Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

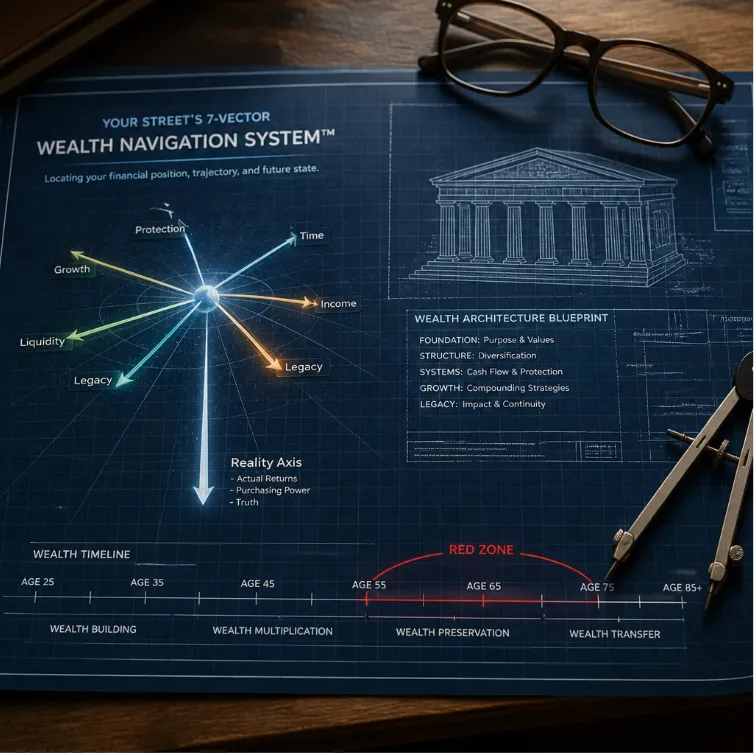

Controlling Retirement Variables: 7-Vector Wealth System

The Illusion of Choice: Why Wall Street Controls Your Retirement Variables (And How to Take Them Back)

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The "Choose 2 Out of 3" Retirement Trap: Why Wall Street Always Wins (Unless You Change the Game)

Have you ever walked into a high-end restaurant where there are no prices on the menu? Or perhaps you’ve dealt with a contractor who told you, “You can have it fast, you can have it cheap, or you can have it high-quality: pick two.”

In the world of project management, this is known as the "Triple Constraint." It’s a standard trade-off. But when this logic is applied to your life savings, it isn’t just a trade-off; it’s a trap designed to keep you in a state of perpetual "Participation" while Wall Street extracts the "Performance."

Most people nearing retirement are being forced to play a game where they think they are making choices. In reality, they are just picking which two variables they get to see while Wall Street controls the rest from behind the curtain.

The "Choose 2 of 3" Trap

In a traditional retirement plan review, a broker will often present you with three primary variables:

Cost (Fees and expenses)

Time (When you can retire)

Deliverables (How much income you’ll have)

They’ll ask which one you prefer to prioritize. If you want lower costs, you might have to work longer (Time). If you want more income (Deliverables), you might have to pay higher fees for "active management" (Cost).

When someone asks me which of these I prefer, my answer is always the same: "I don't have enough information yet to make a good choice for me."

Why? Because if you only choose two, you are implicitly handing control of every other variable over to the house. If you choose Cost and Time, Wall Street controls the Deliverables: meaning your income is at the mercy of the market. If you choose Time and Deliverables, they control the Cost through hidden fees and the "volatility tax" of market losses.

This is the "Single Pillar" model of finance. It’s like trying to build a skyscraper on a single concrete post. It might hold for a while, but it lacks the structural integrity to withstand a storm.

The 7-Vector Wealth Navigation System™

To escape this trap, you have to move beyond 2D math. Wall Street wants you to focus on "Average Returns," but as we’ve discussed before, average returns are a myth that doesn't equal retirement success.

True financial architecture requires a multi-dimensional approach. This is where the 7-Vector Wealth Navigation System™ comes in. Instead of picking two out of three variables, we look at all seven vectors that determine your actual retirement outcome.

If you only account for three variables, they control the other four. Those four hidden variables: like Sequence of Return Margin, tax efficiency, and market protection: are where your wealth goes to die.

The Seven Vectors:

Protection: Is your principal contractually guaranteed?

Time: Are you recovering lost time or just "staying the course"?

Performance: Is it engineered or are you just "participating" in the noise?

Tax Efficiency: Are you building a tax-free legacy or a tax-deferred time bomb?

Truth (Reality Axis): What is your actual compounded growth after fees and inflation?

Strategy: Is it a designed process or a collection of products?

Legacy: Does the plan end with you, or does it heal your balance sheet for the next generation?

When you ignore these vectors, you are stuck with "Free Cheese." And as any "Quiet Builder" knows, Free Cheese keeps you stuck in a trap while the cheese slowly runs out.

Single Pillar vs. Multi-Pillar Architecture

Traditional assets like stocks, bonds, and real estate are "single-pillar" assets. They do one thing reasonably well but fail when you need them to multitask. For example, a stock portfolio might provide growth, but it provides zero protection against sequence of returns risk.

Think of it like the transition from a Rolodex to a smartphone. A Rolodex was great for holding contacts in a 1980s world. But today, your smartphone is your contact list, your camera, your GPS, and your bank. It’s a "multi-pillar" device.

Fully Performing Assets (FPA) are the smartphones of the financial world. They consolidate 5–15 "pillars" of value into a single vehicle:

Uncapped Gains (UCG): Capturing market upside.

0% Floor: Eliminating the math of recovery.

Tax-Free Income: Maximizing what you keep.

Long-Term Care (LTC) Protection: Guarding against health crises.

Contrast this with the best retirement income strategies offered by big-box firms. They usually involve "drawing down" your assets: essentially betting that you’ll die before your money does. That’s not a strategy; it’s a countdown.

The Math of Recovery: Why 0% is Your Best Friend

Wall Street loves to talk about "opportunity." I prefer to talk about "Engineering."

If your portfolio takes a 30% hit: something we see routinely in the market: you don't need a 30% gain to get back to even. You need a 42.8% gain just to get back to the starting line. That is The Math of Recovery.

While you are waiting for that 42.8% gain, you are losing the most precious asset you have: Time.

In an engineered plan, we use a Margin Audit™ and Volatility Recovery Analysis to ensure you never have to do that math. By using a 0% floor, we eliminate the "resetting of the clock." Every bit of growth is locked in. This is the difference between "Growth With Loss" (Interrupted gains) and "Growth Without Loss" (Forward momentum).

Choosing Performance Over Participation

Wall Street is a "False Model" driven by greed and fear. When greed is high, they push you into risk. When fear is high, they tell you to "stay the course" while they continue to collect their fees.

We don't "participate" in the market. We use Engineered Performance. We use institutional-grade banking architecture to create Expanded Market Participation (EMP). This allows you to achieve 110% to 200% of the market's upside with none of the downside.

If the market goes up 10%, your EMP multiplier could turn that into an 11% or 20% gain. If the market goes down 30%, you stay at 0%.

That is not a probability. That is a contractual guarantee.

Audit the Margin. Protect Your Time.

If you are a business owner, an engineer, or a corporate executive, you’ve spent your life building. You understand that a bridge doesn't stand because of "hope"; it stands because of structural engineering.

Your retirement should be no different.

Stop settling for the "Choose 2 of 3" trap. Stop letting Wall Street control the variables of your future. It’s time to move from a plan based on "Probabilities" to one built on "Certainty."

The Million Dollar Hour™ Forecast is designed for the Quiet Builder who is ready to unlearn the myths and start looking at the math. We don't do "free cheese" here. We do architecture. We provide a $995 Engineering/Margin Audit that reveals exactly where your plan is leaking and how to heal your balance sheet for life.

Peace is the path, wisdom is the way.

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now