Why a 10% Market Drop Destroys Retirement Savings Faster

Part 2: The Math of the Peak – Why a 10% Drop Today Costs More Than a 30% Drop Ten Years Ago

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The Math of the Peak: Why Your Biggest Win is Your Biggest Risk

In the world of the "Quiet Builder," silence is usually a sign of progress. You’ve spent decades accumulating, managing your business, and ignoring the daily noise of Wall Street. But as the market hits new all-time highs, that silence can become dangerous.

When you are at the "Peak," the rules of the game change. The math you used to build your wealth is no longer the math you can use to protect it. Most people think a 10% market correction is just a "hiccup." If you’re 35, it is. If you’re 60, it’s a structural failure.

At Your Street Wealth, we don’t look at percentages; we look at the Margin Audit™. We look at the dollars. And the dollars are telling a story that Wall Street won't share.

The Dollar-for-Dollar Reality: Percentages Lie, Dollars Tell the Truth

Wall Street loves percentages because they mask the magnitude of the risk. They tell you, "The market is only down 10%," as if that’s a universal constant. It isn’t.

Let’s look at the math of two different people:

The Young Builder: You have $100,000. The market drops 30%. You lose $30,000. It stings, but you have 25 years of "Employment Window" left to make it up.

The Quiet Builder (You): You have $1,000,000. The market drops a mere 10%. You lose $100,000.

Do you see the disconnect? A "minor" 10% retraction on your current portfolio is three times more devastating than a "major" 30% crash was earlier in your career. This is what we call sequence of returns risk. When you have the most to lose, the market is at its most volatile.

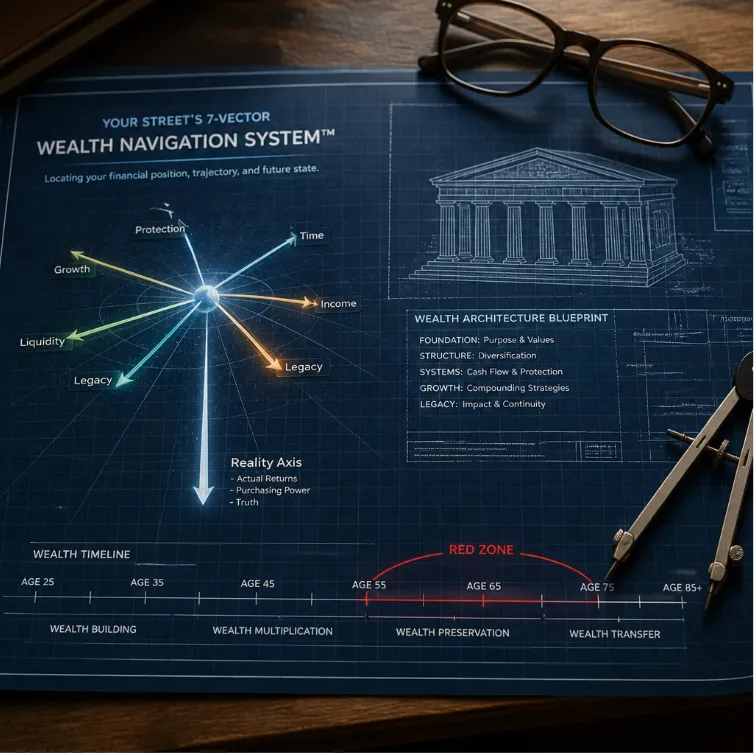

Using our 7-Vector Wealth Navigation System™, we map your actual position on the Reality Axis. We don't care about "projected returns" or Wall Street "hopes." We care about the actual purchasing power of your dollars and the truth of your current trajectory.

The Math of Recovery: The Asymmetric Climb

One of the most dangerous myths in finance is that "if it goes down 50%, I just need 50% to get back to even."

That is mathematically false.

If your $1,000,000 portfolio drops to $500,000 (a 50% loss), and then gains 50% back, you only have $750,000. You are still $250,000 short. To get back to even, you need a 100% gain.

Ask yourself: How long did it take you to earn that first $1,000,000? How many years of work, stress, and missed family time went into that number? Now, imagine needing a 100% gain just to get back to where you were yesterday: all while your Employment Window is closing. That’s exactly why people searching how to protect retirement savings from market crash need to understand the real math before the next drop does the teaching.

Money can recover. Time never does.

The Closing Employment Window

When you are 45 or 55, time is a tool. When you are 65 or 75, time is a limit. This is why "Participation" in the market is a false architecture for someone nearing retirement.

Traditional Wall Street methods are like a "Rolodex in a SpaceX world." They were durable in the 1980s when interest rates were high and volatility was lower, but they are inadequate for the speed and risk of today’s engineered retractions.

Audit the margin. If you are sitting in Assets at Risk (AAR): meaning stocks, mutual funds, or variable annuities: you are essentially spinning sharp knives. One slip in the market cycle, and the math of recovery becomes an impossible mountain to climb.

From Single-Pillar Risks to Multi-Pillar Certainty

Most traditional assets are "single-pillar."

Banks: Give you safety but steal your growth through low interest and inflation.

Stocks: Give you growth but steal your sleep through 100% risk of loss.

Real Estate: Gives you equity but steals your liquidity and time through management and taxes.

We advocate for Fully Performing Assets (FPA). Think of FPA as the "smartphone" of finance. Just as your phone consolidated your camera, pager, map, and phone into one device, an FPA consolidates 5–15 "pillars" of value: Growth, Protection, Tax-Free Income, and Long-Term Care: into one engineered vehicle.

With an FPA, you move from the "Gambling" of Wall Street to the "Architecture" of Your Street. You move from the -30% to +30% roller coaster to a 0% to +30% engineered path.

Uncapped Gains (UCG): You capture the upside of the market.

Expanded Market Participation (EMP): Using multipliers (110%–200%) to turn a 10% market gain into an 11% or even 20% gain.

0% Floor: When the market retractions happen (and they will), your balance stays exactly where it is. No resetting the clock. No "Math of Recovery" required.

Your Margin Audit™: The Million Dollar Hour™ Forecast

You can estimate your income needs, but you cannot predict your future portfolio value when market losses and tax leaks are uncontrollable. This is why "hoping" is not a strategy.

The Million Dollar Hour™ Forecast is a $995 professional engineering audit designed for Quiet Builders who are ready for clarity. This isn't a "free consultation" designed to sell you a product; it is a high-friction, high-clarity scrutiny of your current plan. If you’ve been putting off a serious retirement plan review, this is where noise stops and precision starts.

In 60 minutes, we will:

Calculate your Volatility Recovery Analysis: See exactly how many years you'll lose if the market drops tomorrow.

Audit your Compounding Efficiency: Identify the "leaks" (fees and taxes) that are stealing your wealth.

Establish your Sequence of Return Margin: Ensure your income rises even if the market falls.

Peace is the Path, Wisdom is the Way

Don't let the peak of the market blind you to the math of the valley. Engineer certainty. Protect your time. Protect your wealth.

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads — not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now

Check out the Retirement Blueprint