It is deflated future wealth. It is deflated future income. It is over 32 years of time destroyed by routine retractions that no broker can forecast and no "average-return" illustration can fix.

Would you rather have a trajectory opportunity of $1.9M on Your Street, with No Risk and No Limits, or on Wall Street toward $606k?

You need evidence now!

At Your Street Wealth, we do not grade retirement by participation. We grade it by architecture. Use the Engineered Retirement Blueprint Framework. Start with the Balance Sheet as the Source of Funds. Measure the Income Statement as the Use of Funds. Then inspect Margin, because margin is the battleground between positive and negative outcomes.

Protect your time. Audit the margin. Stop eating their cheese.

1. The Yellow Zone (Ages 55–65): Expose the Routine Retraction Trap

At 55, you are in the critical ten-year sprint to the finish line. This is the "Yellow Zone," where most Quiet Builders are told to keep their heads down and "stay the course."

They are told to focus on an average return number. They are told to ignore the path. They are told retractions are normal, temporary, and nothing to worry about.

Read that again.

The same industry that accepts routine 10% retractions every 18 months almost never forecasts them into the retirement story it sells. That is not precision. That is a false model driven by fear and greed.

Call the two investors what they are: one is participating, one is engineering.

The Wall Street investor is exposed to Assets at Risk (AAR), which means hidden liabilities are already building inside the balance sheet. Losses do not just reduce the account value in the moment; they create negative margin by destroying capital, reducing compounding efficiency, and stealing time that must be won back later.

The Your Street investor uses a rules-based structure built for Engineered Performance. No loss. No reset. No wasted recovery cycle.

The Math of Recovery

Do the math, not the marketing.

If you lose 10%, you drop to $90. You now need 11.1% just to get back to even. If you hit a major retraction (averaging 40% every 5–7 years), a 30% loss requires a 42% gain just to recover. Money can recover. Time never does.

That is why the Wall Street Cycle matters. Stack those 10% retractions over ten years, and the damage compounds. This is how the Wall Street side in our 55-year-old scenario produces $447,000 in accumulated losses and 32.4 lost years.

That $447k is not just missing money. It is future income that never arrives. It is future wealth that never compounds. It is the reason Wall Street's CAGR drops to a measly 2.11% while Your Street's engineered path hits 7.31%.

That is the difference between Participation vs. Engineered Performance.

2. The Orange Zone (Ages 65+): Income Exposes the Lie

Retirement is where the false architecture gets stress-tested. This is the "Orange Zone."

Both investors take 4% income after age 65. On paper, that sounds equal. In reality, on Wall Street, your income is constantly declining due to Sequence of Return Risk (SORR).

Why? Because equal withdrawals taken from unequal systems do not produce equal retirements.

The Wall Street side enters retirement after years of retractions and compounding drag. The source of funds is weaker. Margin is tighter. Take income from a volatile account after losses, and you are harvesting from a wounded system. That is how retirement plans fail quietly: one retraction, one withdrawal, one lost recovery window at a time.

This is where Sequence of Return Margin becomes a live wire.

The Your Street side is built on guarantees instead of probabilities, control instead of dependence, and growth without loss instead of growth with loss.

Use the Power Pairs:

Certainty vs Uncertainty : Know, don’t hope.

Guarantees vs Probabilities : Use contractual design, not projections.

Control vs Dependence : Control outcomes instead of depending on markets.

Growth Without Loss vs Growth With Loss : Stop resetting the clock.

Increasing Income vs Depleting Assets : Build rising income instead of draining principal.

Time Compounding vs Time Lost : Protect the one asset you can never replace.

Single-Pillar vs Multi-Pillar

Traditional assets like banks, stocks, and real estate are single-pillar tools. They are a "Rolodex in a SpaceX world." Durable in their era, but inadequate for the speed and risk of modern retirement planning.

We use Fully Performing Assets (FPA): the "smartphone" of finance. An FPA consolidates 5 to 15 pillars of value into one vehicle: growth, protection, tax-free income, and A+ guarantees.

When we engineer these assets, we include:

Uncapped Gains (UCG)

Expanded Market Participation (EMP), where a 10% UCG can become an 11% to 20% gain through a multiplier.

0% Floor Protection (The math of 0 is the most powerful force in finance).

Compare the design plainly:

Wall Street: -30% to +30%

Your Street / FPA: 0% to +30%

That is not hype. That is architecture.

3. Why the Gap Becomes Massive: Audit the Dark Object

Most people only see the Shiny Object: the 7-10% average annual return mirage.

They do not see the Dark Object:

Cumulative cycle losses

The "Time Tax" (years lost to recovery)

Sequence-of-returns damage

Hidden fees ("Tolls with no bridge")

This is why "average returns" are rouge numbers. They fail to account for the total of all negatives. Nobody can prove Wall Street gains will exceed losses over your specific retirement window. They can only hope.

This is where the 5x Accumulated Loss Truth reveals the hidden liability. Over a lifetime, accumulated losses can be 5x greater than your contributions. A 55-year-old putting in $75k plus $600/month can watch the system destroy nearly half a million dollars of economic value through retractions.

The Million Dollar Hour Income Analysis Comparison is the tool that lets you choose the retraction impact you design for. It shines light on both the Shiny and Dark objects simultaneously.

Why the Gap Exists: The Architecture of Your Street

The gap is not luck. The gap is rules.

Wall Street operates on a false model. They use hidden complexity to drive daily research and addictive buying/selling. They charge fees that provide zero value because they do not eliminate "wealth killers" like market losses or lost time.

At Your Street Wealth, we ground everything in institutional-grade Asset Liability Management (ALM) and modern banking architecture.

Use the Asset Pyramid to visualize your foundation:

Non-Performing Assets (NPA): Infants/Emergency liquidity.

Assets at Risk (AAR): Teens/Declining allocation as you age.

Fully Performing Assets (FPA): The Foundation.

If you are a Quiet Builder at 55, this is your cue to stop admiring "averages" and start interrogating design.

Ask the hard questions:

How many years of my life am I willing to lose to the next 10% retraction?

Am I using a single-pillar tool for a multi-pillar problem?

Am I participating in a gamble, or have I engineered a performance?

The market will retract. It’s part of the cycle. The question is: Is your plan forced to absorb the damage?

Same Money, Same Time, Different Rules, Different Outcomes, Your Choice.

Peace is the path, wisdom is the way.

The Million Dollar Hour™

Ready to stop guessing? The Million Dollar Hour™ is a paid $995 Engineering/Margin Audit designed for those who value precision over "free" advice. In one 60-minute session, we help you:

Audit the Margin

Run a Volatility Recovery Analysis

Measure Compounding Efficiency

Inspect Sequence of Return Margin

Compare Participation vs. Engineered Performance side-by-side

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

👉 Take the 60-Second Quiz

Most people are impacted by 6–9 and don’t realize it

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now