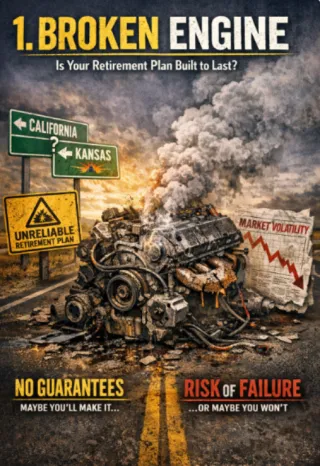

Retirement Strategies That Maximize Income, Eliminate Risk, and Help Ensure You Never Run Out of Money How to Achieve The Retirement Future Everyone Seeks

Most retirement plans are built on assumptions that no longer hold up—market averages, predictable tax rates, and the belief that time will always recover losses. But as you approach or enter retirement, the rules change. What worked during your accumulation years can become a liability during the withdrawal phase.

This blog is designed to help you rethink traditional strategies and discover a more engineered approach to retirement income—one focused on certainty, efficiency, and control.

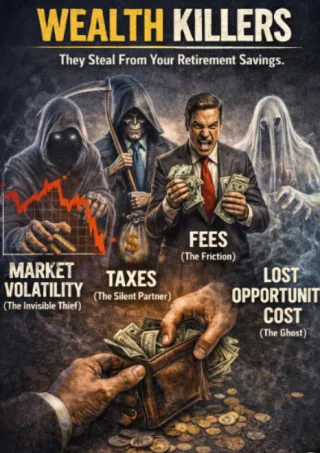

Here, you’ll learn how to reduce or eliminate the biggest threats to your financial future, including market losses, rising taxes, hidden fees, and the silent erosion caused by lost time. We break down complex financial concepts into clear, actionable insights so you can make better decisions about your 401(k), IRA, and retirement income strategy.

You’ll also discover why many conventional approaches—like relying on average returns or the 4% rule—can expose you to unnecessary risk, especially when withdrawals begin. Instead, we explore strategies designed to protect your principal, improve compounding efficiency, and create predictable income streams that last.

Our focus is on helping you transition from “assets at risk” to a more stable and structured approach using fully performing assets—where growth, income, and protection work together instead of against each other.

Whether you’re still working or already retired, the goal is simple:

help you keep more of what you earn, generate more reliable income, and build a plan that doesn’t depend on hope, timing, or market luck.

If you’ve ever wondered:

* How to create tax-efficient retirement income

* How to avoid sequence of returns risk

* How to reduce fees and increase net returns

* How to design income that doesn’t run out

—you’re in the right place.

Explore the articles below and start building a retirement strategy based on engineering, not guesswork.

Retirement Losses vs. FPA: Managing Risk in Retirement

It’s a personal preference. Some people like the texture; they feel it’s more "natural." Others can’t stand it: they want their juice smooth, consistent, and predictable. Either way, you know exactly ... ...more

WOYS - Guarantees ,Time Matters

July 10, 2026•6 min read

Social Security vs IRA: Retirement Income and $5M Risk

You’ve hit the number. You have $1,000,000 sitting in your brokerage account or IRA. You’ve also locked in a Social Security benefit of $40,000 a year. On paper, you’re successful. In the eyes of Wall... ...more

WOYS - Guarantees ,Time Matters

July 10, 2026•10 min read

Social Security Check Compared to IRA

Most people nearing retirement spend 30 years obsessing over a single number: their IRA or 401(k) balance. They check the markets, they sweat the 18-month volatility swings, and they treat their Socia... ...more

WOYS - Guarantees ,Time Matters

July 09, 2026•6 min read

Retirement Savings by Age Costing You MIllions

If you’ve spent any time on the major financial news sites, you’ve seen the charts. You know the ones: the “Retirement Savings by Age” benchmarks from industry giants like Fidelity or Vanguard. They t... ...more

WOYS - Guarantees ,Time Matters

July 09, 2026•7 min read

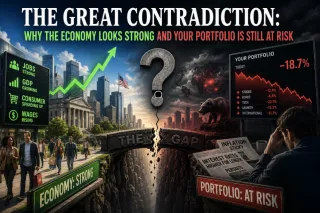

Why the Strong US Economy Could Risk Your Retirement Portfolio

It’s the great contradiction of our time. You turn on the news and see talk of reshoring, massive capital inflows, and a US economy that looks like the only clean shirt in a very dirty global laundry... ...more

WOYS - Guarantees ,Time Matters

July 09, 2026•9 min read

Why Most People Never Build Wealth and Why You Will

Everybody Wants $1 Million. Few are willing to become the person who can build it. Everyone asks, "What investment should I make?" Almost no one asks, "What must I learn to become wealthy?" See the di... ...more

WOYS - Guarantees ,Time Matters

July 09, 2026•4 min read

Follow the Masses or Find a Better Way?

Down the left path, you’ll find the masses. It’s a well-trodden road lined with familiar signs: "Buy and Hold," "Diversification is Your Only Protection," and "The Market Always Goes Up in the Long Ru... ...more

WOYS - Guarantees ,Time Matters

July 08, 2026•7 min read

Trump Accounts vs. Wall Street Cycle | Your Street Wealth

Every few years, Wall Street and Washington team up to sell a new "Shiny Object." Today, it’s the Trump Account. On the surface, it looks like a gift: tax-advantaged growth, low fees, and a "set-it-an... ...more

WOYS - Guarantees ,Time Matters

July 08, 2026•10 min read

Top 10 Causes of Market Retractions

If you’ve spent any time on Wall Street, you’ve been sold the Shiny Object. You know the one: it’s that glowing 7–10% "average annual return" mirage that brokers dangle to keep you "participating" in ... ...more

WOYS - Guarantees ,Time Matters

July 08, 2026•9 min read

Why You Must Inspect What You Expect Authenticity

If you walked into a coin shop and handed over $35 for a 2023 Silver American Eagle, there’s a good chance you’d take a moment to look at it. You’d check the date. You’d look for the "W" mint mark. Yo... ...more

WOYS - Guarantees ,Time Matters

July 08, 2026•6 min read

Three Wealth Levels, Three Retirement Myths to Unlearn

Too many people view retirement as a finish line where they can finally "switch off." But in the world of finance, a fixed mindset is a dangerous liability. Whether you have $100,000 or $100 million, ... ...more

WOYS - Guarantees ,Time Matters

July 07, 2026•11 min read

1929 vs. 2029: The Truth About Market Retractions

The question is everywhere. It’s whispered in the halls of corporate offices and shouted on financial news networks: “Is there anything to stop the market from reaching 90,000 by 2029?” After 50+ reco... ...more

WOYS - Guarantees ,Time Matters

July 07, 2026•6 min read

The Three Lives of Wealth: Engineering Generational Legacy

Over the last four parts of this series, we’ve deconstructed the "Wealth Engine" from the ground up. We’ve audited the margin, stripped away the hidden fees of the Wall Street "Dark Object," and insta... ...more

WOYS - Guarantees ,Time Matters

July 07, 2026•10 min read

Planning for Healthcare Costs in Retirement

Ask any "Quiet Builder": the successful professional or business owner between 45 and 75: what keeps them up at night, and the answer is almost always a variation of the same two fears. First, they fe... ...more

WOYS - Guarantees ,Time Matters

July 07, 2026•7 min read

How to Stop Market Volatility from Stealing Retirement Years

Welcome to the finale. Over the last nine installments of our Wealth Engine series, we’ve deconstructed the mechanics of wealth, exposed the leaks in traditional portfolios, and built a blueprint for ... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•6 min read

Why Interrupted Compounding Kills Retirement Wealth

Most people believe that to build wealth, you simply need to "be in the market" and wait. They’ve been sold a narrative that a 7% or 10% "average annual return" is the golden ticket to a secure retire... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•6 min read

Protect Forward Progress: Discipline 3 of Retirement Wealth

Most people spend their entire working lives running at full tilt. They check the markets daily, tinker with their 401(k) allocations, and listen to the "experts" on TV bark about the next hot sector.... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•6 min read

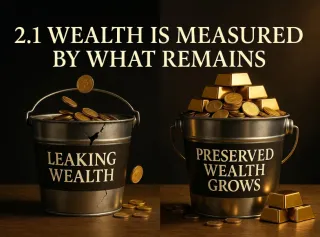

The "What Remains" Rule: Protecting Your Retirement Wealth

Most people spent their entire careers focused on a single number: the "Top Line." They look at their contributions, their salaries, and the "average returns" promised by their Wall Street brokers. B... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•6 min read

Why Protecting Principal is the Key to Retirement Growth

Welcome to Part 6 of our Wealth Engine series. If you’ve been following along, you know we’ve spent the last few weeks dismantling the "Wall Street Cycle" and exposing why most retirement plans are bu... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•7 min read

The Three Lives of Wealth: Engineering Generational Legacy

Over the last four parts of this series, we’ve deconstructed the "Wealth Engine" from the ground up. We’ve audited the margin, stripped away the hidden fees of the Wall Street "Dark Object," and insta... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•7 min read

6 Thinking Shifts Every Retiree Must Make

Most people spend their entire working lives following a "map" that was never designed to get them through retirement. They’ve been taught to focus on Accumulation, to obsess over Average Returns, and... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•6 min read

Engineering Growth Without Risk: The Multiplier Effect

Most investors believe that to get more growth, you must take more risk. They’ve been conditioned by decades of Wall Street marketing to view their retirement like a casino: if you want a bigger jackp... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•7 min read

Stop the Leak: Are Your Retirement Dollars Loitering or Working?

If you walked into your business or office on a Tuesday morning and saw half your staff leaning against the water cooler, scrolling through their phones while the phones on their desks rang off the ho... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•7 min read

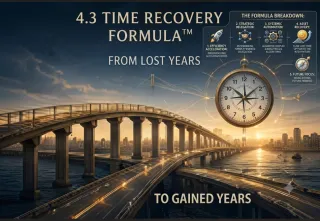

Reclaiming Lost Years: The 4.3 Time Recovery Formula™

You’ve probably heard the old Wall Street adage: "It’s not about timing the market; it’s about time in the market." It sounds wise. It sounds patient. It sounds like something a person in a tailored s... ...more

WOYS - Guarantees ,Time Matters

July 06, 2026•6 min read

Annual Returns vs. Lifetime Income: Which Is Better?

If you’ve spent any time in the traditional financial world, you’ve been conditioned to ask one primary question every December: "How much did my portfolio grow this year?" It’s a natural question. It... ...more

WOYS - Guarantees ,Time Matters

July 03, 2026•7 min read

Why Everyone Is Talking About the Million Dollar Hour™

You’ve been told that if you just participate in the market, follow the "4% rule," and "buy and hold" through the dips, you’ll eventually have enough to retire. But for the Quiet Builder: the business... ...more

WOYS - Guarantees ,Time Matters

July 02, 2026•6 min read

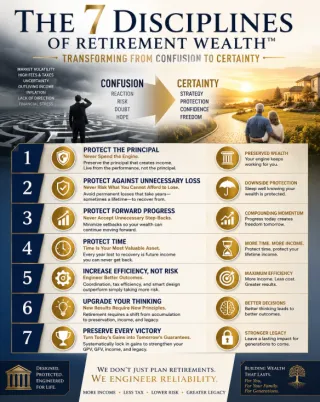

7 Disciplines. One Framework. No More Guessing.

Retirement wealth is not built byIf you are a successful professional or business owner between the ages of 45 and 75, you’ve likely spent decades following a specific set of rules. You were told to s... ...more

WOYS - Guarantees ,Time Matters

June 30, 2026•8 min read

Lifetime ICA™ Analysis: Present Value of Retirement Income

In the world of traditional Wall Street "participation," there is one number that rules them all: the Account Balance. It’s the number at the top of your monthly statement. It’s the number you track o... ...more

WOYS - Guarantees ,Time Matters

June 29, 2026•6 min read

Does Your Retirement Plan Pass the SMART Test?

If you’ve spent any time in a corporate boardroom or managing a complex engineering project, you know the drill: Specific, Measurable, Achievable, Relevant, and Time-Bound. These five pillars are the ... ...more

WOYS - Guarantees ,Time Matters

June 29, 2026•6 min read

How to Outrun Inflation Without Risking Lifestyle

It’s called Wealth Killer #4: Declining Income and Inflation. In the world of the Engineered Retirement Blueprint, we look at your life through two lenses: the Balance Sheet (the Source of Funds) and ... ...more

WOYS - Guarantees ,Time Matters

June 28, 2026•6 min read

Retirement Planning Fees: Wall Street vs. Your Street

When most people review their retirement plan, they get fixated on a single number: the fee percentage. They look at 1% here or 1.5% there and try to shop for a "deal" as if they are buying a gallon o... ...more

WOYS - Guarantees ,Time Matters

June 27, 2026•6 min read

Stop Paying Fees Without Value Add: 3rd Wealth Killer

If you are a “Quiet Builder”: someone who has spent thirty years working, saving, and avoiding the noise of the nightly news: you probably think you know what your retirement costs. You see the line i... ...more

WOYS - Guarantees ,Time Matters

June 27, 2026•6 min read

Stop Paying Taxes Legally in Retirement | Your Street Wealth

You are currently in a joint venture with the Internal Revenue Service. They didn't help you earn the money, they didn't take the market risk, and they didn't stay up late worrying about your "number.... ...more

WOYS - Guarantees ,Time Matters

June 27, 2026•6 min read

Stop Losing Money: Avoid Retirement Sequence of Returns Risk

If you are a “Quiet Builder”: the business owner, the retired engineer, or the executive who spent 30 years stacking capital: you’ve likely been told the same three-word lie for decades: "Ride it out.... ...more

WOYS - Guarantees ,Time Matters

June 27, 2026•6 min read

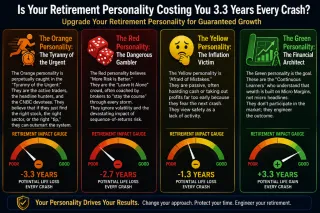

Retirement Personality Has An Impact on Your Future

In the world of wealth, there are two types of people: those who participate in a system designed to extract value from them, and those who engineer a system designed to work for them. If you are a "Q... ...more

WOYS - Guarantees ,Time Matters

June 27, 2026•7 min read

Why Your Retirement Needs an Upgrade

Elon Musk didn’t build SpaceX by following the "traditional" aerospace playbook. He didn't look at Boeing or NASA and say, "Let’s do exactly what they’re doing, but with a cooler logo." He used First ... ...more

WOYS - Guarantees ,Time Matters

June 26, 2026•6 min read

How to Stop the 7 Retirement Wealth Killers Now

The easiest way to elevate your retirement isn't by finding the next "hot" stock or chasing a rogue 7% average return. It’s simpler, more surgical, and infinitely more effective. Stop doing what is ne... ...more

WOYS - Guarantees ,Time Matters

June 26, 2026•5 min read

How Much Do I Need to Retire at 65?

When you are no longer contributing and now taking income, the market stops being a scoreboard and starts becoming a stress test. This is the Orange Zone. Income exposes the lie. Wall Street says, “J... ...more

WOYS - Guarantees ,Time Matters

June 25, 2026•8 min read

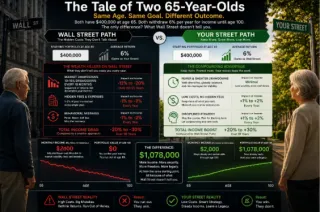

The $1.3 Million Retirement Trap: Why 55 is the Critical Turning Point

Here is the actual setup for our 55-year-old "Quiet Builders." Two investors both start with $75,000. Both contribute $600 per month. Both are shown 5% average annual gains. Both begin taking 4% incom... ...more

WOYS - Guarantees ,Time Matters

June 25, 2026•9 min read

How Much Do I Need to Retire at 45?

Math should be objective. If two people start at the same age, with the same money, contribute the same amount every month, and both receive a 5% average annual gain, they should land in the same plac... ...more

WOYS - Guarantees ,Time Matters

June 25, 2026•10 min read

The 50% Starter: Reallocate Like Wall Street Does

Something is happening in Uptown Dallas. If you walk down Ross Street or Field Street, you aren't just seeing new glass towers; you’re seeing the physical reallocation of the world’s most sophisticate... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•6 min read

Is It Possible for Two 35-Year-Olds to Get Different Retirements?

If you’ve ever sat across from a financial advisor, you’ve likely been fed the “Shiny Object.” You know the one: a colorful chart showing a steady 7% to 10% average annual return over the next thirty ... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•6 min read

Why Two 25-Year-Olds Get Different Outcomes

Both start with $10,000 in their pockets. Both commit to saving $100 every single month. Both are told by their respective advisors that they can expect a "5% growth rate" over a lifetime. On paper, t... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•8 min read

The Market Will Retract. Here's What Triggers It.

If you’ve spent any time on Wall Street, you’ve been sold the Shiny Object. You know the one: it’s that glowing 7–10% "average annual return" mirage that brokers dangle to keep you "participating" in ... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•8 min read

7 Mistakes You’re Making with Your Retirement Plan Review

Most retirement "reviews" are about as useful as checking the weather report for the day that already happened. You sit down with a broker, they show you a few colorful pie charts, tell you that "the ... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•7 min read

Why Retirement Needs 100% Focus and Why That’s Impossible

Look around next time you’re at a stoplight. Half the drivers are looking down. Their hands are on the wheel, but their minds are miles away, buried in a device that has consolidated their entire worl... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•7 min read

Why 94% of Retirement Plans Fail (And How to Fix Yours)

If you feel like your retirement planning is a constant tug-of-war between "hoping for the best" and "fearing the worst," you aren't alone. In fact, you are likely caught in a very specific, very inte... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•7 min read

Retirement Income Planning: Needs an Emergency Action Plan

You have a fire escape plan for your home. You have a backup generator for your business. You likely have a medical directive for your health. But when it comes to the money you intend to live on for ... ...more

WOYS - Guarantees ,Time Matters

June 24, 2026•6 min read

10 Flaws of Your Retirement Income Calculator

You’ve seen it. That glowing green "on-track" light at the end of a free retirement income calculator. It feels good, doesn't it? Like you’ve finally cracked the code, and the next 30 years are just a... ...more

WOYS - Guarantees ,Time Matters

June 23, 2026•7 min read

3.3-Year Tax: The Wealth Killer Wall Street Won't Mention

You are familiar with the IRS. You know how to track capital gains, income tax, and property levies. You might even have a strategy to minimize them. But there is another tax: one that is far more pre... ...more

WOYS - Guarantees ,Time Matters

June 23, 2026•9 min read

Why Wall Street's Balance Sheet Has Never Balanced

If Wall Street’s own titans admit the cycle keeps repeating, and only about 3% of people truly succeed there through a mix of skill and luck, why are so many retirees still being told to "just stay th... ...more

WOYS - Guarantees ,Time Matters

June 23, 2026•7 min read

Level Yield Amortization Healing Retirement Balance Sheet

If you’ve spent the last 30 years building a business, managing complex corporate systems, or designing structures that cannot fail, you know one thing to be true: Hope is not a strategy. ...more

WOYS - Guarantees ,Time Matters

June 23, 2026•6 min read

Why Your Brokerage Statement Hides Real Retirement Growth

If you are a "Quiet Builder": a business owner, a retired engineer, or a former corporate executive: you value precision. You appreciate a blueprint that works because the math says it must, not becau... ...more

WOYS - Guarantees ,Time Matters

June 23, 2026•6 min read

Implementation Guide for Wealth Architecture

But here is the hard truth that most "financial advisors" won't tell you: Architecture without implementation is just expensive wallpaper. Knowing that your 401(k) is a "Mirage" or that Wall Street is... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

Golf vs. Retirement: The Math of a Repeatable Plan

If you’ve ever stood on the tee box of a long par five, staring down a narrow fairway with water on the left and out-of-bounds on the right, you know the temptation. You want to crush it. You tighten ... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•8 min read

The Architect's Toolbox: 5 Retirement Planning Instruments

In Level 1 of the Your Street Wealth Academy, we identified the fundamental flaw in the "Good Enough" retirement plan. We exposed the difference between Participation (the Wall Street gamble of hoping... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•5 min read

Why 'Good Enough' Retirement Plans Fail: The Level 1 Shift

If you’ve found your way here, it’s likely because you’ve reached a level of success that most people only dream of. You’ve worked hard, you’ve saved, and you’ve "participated" in the systems you were... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

Wall Street T+1 Settlement & Retirement Planning Risks

On May 17, 1792, twenty-four brokers and merchants gathered under a buttonwood tree at 68 Wall Street. They signed a brief, two-sentence document: the Buttonwood Agreement: that effectively birthed th... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

The Legacy Layer: Passing Wealth, Not Just Assets

Most people believe that filling out a beneficiary form on their IRA or 401(k) is "legacy planning." They assume that the number they see on their monthly statement today will be the same number their... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

Annuities Pros and Cons for Retirement Income Planning

Imagine you started a business with a partner. This partner never helps with the strategy. They don’t help you find customers, they don’t manage the staff, and they certainly don't chip in when the bu... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

Best Retirement Income Strategies to Beat Inflation

If you’ve been following the traditional Wall Street script, you’ve likely been told that the "4% Rule" is the gold standard. You take 4% of your nest egg in year one, adjust for inflation each year, ... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•5 min read

Social Security Timing Trap: When Waiting Until 70 Fails

Conventional Wall Street wisdom is a lot like a GPS that only tells you to "go north." It sounds simple, it’s easy to repeat, but if you’re already at the North Pole, it’s remarkably unhelpful. ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•5 min read

The Lifetime Income Blueprint: Best Retirement Income Strategies

If you are a "Quiet Builder": someone who has spent the last 30 years working hard, saving diligently, and navigating the noise of the headlines: you’ve likely asked yourself the same question every m... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

Margin Audit: 5 Hidden Leaks Draining Your Retirement Savings

Most people watch the stock market headlines like they’re checking the weather. They see the S&P 500 go up 10% and think, "I’m 10% closer to my dream." But wealth isn't built on macro headlines. It’s ... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

The 0% Floor Blueprint: Guaranteed Retirement Strategy

They tell you to ride the roller coaster, stay the course, and wait for the "inevitable" recovery. But for a Quiet Builder: someone between the ages of 45 and 75 who has worked hard to stack their chi... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•6 min read

401(k) Execution: The Truth About Retirement Outcomes

Everyone tells you the same story. If you just "participate" long enough, max out your contributions, and pick the right "target-date" fund, you’ll reach the finish line with a mountain of gold. They ... ...more

WOYS - Guarantees ,Time Matters

June 22, 2026•7 min read

Asset Pyramid: The Best Retirement Income Strategy

Most people approaching retirement have been taught to build their financial lives like a one-story ranch house. You put all your money into one big "room": usually a 401(k) or a brokerage account: an... ...more

WOYS - Guarantees ,Time Matters

June 21, 2026•6 min read

401k v Fully Performing Asset Which Is Better For Your Margin

For decades, the 401(k) has been marketed as the gold standard of retirement planning. But for the "Quiet Builder", the business owner or executive with a significant nest egg and a desire for reliabi... ...more

WOYS - Guarantees ,Time Matters

June 21, 2026•6 min read

How to Choose the Best Retirement Strategy: 6 Power Pairs

Most retirement plans are built on a foundation of "Participation." You participate in the market, you participate in the risk, and you participate in the hope that everything works out. But hope is n... ...more

WOYS - Guarantees ,Time Matters

June 21, 2026•6 min read

The Architect's Toolbox: 5 Retirement Instruments

If you’ve been following the Retirement Reliability Academy, you’ve already survived the diagnosis. You’ve seen The Four Hidden Killers eating away at traditional portfolios. You’ve recognized the Sur... ...more

WOYS - Guarantees ,Time Matters

June 21, 2026•7 min read

Retirement Moment of Inertia Explained

Retirement Moment of Inertia is when the mass becomes unstable to a desired trajectory. The mass of any individual's retirement portfolio is so small, it’s microscopic relative to the size of the enti... ...more

WOYS - Guarantees ,Time Matters

June 21, 2026•6 min read

Retirement Survivorship Bias: The Hidden Cost of Lost Time

The truth is, what you can see is what Wall Street wants you to see. They want you focused on the "Daily Noise" and the "Macro Headlines." They want you addicted to the buying and selling of "Single-P... ...more

WOYS - Guarantees ,Time Matters

June 21, 2026•6 min read

The 4 Hidden Retirement Killers Experts Miss

In 1941 the U.S. Navy had a problem. They had the most sophisticated weapon in the world: the Mark 14 torpedo. It was a marvel of engineering, costing $10,000 a piece (a fortune at the time) and desig... ...more

WOYS - Guarantees ,Time Matters

June 20, 2026•7 min read

Casino Strategy vs. Retirement Certainty Blueprint

Wall Street operates on the exact same psychological playbook. They’ve spent decades training you to believe that "participation" in the market is the only way to build wealth. They use hidden complex... ...more

WOYS - Guarantees ,Time Matters

June 18, 2026•8 min read

Retirement Income Planning: The 5 D’s of Wealth Deficiency

If you’ve been following our work at Your Street Wealth, you’ve likely seen The 5 D's of Wealth Destruction. Those are the catastrophic events: Denial, Decisions, Downturns, Divorce, and Death: that c... ...more

WOYS - Guarantees ,Time Matters

June 18, 2026•7 min read

Protect Retirement Savings from Market Crash: The 5 D's

Most financial planning is an exercise in hope. You sit across from a professional who shows you colorful "Monte Carlo simulations": essentially a weather report for your money based on the last 50 ye... ...more

WOYS - Guarantees ,Time Matters

June 18, 2026•6 min read

CPA vs. Retirement Planning: Avoid the Compliance Trap

Most high-net-worth individuals and business owners have a "favorite" professional: their CPA. We get it. Your CPA is the person who keeps the IRS off your porch and ensures your filings are "correct.... ...more

WOYS - Guarantees ,Time Matters

June 18, 2026•6 min read

Why Not Needing a Retirement Fund is Your Biggest Risk

I see it often in my office: the "Quiet Builder": the business owner, the retired engineer, the former corporate executive: who looks at their portfolio and thinks, "I am so wealthy I don't need to se... ...more

WOYS - Guarantees ,Time Matters

June 18, 2026•6 min read

Executive Retirement Plan Protect Savings from Market Risk

You’ve spent decades climbing the ladder. You’ve navigated the politics, the late-night board decks, and the high-stakes decisions. Now, looking at your balance sheet, you see the fruits of that labor... ...more

WOYS - Guarantees ,Time Matters

June 17, 2026•7 min read

401(k) vs IRA: The 40-Year Trap and Hidden Admin Costs

Most people treat their 401(k) like a "set it and forget it" machine. You sign a few papers during HR orientation, pick a target-date fund because it sounds safe, and assume that in 30 or 40 years, th... ...more

WOYS - Guarantees ,Time Matters

June 17, 2026•7 min read

The Retraction Tax: Protect Retirement from Market Crashes

It sounds patient. It sounds wise. It sounds like a plan. But for someone between the ages of 45 and 75: the "Quiet Builders" of the world: it is one of the most dangerous lies in finance. It’s a myth... ...more

WOYS - Guarantees ,Time Matters

June 17, 2026•6 min read

2026 vs 1929: Is a Market Crash Coming? | Your Street Wealth

It is the ghost of 1929, and it is staring back at us through a 100-year mirror. The reflection is eerily familiar: a market so drunk on its own success that greed is no longer a whisper; it’s an oozi... ...more

WOYS - Guarantees ,Time Matters

June 17, 2026•7 min read

Your Average Return is an Engineering Fail

In your professional life, if a system has a 10% friction loss, you don't call it "successful": you call it a design flaw. You audit the margins. You tighten the tolerances. You ensure the output matc... ...more

WOYS - Guarantees ,Time Matters

June 16, 2026•6 min read

Great Financial Disconnect is so good

If I had a nickel for every time a successful business owner or retired executive said those words during a Million Dollar Hour™, I wouldn’t need to manage money. I’d just retire on the nickels. It’s ... ...more

WOYS - Guarantees ,Time Matters

June 16, 2026•7 min read

CEO Wealth Leakage: Auditing Your Retirement Strategy

You’ve spent decades building an empire. You understand margins, you’ve mastered the P&L, and you can spot a weak operational process from a mile away. In your industry, you are a titan: a “Whale.” Yo... ...more

WOYS - Guarantees ,Time Matters

June 16, 2026•6 min read

Retirement Planning: The Cost of Inaction is HIGH

You’ve seen the invitations: "Free steak dinner and a retirement consultation!" or "Complimentary portfolio review!" To the "Quiet Builder": the successful professional or business owner who has spent... ...more

WOYS - Guarantees ,Time Matters

June 15, 2026•5 min read

Sequence of Returns Risk: Why Your First 3 Years are Dangerous

But there is a mathematical cliff that Wall Street rarely mentions. It’s called Sequence of Returns Risk, and it is the single most dangerous variable in your financial life between the ages of 60 and... ...more

WOYS - Guarantees ,Time Matters

June 15, 2026•6 min read

Everything is a Business Case: Wall St. vs. Compounding

When you go to the fair, you might decide to shell out $55 for a ticket to the big rollercoaster. It’s a transaction. You invest 15 minutes of your life standing in a hot, crowded line for the privile... ...more

WOYS - Guarantees ,Time Matters

June 15, 2026•6 min read

2028 Virtual Migration: Escaping Corrosive Taxes

Washington has fired a warning shot. Starting in 2028, a new 9.9% tax on high-earners is set to go live, stacking on top of existing capital gains taxes and one of the steepest estate taxes in the nat... ...more

WOYS - Guarantees ,Time Matters

June 15, 2026•6 min read

Raptor 4 Retirement vs. Traditional Market Risk Strategies

While the majority of retirees are still trying to navigate a SpaceX-speed world using a 1970s Rolodex, a small group of "Quiet Builders" has moved beyond the noise. They aren't "participating" in the... ...more

WOYS - Guarantees ,Time Matters

June 15, 2026•11 min read

Best Retirement Income Strategies: Engineering Success

Imagine you are sitting at the head of a mahogany table. This is your Personal Board Meeting. You are the CEO of your life, and your most important division: the Retirement Division: is presenting its... ...more

WOYS - Guarantees ,Time Matters

June 14, 2026•10 min read

Guaranteed Retirement Income vs. Wall Street Risk

Imagine you are sitting at the head of a mahogany table for your "Personal Board Meeting." On one side sit the "Market Enthusiasts": the brokers who tell you to "stay the course" and "ride out the vol... ...more

WOYS - Guarantees ,Time Matters

June 14, 2026•6 min read

How Much I Need to Retire? Real Truth About Your Number

The standard Wall Street advice usually boils down to a single, static number. They tell you to aim for $1 million, $2 million, or maybe 25 times your annual spending. They call it "The Number." ...more

WOYS - Guarantees ,Time Matters

June 14, 2026•6 min read

Questions to Expose the Truth About Your Retirement

When the market is up, they want you greedy, buying the hype, participating in the "noise," and paying their fees for the privilege. When the market is down, they want you fearful, staying the course,... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•7 min read

Why CEOs Need a Forensic Margin Audit for Retirement

As a CEO, Managing Partner, or high-level Engineer, you would never allow your company to operate on "vibes" or "participation." You don't just "participate" in your industry; you engineer outcomes. Y... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

Why Traditional Retirement Income Calculators Fail

If you’ve spent any time on a big-box brokerage website lately, you’ve probably played with their retirement income calculator. You plug in your age, your current nest egg, and a "modest" 7% return. S... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

The Compounding Lie: Why Your Nest Egg Isn't Growing

If you’ve spent the last twenty years diligently "participating" in the market, you’ve likely been fed a steady diet of the same Wall Street gospel: “Just stay the course. Compounding will do the heav... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

How to Protect Retirement Savings From a Market Crash

If you are a "Quiet Builder": someone who spent decades building a career, a business, or a corporate legacy: you probably feel a nagging sense of unease. You’ve done the work. You’ve filled the nest ... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•7 min read

When the Greed Meter Hits Red: Take Retirement Gains Now

With the market hitting over 50 new highs in a single 12-month period, the "Greed Meter" isn't just high: it’s pinned in the red. Everywhere you look, there’s a new rocket ship to board. Whether it’s ... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

Wall Street Shiny Objects: Why They Won't Save Retirement

Right now, it’s the SpaceX IPO rumors and the explosion of AI. These are the "shiny objects" of the day: the high-octane rockets that promise to launch your portfolio into the stratosphere. But here i... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•5 min read

Retirement Plan Review: How a HUD Secures Lifetime Income

Most retirement planning is built on a "North Star." You know the one: it’s that distant point of light representing the dream. It’s the cabin in the woods, the world travel, or the simple peace of kn... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

Retirement Income Planning Finding Retirement North Star

Most retirement planning today feels like being trapped in a math-induced trance. You’re staring at a spreadsheet of probabilities, watching a Monte Carlo simulation tell you that you have an “82% cha... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

Retirement Income Planning: How to Build a Strategic HUD

Imagine you’re the pilot of a high-performance aircraft. You’re at 35,000 feet, cruising toward a destination you’ve spent forty years preparing to reach. Suddenly, a thick fog rolls in. You look out ... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•7 min read

The Retirement HUD: Best Retirement Income Strategies

In the cockpit of a modern jet, a pilot has a Heads-Up Display (HUD). It allows them to stay focused on the horizon while critical data: altitude, airspeed, and trajectory: floats right in front of th... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

End the Hustle Stop Managing Risk Start Consuming Life

You’ve spent thirty years building. You’ve navigated the corporate ladders, the business pivots, and the late-night spreadsheets. You’ve won the game of accumulation. But as you look toward the finish... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•6 min read

What’s Fueling Your Retirement

Most people think of retirement as a destination: a finish line where the work stops and the golf starts. But if you’re a "Quiet Builder," someone who has spent decades accumulating success, you know ... ...more

WOYS - Guarantees ,Time Matters

June 13, 2026•5 min read

Retirement Income Planning: Process vs Product Comparison

If you’re a "Quiet Builder": someone who spent the last thirty years quietly stacking wins, managing teams, and building a life: you’ve likely reached a stage where the "hustle" has lost its charm. ...more

WOYS - Guarantees ,Time Matters

June 12, 2026•7 min read

Inspect What you Expect 10 Brutal Questions You Need to Ask

Most people are loyal to their broker, their banker, or a brand name they’ve seen on a stadium. But in a 60-year retirement plan, that loyalty can become a barrier to the healthy scrutiny required to ... ...more

WOYS - Guarantees ,Time Matters

June 12, 2026•8 min read

Engineered Retirement vs. Wall St Risk | Your Street Wealth

You could take a car to a boat, hop on a train, board a commercial jet, or: if you’re looking for the ultimate efficiency: ride a SpaceX rocket. Each mode of travel has a different cost, a different s... ...more

WOYS - Guarantees ,Time Matters

June 12, 2026•7 min read

Best Retirement Income Strategies: Guaranteed Income Guide

You’ve spent thirty years building, scaling, and engineering a life of success. You’ve navigated market cycles, survived corporate shifts, and likely built a balance sheet that makes most people's hea... ...more

WOYS - Guarantees ,Time Matters

June 11, 2026•6 min read

Wholesale Wealth Stop Paying Retail Prices for Your Money

When you keep your wealth in traditional "Single Pillar" assets: standard bank accounts, basic stocks, or traditional real estate: you are operating at retail. You are accepting the lowest possible va... ...more

WOYS - Guarantees ,Time Matters

June 11, 2026•7 min read

Tripling: The Math Wall Street Hopes You Never Do

Most people know the Rule of 72. It’s that handy little mental shortcut that tells you how long it takes for your money to double. If you earn 10%, your money doubles every 7.2 years. If you’re stuck ... ...more

WOYS - Guarantees ,Time Matters

June 10, 2026•7 min read

Rule of Doubling: Protect Retirement Savings from Market Crash

For the "Quiet Builder": the business owner, the retired engineer, or the former corporate executive: retirement isn’t about "winning big." It’s about not losing. It’s about protecting the time and we... ...more

WOYS - Guarantees ,Time Matters

June 10, 2026•5 min read

Finding Hidden Wealth in Your Retirement Plan Review

We hunt for it in every corner of the balance sheet. We look for synergies in People, Process, Production, Projection, and Performance. Why? Because synergy is the closest thing to a "free lunch" in t... ...more

WOYS - Guarantees ,Time Matters

June 10, 2026•5 min read

Why Retirement Calculators Lie: Real Income Strategies

If you’ve spent any time on a big-bank website lately, you’ve seen it: the "Retirement Nest Egg Calculator." You punch in your age, your current savings, and: presto!: a colorful bar chart tells you t... ...more

WOYS - Guarantees ,Time Matters

June 10, 2026•6 min read

Four Questions of Retirement Quality: Why 'How Much'

They go to a "Big Box" brokerage, use a retirement calculator that makes a dozen rosy assumptions, and walk away with a "number" that feels like a security blanket. But here’s the cold, hard truth: "H... ...more

WOYS - Guarantees ,Time Matters

June 10, 2026•7 min read

The One Question with Three Different Answers. How Much

If you are nearing retirement, you’ve likely spent late nights staring at a calculator screen, typing in various numbers, and asking the same question over and over: "How much do I need to retire?" ...more

WOYS - Guarantees ,Time Matters

June 10, 2026•7 min read

Retirement Math: Why Your Strategy Needs to Grow Up

But in the world of retirement planning, many "Quiet Builders" are still living that adolescent fantasy. They are waiting for a DeLorean that isn’t coming. They are hoping that the market will "eventu... ...more

WOYS - Guarantees ,Time Matters

June 10, 2026•6 min read

Math Matters Retirement Calculator is False Sense of Security

If you’ve spent any time planning for your future, you’ve likely seen it: the "Green Light." You plug your current savings, your age, and a hypothetical "7% average return" into a sleek online retirem... ...more

WOYS - Guarantees ,Time Matters

June 09, 2026•7 min read

QSG Retirement Plan Review Do This First

Let’s be honest: most people do not avoid a Retirement Plan Review because they are too busy. They avoid it because they are afraid. Afraid the review will uncover a leak. Afraid it will expose a mist... ...more

WOYS - Guarantees ,Time Matters

June 09, 2026•6 min read

Main St vs Wall St vs Your St Where Does Your Retirement

In our world at Your Street Wealth, we’ve found that almost every retirement plan in America resides on one of three streets. Where you choose to park your life savings determines whether you’ll spend... ...more

WOYS - Guarantees ,Time Matters

June 09, 2026•6 min read

Choosing Peace & Wisdom Over the Wall Street Rollercoaster

If you’ve ever stood on the edge of a high-speed transit platform, you know that proximity matters. Stand too close to the yellow line, and the wind from the passing train will pull at you. Move back ... ...more

WOYS - Guarantees ,Time Matters

June 09, 2026•6 min read

Retirement Math Trap: Why Your 'Number' Is a Lie

The question is ubiquitous. It’s the holy grail of financial planning. You’ve seen it on the covers of magazines, heard it in late-night commercials, and likely plugged your data into a dozen differen... ...more

WOYS - Guarantees ,Time Matters

June 09, 2026•7 min read

Your Money, Your Rules: The Choice You Didn’t Know You Had

For decades, we’ve been told that "Wall Street" is the only street. We’ve been conditioned to believe that volatility is the price of admission for growth, that losses are just "part of the process," ... ...more

WOYS - Guarantees ,Time Matters

June 09, 2026•7 min read

Invisible Lien Your IRA is Joint Account with the IRS

For decades, we’ve been told that "Wall Street" is the only street. We’ve been conditioned to believe that volatility is the price of admission for growth, that losses are just "part of the process," ... ...more

WOYS - Guarantees ,Time Matters

June 09, 2026•6 min read

Why Most Retirement Plans are Set to Self-Destruct

If you’re planning to retire in the next few years, or if you’re already there, you’re currently sitting on a ticking time bomb. No, I’m not talking about the latest geopolitical flare-up or a sudden ... ...more

WOYS - Guarantees ,Time Matters

June 08, 2026•9 min read

Delay: Why Later Doublings are the secret to Wealth

Most people think the cost of waiting is just the return they miss this year. They look at a 5% or 7% market fluctuations and think, "I'll just catch the next wave." They are wrong. The true cost of d... ...more

WOYS - Guarantees ,Time Matters

June 08, 2026•7 min read

Annuities Pros and Cons: A Strategy for Guaranteed Growth

If you’ve spent the last twenty or thirty years in the workforce, you’ve likely been fed a steady diet of "Peter Pan Math." This is the financial fairy tale where you’re told to think happy thoughts, ... ...more

WOYS - Guarantees ,Time Matters

June 06, 2026•8 min read

Retirement Income Calculator Truth About Generic Math

You’ve seen the chart. It’s smooth, it’s green, and it marches upward at a perfect 45-degree angle. You plug in your current savings, your "expected return," and, presto!, the internet tells you you’r... ...more

WOYS - Guarantees ,Time Matters

June 06, 2026•10 min read

Protect Retirement Savings Market Crash Everything Needed

You’ve spent the last thirty years building. As a business owner, executive, or engineer, you’ve mastered the art of production. You understand systems, you respect the math, and you value precision. ... ...more

WOYS - Guarantees ,Time Matters

June 06, 2026•6 min read

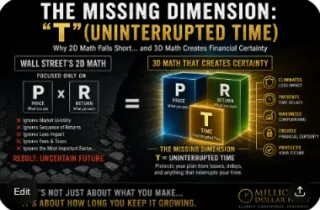

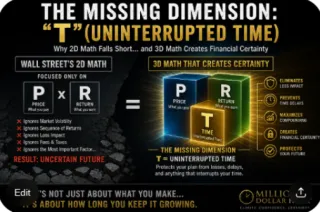

The Secret to PxRxT: Engineering Wealth on Your Street

If you want true financial peace, you must stop gambling and start engineering. At Your Street Wealth, we don’t look at "projections" or "probabilities." We look at the math. Specifically, we look at ... ...more

WOYS - Guarantees ,Time Matters

June 05, 2026•7 min read

Annuities: The Good, The Bad, and The Wall Street Lies

If you’re an engineer, a business owner, or someone who spent forty years building something real, you probably have a healthy skepticism for "sales pitches." You don't want a story; you want the math... ...more

WOYS - Guarantees ,Time Matters

June 05, 2026•6 min read

Gratitude and a Goldfish: Why Your Emotions Are Wall Street’s Favorite Weapon

There is a strange paradox in the world of money. Gratitude is the shortest-lived human emotion. It’s a spark that flickers and fades the moment the next “opportunity” or "threat" flashes on a screen.... ...more

WOYS - Guarantees ,Time Matters

June 05, 2026•7 min read

Why Time, Not Money, Is Your Biggest Retirement Risk

Most people believe the greatest threat to their retirement is losing money. They watch the tickers. They check their apps. They sweat the red days and breathe a sigh of relief when the green days ret... ...more

WOYS - Guarantees ,Time Matters

June 04, 2026•7 min read

The 5 Numbers That Will Determine Your Retirement Future

Most people spend more time researching a two-week vacation than they do evaluating the financial architecture that will fund the next thirty years of their lives. They live in a state of "unknowing":... ...more

WOYS - Guarantees ,Time Matters

June 04, 2026•6 min read

Best Retirement Income Strategies: Stop Market Gambling

If you feel like you’re "behind" in the retirement race, you’re not alone. Most people in their 40s, 50s, and 60s feel a low-grade fever of financial fatigue. They look at the 401(k) balance, look at ... ...more

WOYS - Guarantees ,Time Matters

June 03, 2026•6 min read

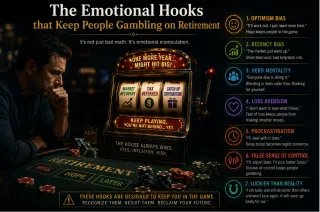

The 7 Emotional Hooks Keeping You Tethered to Wall St Gamble

You’ve spent thirty years building. You’ve survived the dot-com bubble, the 2008 crash, and the recent whipsaws of a post-pandemic economy. By most measures, you are a success: a "Quiet Builder" who h... ...more

WOYS - Guarantees ,Time Matters

June 03, 2026•7 min read

The 5 Layers of Secrecy Your Retirement Risk

If you are a "Quiet Builder": someone who has spent decades focused on your craft, your business, or your career: you likely assume that the financial systems holding your wealth are built on the same... ...more

Time Matters

June 03, 2026•6 min read

The Secrecy Layers: Who Benefits from Your 401(k) Risk?

If you have a 401(k), IRA, 403(b), or a standard brokerage account, I have a forensic question for you: Where is the benefit of all the risk you are carrying? You see the red days. You feel the stoma... ...more

WOYS - Guarantees ,Time Matters

June 03, 2026•6 min read

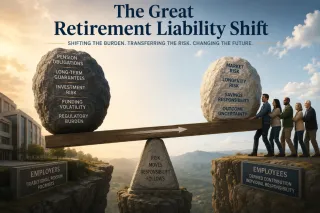

Pension vs. 401k vs. FPA: Choosing Guaranteed Income

Before this shift, retirement was built on the "Known." If you worked for a major corporation, they carried the liability of your future on their balance sheet. After 1975, the liability was handed to... ...more

WOYS - Guarantees ,Time Matters

June 03, 2026•6 min read

Reliability of Delivery Your Retirement Contract

If you’re a "Quiet Builder": the kind of person who spent thirty years engineering a career, a business, or a corporate division: you know that hope is not a strategy. In the world of institutional-gr... ...more

WOYS - Guarantees ,Time Matters

June 03, 2026•7 min read

Avoid the Lost Landing: Engineered Retirement Certainty

Imagine you’re standing at the open door of an airplane, 10,000 feet above the ground. You’ve spent twenty years preparing for this jump. You’ve been told the parachute is in the bag. You’ve been told... ...more

WOYS - Guarantees ,Time Matters

June 03, 2026•8 min read

The 7 G’s of Retirement Success: A Forensic Guide

For the "Quiet Builder": the business owner, the retired engineer, the former executive: retirement isn’t about the "next big thing." It’s about the last big thing. It’s about ensuring that the wealth... ...more

WOYS - Guarantees ,Time Matters

June 03, 2026•6 min read

Arithmetic vs Geometric Why Average Returns Are Lie

If you have a $1,000,000 retirement portfolio and it grows by 50% this year but drops by 50% next year, what is your "average" return? Wall Street would tell you it’s 0%. They’d tell you that you’re "... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•6 min read

ICA of Last Resort: Why People Move States

Irrevocable Corrective Actions (ICA). They move. They leave high-tax states like New York or California. They sell homes they’ve lived in for decades. They relocate businesses, change schools, find ne... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•7 min read

A Universal Methodology for Geometric Improvement

The difference between the two is the difference between struggling to stay afloat and achieving effortless, geometric growth. At Your Street Wealth, we call this difference an ICA: an Irrevocable Cor... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•8 min read

Protect Retirement Savings from Market Crash with an ICA

In the business world, risk is something you manage, mitigate, and: most importantly: engineer out of the system. We call this an ICA, or an Irrevocable Corrective Action. It’s the process of finding ... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•8 min read

The Forensic Audit of Hidden Fee Compounding

If you walked into your kitchen and saw a steady drip falling from the faucet, you wouldn’t just watch it. You’d grab a wrench. You’d call a plumber. Why? Because you know that a "small" leak isn't ju... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•8 min read

Average' Returns are a Retirement Death Sentence

If you’ve ever sat across from a Wall Street broker, you’ve heard the "Stay the Course" sermon. They point to a colorful chart showing an "Average Annual Return" of 7% or 8% and tell you that as long ... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•9 min read

CEO ARCHITECT Engineering MDH for Post Business

For decades, you’ve been the CEO. You’ve managed people, navigated market shifts, and mastered the art of active participation in the economy. You’ve been the pilot, the captain, and the primary engin... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•6 min read

Your Retirement Plan is Currently Shorting Your Business Legacy

Every successful business owner understands the difference between an asset and a liability. You spend your life optimizing your balance sheet, scrubbing expenses, and ensuring your capital is allocat... ...more

WOYS - Guarantees ,Time Matters

June 02, 2026•6 min read

High-Performing Business Owners are Losing Years

You’ve built a company from the ground up. You’ve mastered the art of managing teams, navigating markets, and engineering a product or service that people actually value. You are a high-performer. ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•6 min read

Why Risk Belongs in Your Business, Not Your Retirement

You’ve spent decades mastering the art of the calculated risk. As a business owner, risk was your primary tool for growth. You bet on yourself, your team, and your vision. You understood that in the m... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•7 min read

'Stay the Course' is a Retirement Death Trap

For most high-achievers, there is a recurring nightmare that begins about five years before they plan to walk away from their business or career. It’s the feeling of being on a high-speed train where ... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•6 min read

Annuities Pros and Cons: Guaranteed Retirement Income Guide

For most "Quiet Builders": those successful business owners, engineers, and executives nearing the finish line: the word "annuity" triggers a visceral reaction. It’s either the promise of a golden "gu... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•6 min read

Forensic Audit $10 Diagnostic for the Sequence of Returns Trap

The patient was 65. He had a clean bill of health: or so his "Participation" reports from Wall Street said. He had spent 30 years dutifully feeding his 401(k), watching it grow into a $1.2 million "ne... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•7 min read

Guaranteed Lifetime Income: The Engine vs. Transmission Shift

You’ve spent thirty years building the "Engine." You fed it monthly contributions. You endured the noise of CNBC. You watched the ticker symbols dance. You were told that the bigger the engine (your n... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•6 min read

10 Rules for a Retirement That Actually Works

Recently, a 30-year-old reader pulled me aside after finishing a few of our articles. She didn’t want the "market update" or the latest stock tip. She asked a question that most people twice her age a... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•6 min read

Is Your Retirement Plan Running on Prayer?

A retirement plan without guarantees isn't a strategy; it's a prayer. Are you really willing to find out your engine is "broken" when you’re 10 miles into the desert with no cell service and the sun i... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•5 min read

Financial Malpractice: Why Your Retirement Plan Is Broken

If you were sitting in an architect’s office and said, “I want a house that won’t fall down during an earthquake,” and that architect replied, “Well, we’ll aim for ‘Acceptable Collapse’ based on histo... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•7 min read

Your Wall Street Strategy is a Forensic Emergency

If you’ve ever heard the phrase “the market is short-sighted,” you probably nodded along, thinking it was just another piece of common Wall Street wisdom. You likely didn’t realize it was a warning th... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•6 min read

Your Retirement Plan Is Losing Money You Can’t See

You open the envelope, see a "plus" sign next to your balance, and breathe a sigh of relief. You think you’re winning. But while you’re looking at the front door, four invisible thieves are emptying t... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•5 min read

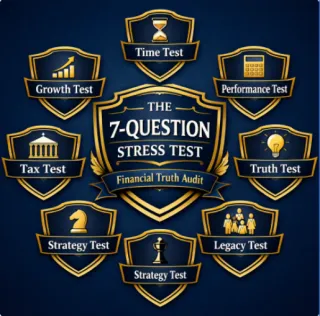

The 7-Question Retirement Stress Test

Most retirement plans are built on a "Story." Wall Street tells you a tale about historical averages, "long-term" growth, and the magic of diversification. But stories don't pay for groceries when the... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•4 min read

a 90% Success Rate is a 100% Gamble

It’s that shiny, free online tool on some big-name brokerage site. You plug in your age, your current savings, and a guess at your future spending. You hit "Calculate," and the screen flashes a comfor... ...more

WOYS - Guarantees ,Time Matters

June 01, 2026•9 min read

Part 6: Time is NOT on Your Side

But if you are 62 years old and that 20% drop takes you five years to recover just to get back to where you were today, you haven’t just lost money. You’ve lost five years of your life. That is a Time... ...more

WOYS - Guarantees ,Time Matters

May 31, 2026•7 min read

Protect Retirement Savings from Market Crash: 4 Wealth Killers

If you’re a "Quiet Builder" trying to protect retirement savings from market crash risk: someone who spent decades scaling the corporate ladder, engineering systems, or building a business: you know t... ...more

WOYS - Guarantees ,Time Matters

May 31, 2026•7 min read

Retirement Plan Review: Participation or Architecture?

Guaranteed Retirement Income and Retirement Income Planning should start with one simple question: is your strategy built to protect your time, or just keep your money participating in risk? When you ... ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•9 min read

Taking Your Profits Off the Table Before They Take Them Back

Wall Street is a jealous lover. It demands your absolute loyalty, your constant attention, and most importantly, your capital. They tell you to “stay the course,” to “buy and hold,” and to “weather th... ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•8 min read

Be Loyal to Yourself by Taking Your Gains Out of Risk

If you’ve spent the last 20 to 30 years building a business, climbing the corporate ladder, or engineering complex systems, you know one thing to be true: success isn’t accidental. It’s designed. ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•6 min read

Why a 10% Market Drop Destroys Retirement Savings Faster

In the world of the "Quiet Builder," silence is usually a sign of progress. You’ve spent decades accumulating, managing your business, and ignoring the daily noise of Wall Street. But as the market hi... ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•6 min read

Part 1 - The Psychology of the Peak

If you’ve been watching the headlines lately, you’ve probably seen a lot of celebration. The markets are hitting all-time highs. Your 401(k) statement looks better than it did two years ago. On paper,... ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•7 min read

Two Questions Wall Street Hopes You Never Ask

They’ve been told by every glossy brochure, every talking head on CNBC, and every "wealth manager" with a shiny office that the secret to a successful retirement is a "Magic Number." Usually, that num... ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•7 min read

7 Retirement Shields: A Financial Truth Audit for Certainty

They participate in the ups and downs of the S&P 500. They participate in the hope that taxes won’t skyrocket. They participate in the "probabilities" that Wall Street analysts throw at them like conf... ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•6 min read

10 Reasons Your Retirement Engine is Broken And How to Fix

They are “participating” in a Wall Street model designed in the 1970s: a model that worked when the world was a Rolodex, but is dangerously inadequate in a SpaceX world. If you feel a lingering sense ... ...more

WOYS - Guarantees ,Time Matters

May 30, 2026•7 min read

Defeating Wealth Killers Before, During, and After Your Career

They use that word a lot because it sounds inclusive and friendly. But in the world of high-stakes finance, "participation" is just another word for being a passenger on a ship you don’t captain. When... ...more

WOYS - Guarantees ,Time Matters

May 29, 2026•6 min read

Your Last Paycheck is the Deadline for Tax-Free Wealth

Most "Quiet Builders": those successful business owners and executives who have spent decades stacking bricks: believe that retirement is the time when you finally get to stop worrying about the rules... ...more

WOYS - Guarantees ,Time Matters

May 29, 2026•7 min read

Your Quick-Start Guide to a Retirement Plan Review

For decades, you’ve been the pilot. Whether you were building a business, managing a complex engineering project, or navigating a corporate career, your income was a "Working Asset." It was fueled by ... ...more

WOYS - Guarantees ,Time Matters

May 29, 2026•6 min read

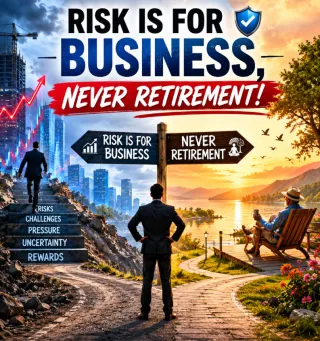

Risk is for Business, Not Retirement: Why Your 401(k) is a 'Working' Asset

You’ve spent the last 30 or 40 years as a "Quiet Builder." You took risks. You grew a business, climbed the corporate ladder, or managed complex engineering projects. You understood that to build some... ...more

WOYS - Guarantees ,Time Matters

May 29, 2026•7 min read

If Wall St Magic Box Worked Why Is Everyone Still Working

Wall Street has spent billions of dollars and millions of lines of code trying to convince you that they have finally built the "Magic Box." They call it AI-driven wealth management. They promise it c... ...more

WOYS - Guarantees ,Time Matters

May 29, 2026•10 min read

Wall Street AI vs. Retirement Certainty: The Win-Lose Truth

If you’ve turned on a television or scrolled through a financial news feed lately, you’ve seen the ads. They feature soothing voices and sleek, high-tech visuals promising that Artificial Intelligence... ...more

WOYS - Guarantees ,Time Matters

May 29, 2026•5 min read

Wall St vs Your Street: The Truth About Retirement Certainty

If you’ve spent the last 20 or 30 years building your nest egg, you’ve likely been told a very specific story. It’s a story about "market participation," "average returns," and "long-term growth." ...more

WOYS - Guarantees ,Time Matters

May 29, 2026•6 min read

7-Questn Retirement Stress Test Your Plan Built for Reality

Wall Street dresses that guess up with charts, simulations, and polished language, but the core problem stays the same: if your retirement depends on market participation, your future depends on varia... ...more

WOYS - Guarantees ,Time Matters

May 28, 2026•7 min read

11 Wealth Killers Every Pre-Retiree Needs to Know

Most retirement plans aren’t destroyed by a single catastrophic event. They aren’t taken down by one "big bad" market crash or a single bad investment. Instead, they are bled dry by a "Silent Heist": ... ...more

WOYS - Guarantees ,Time Matters

May 28, 2026•7 min read

Retirement Income Calculator. Possibilities Not Promises

If you’ve spent any time on a major brokerage website lately, you’ve probably played with their "Retirement Income Calculator." You plug in your age, your current savings, and a few "assumptions" abou... ...more

WOYS - Guarantees ,Time Matters

May 28, 2026•7 min read

Sync 15 Pillars for Guaranteed Retirement Wealth

Verification of a process occurs at two levels: the components and the totals. In school, we’re taught that the sum of the parts equals the whole. But in the world of high-level financial engineering,... ...more

WOYS - Guarantees ,Time Matters

May 28, 2026•6 min read

Wall Street Statement is Missing the Most Important Number

Most people believe that if they look at their monthly brokerage statement, they are seeing the "whole" story. They see a starting balance, a list of ticker symbols, some green or red arrows, and an e... ...more

WOYS - Guarantees ,Time Matters

May 28, 2026•6 min read

Trust but Verify: How to Verify Your Retirement Income Planning

In the world of Wall Street, "trust" is a high-priced commodity. Your broker asks for it. Your mutual fund manager relies on it. Your "average" return charts depend on it. But for the Quiet Builder: t... ...more

WOYS - Guarantees ,Time Matters

May 28, 2026•5 min read

Guaranteed Growth Secrets Revealed: What Wall Street Doesn't Want You to Know

For decades, the financial industry has sold you a story. It’s a story of "participation," "average returns," and "long-term growth." They tell you to keep your head down, ignore the volatility, and w... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•7 min read

Assets vs. Income: The Best Retirement Income Strategies

You’ve been told that if you just work hard enough, save enough, and “participate” in the market long enough, you’ll reach a magic summit, a pile of assets so large it can withstand anything the world... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•5 min read

Paved Cow Trail Your Safe Retirement on Unstable Ground

Whether you’ve spent forty years climbing the corporate ladder or built a business from the ground up, you’ve likely been led onto what we call the Paved Cattle Trail. For over 200 years, the financia... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•5 min read

Is Your Strategy Built for Wall Street or Your Street

You’ve spent the last thirty years playing a specific game. It’s the "Wall Street Game," and for a long time, it worked. You took risks, you endured the volatility, and you watched your accounts grow:... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•7 min read

Strait of Retirement: Keeping Your Wealth in Motion

For the last thirty years, you’ve been the captain of a heavy-duty cargo ship. You’ve braved the open ocean, weathered the storms of 2008 and 2020, and slowly stacked your hull with the fuel needed fo... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•6 min read

Waiting is the Most Expensive Decision in Retirement

Most people think "waiting" is a neutral act. They see a volatile market, hear the noise of the nightly news, and decide to "wait and see what happens" before fixing their retirement plan. In the wo... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•6 min read

Trading Good Enough Retirement to Fully Performing

Most retirement plans aren’t "broken" in the way a shattered mirror is broken. They are broken in the way a car with a misfiring engine is broken. It still moves, it still looks like a car, and if you... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•6 min read

Get the 11 Wealth Killers Off Your Retirement Bus

But here’s the cold, hard truth: Most retirement "buses" are currently packed with hitchhikers who aren't just taking up space: they’re actively picking your pockets while you try to drive toward the ... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•6 min read

Strategy to Turn Your Retirement from Good to Great

Most people work hard for forty years with one simple goal: a “good” retirement. They save, they invest in their 401(k)s, and they hope the market stays friendly enough to let them play a few rounds o... ...more

WOYS - Guarantees ,Time Matters

May 27, 2026•6 min read

10 Reasons Your Retirement Engine Is Broken

Most retirement plans look fine… right up until they don’t. That’s the Invisible Wall: the hidden math, hidden leaks, and hidden risk that don’t show up on the quarterly statement, until retirement ... ...more

WOYS - Guarantees ,Time Matters

May 26, 2026•7 min read

Why Your Retirement Strategy is a Casino in Disguise

You probably held a Zoom meeting today from a device that fits in your pocket. You didn’t think twice about it because you’ve lived through the Consolidation of Technology. You remember when a pager, ... ...more

WOYS - Guarantees ,Time Matters

May 26, 2026•7 min read

Why Your Retirement is Running Backwards

Time is your most critical commodity, and seconds matter. It takes seconds to identify that something is wrong. Seconds to learn better solutions exist. Seconds to schedule a session that can stop the... ...more

WOYS - Guarantees ,Time Matters

May 26, 2026•7 min read

7 Questions That Reveal if Your Retirement is at Risk

You look at your statements and see growth, but you also see the "drawdowns." You’ve been told that "participation" in the market is the only way to build wealth. But as you get closer to the day you ... ...more

WOYS - Guarantees ,Time Matters

May 26, 2026•10 min read

Uncapped Gains Trap How Wealth Killers Steal Your Retirement

Wall Street loves to sell you on the "Uncapped Gains" dream. It’s the ultimate carrot: the promise that if you just stay in the game, the sky is the limit. They show you charts that only go up and rig... ...more

WOYS - Guarantees ,Time Matters

May 26, 2026•6 min read

Why Your Retirement Needs a Master Architect

If you are currently following traditional Wall Street advice, you aren’t an architect; you’re a player in a high-stakes casino where the house always takes its cut. You are told to focus on "Average ... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Wall St vs Your St: Best Retirement Income Strategies for Guaranteed Growth

Ever walked into a casino and noticed there are no windows and no clocks? It’s by design. The environment is engineered to keep you in a state of perpetual "participation" until the house edge eventua... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Retirement Income Planning:is Failing: The Average Return Trap

You look at your retirement statements and see numbers that look "fine." Your broker tells you that you’ve had an "average return" of 7% or 8% over the last decade. On paper, the engine is running. ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Risk is for Business, Not Retirement: Protect Your Savings

In the world of business, risk can make sense because you can mitigate it with skill, talent, leadership, and solid processes. You can hire better. Sell better. Adapt faster. If something breaks, you ... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

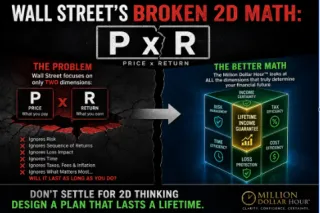

Why Retirement Math is Broken by 2D Trap 7 Wealth Killers

It’s a flat-earth approach to finance that focuses almost entirely on two things: Price and Return. The pitch is simple: "If the market averages 8%, and you have $1M, you’ll have plenty of money in tw... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Controlling Retirement Variables: 7-Vector Wealth System

Have you ever walked into a high-end restaurant where there are no prices on the menu? Or perhaps you’ve dealt with a contractor who told you, “You can have it fast, you can have it cheap, or you can ... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•7 min read

Guaranteed Lifetime Income vs Wall St Growth Which one?

Most retirement planning is just a high-stakes "Participation" game. You hand over your life savings to Wall Street, cross your fingers, and hope the "average returns" stay high enough to fund your li... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Choosing Guaranteed Value over Wall Street Free Cheese

For the "Quiet Builder": the successful business owner, the retired engineer, the former corporate executive: wisdom usually comes from a life of building things that work. You know that a bridge does... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Wealth Assassin: 7 Sequence of Returns Mistakes

You’ve spent thirty years building a bridge. You’ve laid the bricks, poured the concrete, and fortified the structure. But as you prepare to drive your retirement across it, you notice something terri... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Best Retirement Income Strategies: Solving the Income Gap

You’ve spent decades building. You’ve been the "Quiet Builder": the one who worked hard, saved diligently, and mostly ignored the daily noise of the headlines. You’ve followed the traditional rules: c... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

Protect Retirement Savings: 3 Stealth Wealth Killers

You’ve done everything right. You’ve worked hard, lived beneath your means, and steadily built what most people would call a solid financial life. Your quarterly statements show a number that seems to... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•8 min read

Why Retirement Calculators Fail: The Truth About Average Returns

If you’ve spent any time on a major bank or brokerage website, you’ve seen them: the "Free Retirement Calculator." You plug in your age, your current savings, and a magic number like "7% average retur... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•6 min read

How to Capture Market Upside Without the Downside Risk

If you’ve spent any time on Wall Street, you’ve been sold a story. It’s a story about participation. They tell you to hop into the market, hold on tight, and ride the waves. But here’s the problem: W... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•7 min read

Sequence of Returns Risk vs Volatility: Retirement Strategy

If you’ve spent the last twenty or thirty years building a career, a business, or a life of "Quiet Building," you’ve likely grown accustomed to the market’s mood swings. You’ve seen the headlines scre... ...more

WOYS - Guarantees ,Time Matters

May 25, 2026•7 min read

Wall Street is a Mechanical Watch in an Atomic Age

They spend their lives obsessing over account balances, rates of return, and market performance. But here is the reality that Wall Street won’t tell you: Retirement is a time problem before it is a ... ...more

WOYS - Guarantees ,Time Matters

May 24, 2026•7 min read

How to Build a Machine That Never Runs Out of Money

If you’ve spent your career building a nest egg, you’ve likely been told that if you just "stay the course" and follow the "4% rule," everything will work out. But "working out" is a matter of probabi... ...more

WOYS - Guarantees ,Time Matters

May 24, 2026•6 min read

Why Your ‘Growth’ Strategy is Actually a Hazard

As a business owner, executive, or high-level professional, you understand that risk is the fuel for growth. You’ve navigated market shifts, managed "spinning sharp knives" in the form of interest rat... ...more

WOYS - Guarantees ,Time Matters

May 24, 2026•6 min read

Staying the Course is a Retirement Death Sentence

On the surface, "staying the course" sounds stoic. It sounds brave. It sounds like something a sea captain would say while gripping the wheel in a hurricane. But here’s the problem: you aren’t a sea c... ...more

WOYS - Guarantees ,Time Matters

May 23, 2026•6 min read

Market Losses Make Your Money Disappear

They tell you it’s the ultimate safety net. "You can get to your money whenever you want!" they chirp, as if that solves every problem. But here is the cold, hard truth that most advisors won't tell y... ...more

WOYS - Guarantees ,Time Matters

May 23, 2026•6 min read

HIdden Thieves Quietly Steal Your Nest Egg

If you’ve spent twenty or thirty years diligently feeding your 401(k), you might think you’re holding a winning lottery ticket. But here’s the cold, mathematical reality: there are invisible thieves i... ...more

WOYS - Guarantees ,Time Matters

May 23, 2026•7 min read

Avg Return Trap Wall St Math DNE Retirement Success

Your advisor shows you a shiny brochure with a 7% or 8% historical average. They tell you to "stay the course" because, over time, the math works out. But here is the problem: you don’t live on "avera... ...more

WOYS - Guarantees ,Time Matters

May 23, 2026•7 min read

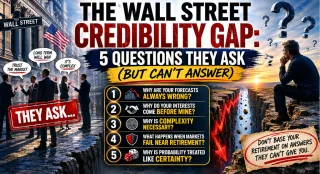

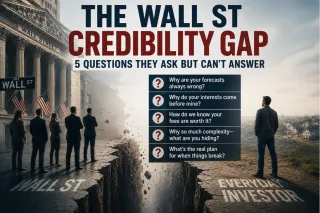

Wall Street Credibility Gap 5 Retirement Questions For Life

See why Wall Street fails a proper retirement plan review. Learn about sequence of returns risk, retirement income calculator limits, and how much you need to retire with engineered certainty. ...more

WOYS - Guarantees ,Time Matters

May 23, 2026•8 min read

The Problem Why Wall St Blueprints Always fail

If accuracy actually mattered on Wall Street, why are the same "expert" forecasters still famous? Think about it. In almost any other industry, being wrong as often as a financial pundit would get you... ...more

WOYS - Guarantees ,Time Matters

May 23, 2026•7 min read

Wall St asks about Risk Tolerance not Risk Elimination

Imagine you’re standing at the edge of a deep canyon, looking at a bridge you need to cross to reach your retirement. You ask the engineer, “Is this bridge safe?” Instead of showing you the blueprints... ...more

WOYS - Guarantees ,Time Matters

May 23, 2026•8 min read

Retirement Confidence Illusion not the same as safe