Wall Street Credibility Gap: 5 Retirement Questions

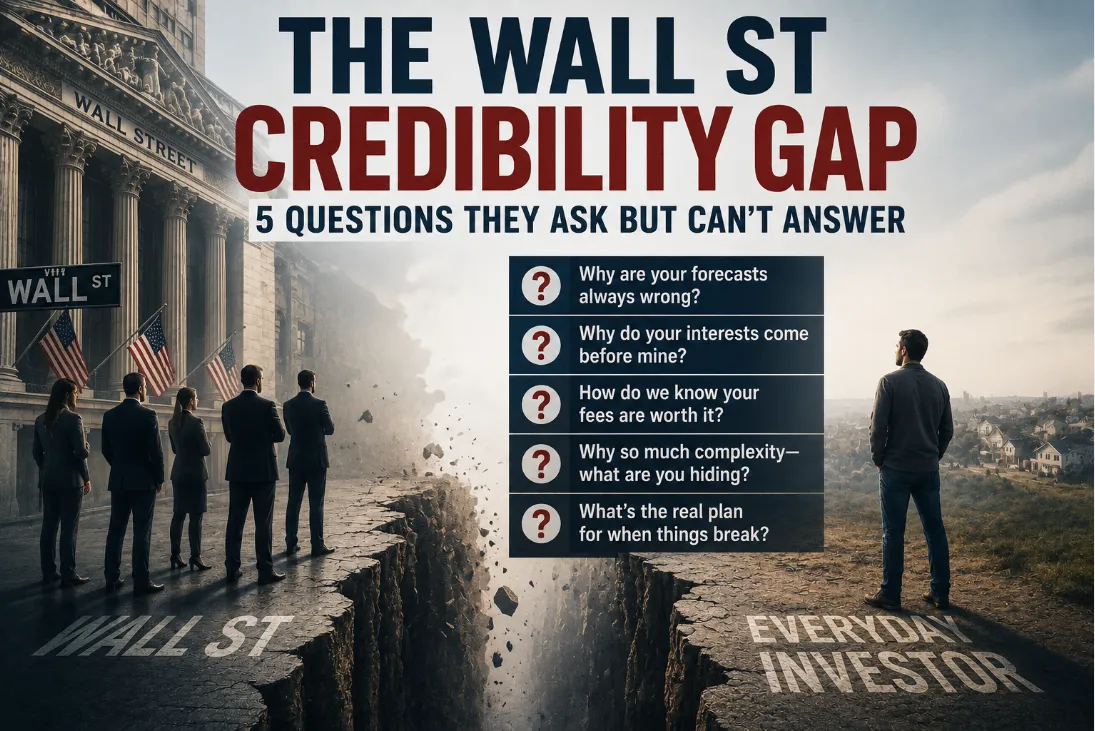

The Wall Street Credibility Gap: 5 Questions They Ask (But Can’t Answer)

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The Wall Street Credibility Gap: 5 Questions They Ask (But Can’t Answer)

Wall Street has a structural problem. It’s not just the volatility, the hidden fees, or the endless research cycles designed to keep you addicted to the "buy/sell" button.

The real problem is a Credibility Gap.

The industry asks you deep, probing questions about your future, your safety, and your family’s security: but their own system is physically incapable of delivering the answers you give. It’s like a car salesman asking how much you value safety, only to sell you a vehicle with no brakes and a "hope-based" steering system.

They ask the questions, but they cannot satisfy the answers. This creates a massive disconnect between what you actually want and what the traditional market is structurally built to provide.

At Your Street Wealth, we don't play the "Participation" game. We focus on Engineered Performance. We don't hope for outcomes; we design them.

Here are the 5 questions that expose the Wall Street gap: and why the traditional response is a violation of your preferences.

1. “How Much Principal Are You Willing to Lose?”

The Client Answer: 96% say ZERO.

Ask any "Quiet Builder": the successful, financially fatigued executive or business owner: how much of their hard-earned capital they are comfortable seeing evaporate in a market correction. The answer is almost always a resounding zero. You spent decades building this; you aren't looking to gamble it now.

The Wall Street Contradiction:

Despite your answer, Wall Street portfolios are built on "accepted loss models." Your advisor likely normalizes loss as "part of the journey." They tell you to "stay the course" while your balance sheet bleeds. Even TV analysts casually admit to 10%–20% retractions about every 18 months, and roughly double that every 6 years. In other words, the system openly expects setbacks and then asks you to call that normal.

The system begins with a known violation: You want protection; they offer exposure. In our world, we call this the Single-Pillar Trap. Traditional assets like stocks are single-purpose: they only work if the market goes up. We prefer Fully Performing Assets (FPA), the "smartphone" of finance, which consolidate protection and growth into one resilient vehicle with a 0% Floor in the FIAAR strategy.

2. “If You Were to Lose Money, How Long to Break Even?”

The Client Answer: 87% say 1 year or less.

Time is your most precious asset. In your 50s and 60s, you don't have a 10-year horizon to "wait for the market to come back." You need your money to be ready when you are.

The Math of Break Even:

Wall Street rarely explains the Volatility Recovery Analysis. If you lose 30%, you don’t need a 30% gain to get back to even. You need a 42% gain just to Break Even. That gap is lost time and lost money.

If that loss happens near retirement: what we call the "Retirement Risk Zone": you hit Sequence of Return Risk. This is where the math becomes devastating. Withdrawing income from a shrinking base permanently impairs your portfolio’s ability to recover. Money can recover; time never does.

The traditional system relies on long break-even cycles. Our architecture is designed for Compounding Efficiency, and the FIAAR strategy introduces the SUF - Stepped UP Floor to lock in progress so you do not keep sliding backward and restarting the clock.

3. “How Much of Your Principal Do You Want to Grow?”

The Client Answer: 100% say 100%.

No one walks into a financial office and says, "I’d like only 40% of my money to actually work for me, while the rest sits in defensive, low-yield positions or spends the next five years just trying to get back to where it started."

The Hidden Inefficiency:

In a traditional market-based plan, large portions of your portfolio are often:

Recovering from previous losses.

Trapped in "safe" side-pockets that barely beat inflation.

Offsetting the volatility of the "risky" side.

This creates an invisible drag on your lifetime performance. To get 100% of 100% growth, you need a declining allocation of Risk over time per the FIAAR strategy, not permanent exposure to Wall Street volatility. We use Uncapped Gains (UCG) and Expanded Market Participation (EMP). Imagine getting 110% to 200% of the market's upside with none of the downside. That’s not a "market play"; that’s financial engineering.

4. “How Much Access Do You Want to Your Principal?”

The Client Answer: 98% say 100% access.

You want control. You want the flexibility to pivot, to fund an emergency, or to seize a new opportunity on your own terms. You want Strategic Mobility.

The Dependency Model:

Traditional systems often create "liquidity traps." Whether it’s tax penalties, surrender charges, or the simple reality that you can’t sell stocks when the market is down 20% without "locking in" the loss, you are often at the mercy of the system. Wall Street access is further restricted by tax traps on gains and principal reduction on losses. Both erase wealth.

Wall Street creates dependency; Architecture creates freedom. Our goal is to ensure you have access to your capital without the "permission" of a volatile market.

5. “Should We Plan for the Good, the Bad, or Both?”

The Client Answer: 98% say BOTH.

This is the most devastating answer for the Wall Street model. Traditional marketing is built on "Optimism Language." They show you hypothetical growth curves, upward projections, and "average" returns that look great in a brochure but fail in a recession.

Optimism vs. Engineering:

You don’t want a plan that only works if the next ten years look like the 1990s. You want a plan robust enough to survive:

Recessions and market crashes.

Hyper-inflation.

Rising tax environments.

Health events and longevity risk.

And this is where the industry's psychologically dark strategy shows up. These questions are often designed to psychologically prepare clients for losses rather than engineer success. That is the real trap. The conversation sounds caring, but the system underneath still assumes setbacks, excuses delays, and trains people to tolerate damage.

Wall Street responds with optimism and a psychologically dark strategy. We respond with institutional-grade Asset Liability Management (ALM). We audit the margin and engineer certainty so that "the bad" doesn't break your life.

The Core Contradiction: Participation vs. Performance

The public is unknowingly asking for certainty, resilience, and protected growth. Wall Street frequently delivers volatility, exposure, and recovery dependency.

This is the philosophical divide. Participation is gambling on headlines. Performance is an architecture designed to heal and grow regardless of the macro noise.

Think of it like the consolidation of technology. We used to carry a pager, a camera, a map, and a phone. Now, we just have a smartphone. The old "Single Pillar" model of 1980s-style banking and stock-picking is the "Rolodex in a SpaceX world." It’s outdated. Fully Performing Assets (FPA) are the multi-pillar solution for the modern "Quiet Builder."

The Greatest Deception

The greatest deception in the financial industry is not the answers you give. It is the industry pretending that a traditional, risk-based system was ever designed to fulfill them.

If you are tired of the "Stay the Course" mantra and want to see the actual math of your current plan, it’s time for a Margin Audit™.

Our Million Dollar Hour™ Forecast is a $995 professional engineering session designed for those who value precision over probability. In 60 minutes, we don’t just "review your stocks"; we scrutinize your architecture. We calculate your years lost to market volatility and present a guaranteed path to safer wealth. Guaranteed to show you how to Increase your account value by $20,000 - $100,000 immediately.

Stop spinning sharp knives with your retirement. It’s time to move from Your Street to Your Rules.

Peace is the path, wisdom is the way.

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now

Check out the Retirement Blueprint

The Orange Zone (Ages 45–65): — The "Great Unknown" where market retracements keep you in the dark.

Wealth Killer #2: The 4% Rule Myth : Why 'Safe' Withdrawal Rates Are Dangerous

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →