Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Pension vs. 401k vs. FPA: Choosing Guaranteed Income

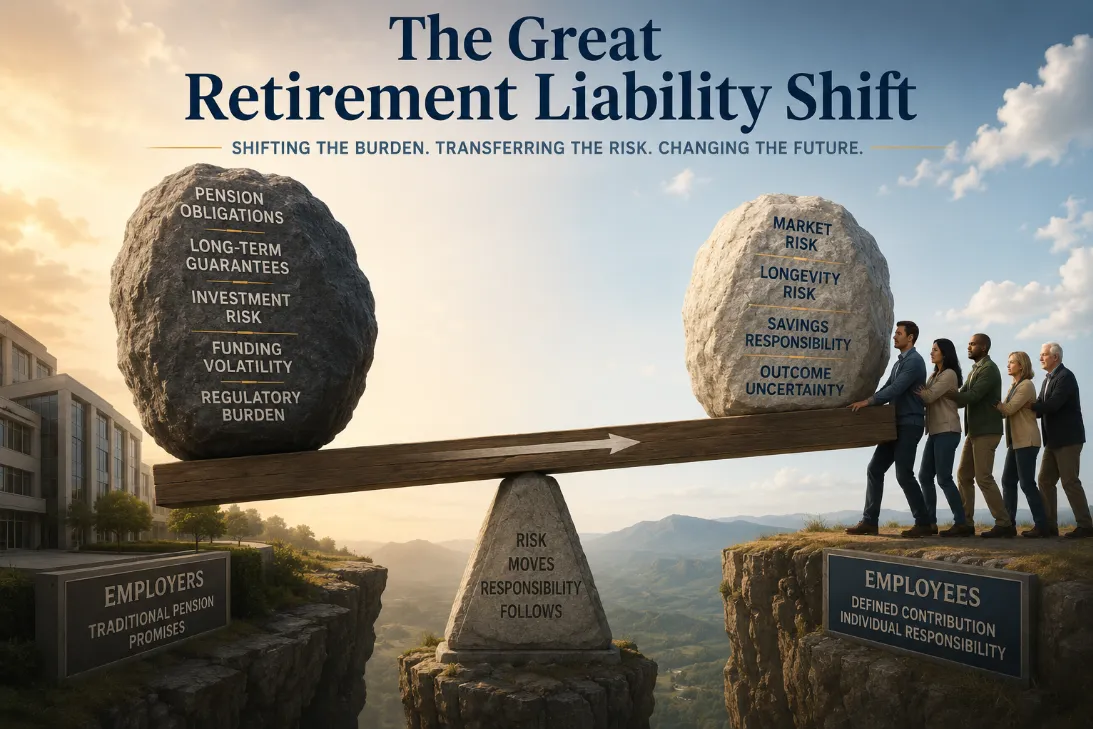

The Great Retirement Liability Shift: Why Your 401(k) is a Corporate Hand-Me-Down

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The Great Retirement Liability Shift: Why Your 401(k) was a Step-Down

In 1975, the American retirement landscape underwent a forensic transformation that most people missed. It wasn’t a headline-grabbing market crash; it was a quiet, structural pivot in Asset Liability Management (ALM).

Before this shift, retirement was built on the "Known." If you worked for a major corporation, they carried the liability of your future on their balance sheet. After 1975, the liability was handed to you, packaged as a "benefit," and renamed the 401(k).

At Your Street Wealth, we call this the Great Retirement Liability Shift. It was the moment Wall Street replaced "Engineering" with "Participation." It was the day the pension’s certainty was traded for the 401(k)’s noise.

If you feel like you’re spinning sharp knives trying to manage your own retirement risk, you aren’t paranoid. You’ve simply been handed a "Rolodex" tool in a "SpaceX" world. It’s time to unlearn the myths of individual liability and return to the principles of institutional-grade architecture.

The 1975 Pivot: From Corporate Certainty to Individual Uncertainty

To understand why your current plan feels fragile, we have to look at the "Before and After" of the mid-70s. This wasn't just a change in accounts; it was a change in who bears the Sequence of Returns Margin.

Pensions (Pre-1975): The Era of the "Known"

Before the shift, retirement was a designed outcome. The corporation acted as the Architect.

Guaranteed Income Level: You knew the number. It was contractual.

Corporate Liability: If the market tanked, the company had to make up the difference. You didn't stay awake at night worrying about "spinning sharp knives" in the bond market.

The Trade-off: While the income was high-certainty, there was no post-life asset value and rarely any spousal continuation. When you passed, the "fountain" stopped.

401(k)s (The Hand-Me-Down): The Era of the "Unknown"

Then came 1974’s ERISA and the 1978 Revenue Act. Corporations realized they could move the liability from their books to yours.

Individual Liability: You became the portfolio manager, the actuary, and the risk officer.

No Guarantees: You were given "Participation" instead of "Performance."

Unlimited Gains & Losses: Wall Street sold you on the "Unlimited Gains," but they buried the "Unlimited Losses" in the fine print.

The Math of Recovery: You were told to "stay the course," ignoring the fact that 30 years of savings can die in 30 months when volatility hits at the wrong time.

Social Security: The $900,000 "Phantom Asset"

Most "Quiet Builders" view Social Security as a simple monthly check. In our Margin Audit™, we view it through the lens of institutional engineering.

If you are receiving a $3,000 monthly check from Social Security, you don’t just have "income." You have the mathematical equivalent of a $900,000 to $1.2 million asset (depending on current safe withdrawal rates).

However, Social Security is a "Single-Pillar" asset. It provides income, but it has zero post-life value. If you pass away tomorrow, that $900,000 "phantom asset" vanishes. It cannot be left to your children. It cannot be used for Long-Term Care (LTC) beyond the monthly check.

This is where the Guaranteed Lifetime Income of a Fully Performing Asset (FPA) changes the math. An FPA can often deliver income that is 150% higher than traditional withdrawal strategies while maintaining the underlying asset for your legacy.

Fully Performing Assets (FPA): The "Smartphone" of Finance

Think about the late 90s. You carried a pager, a cell phone, a digital camera, and a GPS. These were "Single-Pillar" tools. They did one thing, often poorly, and required separate batteries and chargers.

Today, you have a smartphone. It’s a consolidated technology that performs 15+ tasks in one device.

In the financial world, Banks, Stocks, and Real Estate are "Single-Pillar" traditional assets. They are the "pagers" of retirement. They are high-risk or high-fee, and they only do one thing (and usually not with a guarantee).

Fully Performing Assets (FPA) are the "Smartphone" of finance. They consolidate 5 to 15 pillars of value into a single, engineered vehicle:

Guaranteed Present Value (GPV): Knowing what it's worth today.

Guaranteed Future Value (GFV): Knowing exactly what it will be worth when you need it.

Uncapped Gains (UCG): Participating in market upside without the downside.

Expanded Market Participation (EMP): Using multipliers (110%–200%) to outpace traditional indices.

Spousal Continuation: Ensuring the fountain doesn't stop when you do.

LTC Benefits: Built-in protection for health volatility.

Tax-Free Income Potential: Protecting your margin from the government.

While Wall Street operates on a "False Model" driven by greed and fear, an FPA operates on Asset Liability Management (ALM). It is designed to heal your balance sheet through Level Yield Amortization rather than gambling on headlines.

merging into a sleek modern smartphone, mirrored by \"Single Pillar\" financial assets merging into a \"Fully Performing Asset\" triangle.")

The Math of Recovery: Why "Participation" is a Trap

Wall Street wants you to focus on "Average Returns." We focus on Compounding Efficiency.

If your 401(k) "participates" in a 30% market loss, you don’t need a 30% gain to get back to even. You need a 42% gain just to see the surface of the water again. That is "Time Lost," and money can recover, but time never does.

When we conduct a Million Dollar Hour™ Forecast, we move you from the -30%/+30% volatility of Wall Street to the 0%/+30% engineering of Your Street.

By establishing a "Contractual Floor," we ensure that your gains are locked in. You aren't "hoping" for a retirement; you are executing an architectural plan. Peace is the path, and wisdom is the way.

Are You Choosing by the Known or the Unknown?

The "Quiet Builder" doesn't want more "opportunity" language. They've had enough of that. They want Precision. They want to know that their income is designed, not dependent.

The difference between a 401(k) and an FPA is the difference between a "Probability" and a "Guarantee."

Wall Street offers Projections (Hoping).

Your Street offers Contracts (Knowing).

If your current retirement strategy is built on the "Hand-Me-Down" model of individual liability, you are essentially functioning as your own pension manager without the institutional tools to succeed.

It’s time to audit the margin. It's time to protect your time and your wealth.

Your Move: The Million Dollar Hour™ Structural Audit

We don't chase "mice" looking for free cheese. We work with "Architects" who understand that a scrutinized, certain plan is worth the investment.

The Million Dollar Hour™ Forecast is a $995 engineering session designed to last for life. We don't just "look at your statements." We perform a forensic Margin Audit™ to identify exactly how many years you've lost to Wall Street risk and exactly how to engineer a path to guaranteed growth.

Stop participating in a false architecture. Start building on Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement review that reveals where your plan leads : not just where it’s been.

👉 Schedule your session today

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now