Protect Retirement Savings from Market Crash: 4 Wealth Killers

When the Market Peaks (Part 5): The 4 Wealth Killers Stealing Your Retirement

One of the fastest ways to uncover hidden risk is to take our 7 Question Retirement Stress Test.

Start here: See what your retirement actually looks like → 👉 Book Your Million Dollar Hour™

The Stealth Saboteurs: Is Your Retirement Engine Leaking Wealth?

If you’re a "Quiet Builder" trying to protect retirement savings from market crash risk: someone who spent decades scaling the corporate ladder, engineering systems, or building a business: you know that a project is only as good as its architecture. You wouldn't build a skyscraper on a foundation of "hope," and you certainly wouldn't ignore a 30% leak in your fuel line.

Read the Series So Far

Part 3: Why a 10% Market Drop Destroys Retirement Savings Faster

Part 4: Retirement Plan Review: Participation or Architecture?

Yet, most traditional retirement plans are built on exactly that: a "Participation" model where you simply hope the market behaves while ignoring the systemic leaks draining your bucket. That is why a proper retirement plan review matters before the next downturn exposes the cracks.

In this fifth installment of our When the Market Peaks series, we’re moving past the headlines of "market highs" and looking into the dark corners of your portfolio. We are identifying the four "Wealth Killers" that steal your time and money, even when the market looks like it’s winning.

The Disconnect: Participation vs. Engineered Performance

Most Wall Street advice is centered on one word: Participation. They want you to participate in the ups (and the downs) of the market. They use hidden complexity to keep you addicted to the daily research: the "noise."

But for the Quiet Builder, participation is a false architecture. It’s gambling disguised as growth.

Real wealth isn't built on macro headlines; it’s built on micro margins. While the crowd is chasing the next "hot stock," the architect is performing a Margin Audit™. They are looking for the friction, the leaks, and the "Wealth Killers" that make the math of retirement impossible.

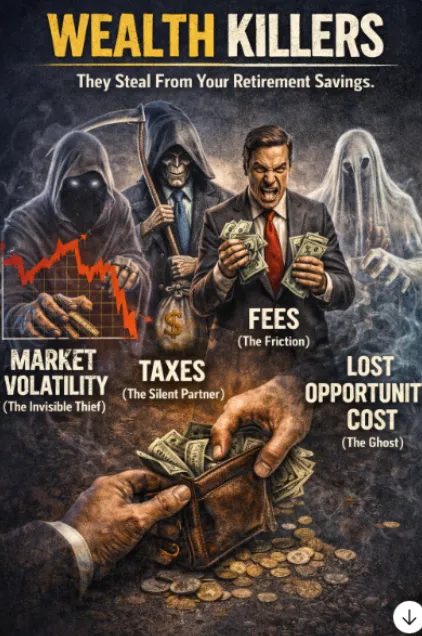

Wealth Killer #1: Market Volatility (The Invisible Thief)

Wall Street tells you that "volatility is normal." They say, "the market always goes up in the long run." That sounds comforting until you actually need to protect retirement savings from market crash conditions instead of just surviving them.

What they don't tell you is the Math of Recovery. Money can recover, but time never does. When you lose 30% of your portfolio, you don’t just need a 30% gain to get back to even. You need a 42.9% gain. If you lose 50%, you need a 100% gain just to see the surface of the water again.

In a "Participation" model, you are spinning sharp knives. When the market peaks and then drops, you aren't just losing money; you are resetting your compounding clock. Every year spent "getting back to even" is a year of your life you will never get back. This is the Sequence of Return Margin: and if you get it wrong in the first five years of retirement, your engine is essentially broken before you even leave the driveway. If your goal is to protect retirement savings from market crash events, you must stop treating volatility like a harmless inconvenience and start treating it like an engineering flaw.

Wealth Killer #2: Taxes (The Silent Partner)

You’ve likely spent your career in the "Single Pillar" world: Banks, Stocks, and Real Estate. These are traditional assets that often carry a heavy, invisible tax burden.

Think of the IRS as your "Silent Partner" who shows up only when you’re successful. If your retirement is sitting in a traditional 401(k) or IRA, you don't actually own that balance. You own a portion of it, and the IRS owns the rest.

When you withdraw money to fund your life, the tax drag acts as a permanent governor on your engine. If you need $10,000 a month to live, but you have to withdraw $13,000 to cover the tax bill, you are depleting your assets 30% faster than you planned. This is a leak in your Compounding Efficiency.

Wealth Killer #3: Fees (The Friction)

Traditional Wall Street products are like a "Rolodex in a SpaceX world." They are single-use, high-friction, and often come with layers of hidden fees.

Management fees, expense ratios, and transaction costs may look like small percentages (1% or 1.5%), but they are calculated on the total balance, not just the profit. Over 20 or 30 years, these fees can consume up to 40% of your total retirement wealth.

This is the "Broken Engine" at work. It’s an extraction system designed to benefit the institution, not the individual. At Your Street Wealth, we look for Fully Performing Assets (FPA): the "smartphones" of finance: that consolidate 5–15 pillars of value (growth, protection, LTC, tax-free income) with fees as low as 0% to 1.5%. For many Quiet Builders, this is where the conversation starts to shift toward the best retirement income strategies: not chasing more noise, but engineering more function from every dollar.

Wealth Killer #4: Lost Opportunity Cost (The Ghost)

The most dangerous Wealth Killer is the one you can’t see on a statement: Lost Opportunity Cost.

When your money is sitting in a "Non-Performing Asset" (like a low-interest savings account) or is lost to market volatility, it’s not just "gone." It’s the future earnings of that money that are gone.

If you lose $100,000 in a market crash at age 60, you haven't just lost $100k. You’ve lost what that $100k would have become by age 80. You’ve lost the Compounding Efficiency of those dollars for the rest of your life.

Wall Street treats your money like a "Participation" game. We treat it like Institutional-Grade Engineering. We use Volatility Recovery Analysis to ensure that your gains are locked in, your principal is protected, and your compounding never resets to zero.

Best Retirement Income Strategies: From Participation to Architecture

Traditional assets (Banks, Stocks, Real Estate) are "single-pillar." They do one thing, often with high risk or high fees.

Fully Performing Assets (FPA) are the foundation of a modern retirement and belong in the conversation about the best retirement income strategies. They provide:

Uncapped Gains (UCG): The ability to capture market upside.

Expanded Market Participation (EMP): A multiplier (often 110%–200%) on those gains.

0% Floors: If the market drops 30%, your account stays at 0%. You never have to do the "Math of Recovery" because you never lost the principal.

When you shift from "Hoping" to "Knowing," you move from a fragile, single-pillar existence to a multi-pillar fortress. You move from the -30% to +30% chaos of Wall Street to the 0% to +30% certainty of Your Street. That shift is why many of the best retirement income strategies are built on engineering, not participation.

Retirement Plan Review: Audit the Margin. Engineer Certainty.

You can estimate your income needs, but you cannot predict future portfolio value when losses and leaks are uncontrollable. Wall Street operates on a "False Model" driven by the Greed/Fear meter. When greed is high, they push you into risk. When fear is high, they sell you "safety" that doesn't grow.

The Million Dollar Hour™ Forecast is designed for the Quiet Builder who is finished with the noise. It is a $995 Engineering/Margin Audit and retirement plan review that scrutinizes your current plan, calculates your true years lost to volatility, and builds a personalized, guaranteed path. If you want a serious retirement plan review instead of another generic opinion, this is where you audit the margin and engineer certainty.

Stop participating in their game. Start engineering yours.

Moving toward the best retirement income strategies starts with a clear retirement plan review.

Peace is the path, wisdom is the way.

Your Money, Your Rules, In Your Time, On Your Street.

Ready for clarity instead of confusion?

The Million Dollar Hour™ is your educational, one-on-one retirement plan review that reveals where your plan leads — not just where it’s been.

👉 Schedule your session today.

Discover Which Wealth Killers Are Affecting You

Most people are impacted by 6–9 and don’t realize it

Wealth Killer #1: The Granddaddy : Why Market Volatility is Your Retirement’s Greatest Enemy

Concerned about market losses, taxes, or income reliability?

Take the 7 Question Retirement Stress Test →

You can keep participating… Or you can finally see the outcome. The Million Dollar Hour™ shows you exactly:

✔ Where you are ✔ Where you’re going ✔ How to fix the gaps 👉 Book your session now